Despite market volatility and noise, US Treasuries are still considered a safe-haven

Rick Patel

Recent market volatility and news flow driven by geopolitical and trade issues have led some to question the US Treasuries’ status as a safe-haven. While there are valid concerns around the recent US credit downgrade from Moody’s, the size of the US fiscal deficit, and questions around overseas demand for Treasuries, we believe that this fear is overstated.

To begin with the first point, the US had been on ‘negative watch’ from Moody’s for around 18 months prior to the downgrade over concerns around the fiscal landscape. So the downgrade was not necessarily unexpected. In addition to this, Moody’s has recently highlighted the ‘exceptional credit strengths the US still has, including ‘the size, resilience and dynamism of its economy and the role of the US dollar as the global reserve currency.’ The size, liquidity and strength of the US market is unparallelled and irreplaceable and we expect US Treasuries and credit to remain a key allocation for investors globally.

When it comes to the fiscal deficit, while we are concerned about the increase here given projections of a deficit of around seven per cent over the next few years, it is important to break this number down. In the most simplistic terms, this around seven per cent forecast can be halved into around 3.5 per cent from interest payments on Treasury debt and around 3.5 per cent from fiscal spending. As we move closer to a potential series of Fed rate cuts, interest expenses will fall, therefore reducing the size of the deficit. This would limit concerns from bond markets about the debt to GDP ratio. What concerns us more, and has done for quite some time, is that in a scenario where the US economy weakens, any fiscal support is now likely to be much smaller and less forthcoming than in previous crises, as the government will simply have less fiscal headroom to spend.

With deficit projection this high, it is no secret that the US will need to issue heavily in the bond market. Understandably, there has been some concern that recent geopolitical events have limited overseas demand for US Treasuries. As a starting point, we would highlight that the trend of Japanese and Chinese institutional investors slightly reducing their allocation to the US has already been taking place for some years now, with a limited impact on overall demand.

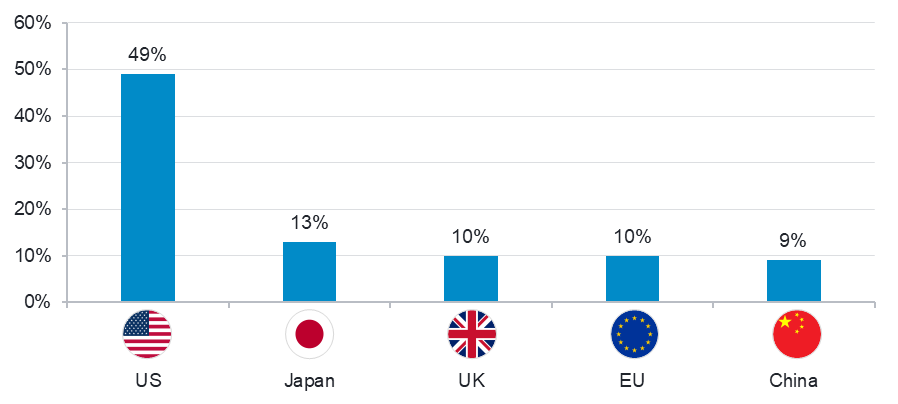

In addition, the thing that provides us with a high degree of comfort in the resilience of demand for US Treasuries going forward is the composition of domestic wealth. For instance, compared to the rest of the world, US households have a much higher allocation to equities, so there is material capacity for US domestic investors to increase their allocation to fixed income. To put this in perspective, a one per cent increase in US domestic allocations to fixed income would likely fund the increased US Treasury issuance for the next two to three years. There are numerous ways this small asset allocation shift could happen. An organic increase is likely, with attractive yields on US Treasuries inducing pensions, insurance and multi manager accounts to increase their allocations, limiting the need for individual investors to actively switch, or there may be some form of tax incentive from the US government.

US households’ allocation to equities is very high relative to other countries

Source: Fidelity International, Goldman Sachs Global Investment Research. June 2025.

Whilst there are many unknowns ahead and some of the concerns around the US are just, we remain convinced that should the US economy weaken enough to trigger a flight to quality, US Treasuries are well positioned relative to risk assets. The fact is there are few viable alternatives to Treasuries, and we expect a very limited change in demand in the long term.

By Rick Patel, portfolio manager