CPD: Lessons from ethical failures in financial advice

Adherence to the Code of Ethics can avoid risk of criminal activity in your practice.

Ethical standards are the foundation of financial advice, defining the trust and professional bond between advisers and their clients. While most professionals operate with integrity, a small minority within the industry act with criminal intent. This article, proudly sponsored by GSFM, explores the complex relationship between ethical conduct and criminal behaviour in the financial advice sector.

Financial advice serves a vital function, empowering individuals and organisations to make educated choices regarding their economic prospects. In a world of increasing complexity and market volatility, the insight provided by seasoned professionals often dictates the boundary between financial security and hardship. Professional guidance transforms overwhelming data into actionable strategy, ensuring that long-term stability remains achievable for everyone.

From retirement and investment planning to debt and estate management, advisers help clients navigate market intricacies while mitigating risks and capturing growth. By offering tailored strategies and fostering trust-based partnerships, these professionals provide the support necessary for clients to reach their objectives. This personalised approach is essential for securing a prosperous and stable future in an unpredictable global economy.

Ethical considerations are the cornerstone of financial advice, defining the professional bond and the trust that sustains it. Central to this integrity is the principle of fiduciary duty, which requires advisers to act with total loyalty and good faith toward their clients. This commitment ensures that the client’s welfare remains the primary focus of every recommendation and strategic decision made.

This duty requires providing unbiased advice, disclosing all conflicts of interest and prioritising client best interests over personal or corporate gain. Transparency and professionalism are the core pillars of this ethical framework, as highlighted in the Financial Planners and Advisers Code of Ethics 2019 (Code of Ethics). Such standards ensure that every individual is fully informed and capable of making decisions that reflect their specific goals and risk tolerance.

To meet these rigorous standards, advisers must comply with all regulatory requirements while continuously evolving their professional knowledge and technical skills. By embracing these ethical principles, advisers do more than just follow the law; they protect the integrity of the entire financial profession. Ultimately, this dedication builds more resilient, respectful relationships that benefit both advisers and consumers over the long term.

Ethics and financial advice

There are two types of ethics relevant to financial advice: deontological ethics and virtue ethics.

Deontological ethics

Deontological ethics, rooted in Greek philosophy, emphasises the intrinsic relationship between duty and the morality of human behaviour. The term itself is derived from the Greek words deon, meaning ‘duty’ and logos, meaning ‘science’ or ‘study’. This framework suggests that the rightness of an act is found in the motive of the actor rather than the final result.

This ethical branch holds significant relevance for the financial advice profession. Within this framework, an adviser’s actions are judged by their adherence to established moral principles and rules, rather than their eventual outcomes. In practice, deontology stresses the necessity of following professional standards even when different choices might lead to greater financial benefits or more favourable short-term results.

Advisers operating under this framework, particularly through the industry’s Code of Ethics, are guided by moral imperatives such as honesty, integrity and transparency. They recognise a fundamental duty to act in their clients’ best interests, maintain strict confidentiality and proactively avoid conflicts of interest. For these professionals, the ‘right’ thing to do is defined by the rules of the profession.

A deontologist views a breach of ethical standards as a failure to fulfill a professional obligation. To them, the solution is to re-establish the rule of law and ensure future compliance with the Code of Ethics.

By prioritising ethical duties over personal gain or the pursuit of profit, advisers practicing deontology contribute to the cultivation of trust and credibility within the sector. This commitment fosters enduring relationships built on principles of honesty and ethical conduct. It ensures that the integrity of the profession remains intact, regardless of market volatility or

Virtue ethics

Virtue ethics is rooted in the deliberate cultivation of character and moral excellence. Within this philosophical framework, the focus shifts from merely adhering to external rules or duties to embodying internal qualities such as integrity, honesty, prudence and fairness. It suggests that ethical behaviour is not a checklist of obligations, but a natural reflection of a person’s ingrained habits and disposition.

For financial advisers, virtue ethics emphasises the importance of developing a virtuous character that instinctively guides their daily decision-making and professional behaviour. A virtue ethicist would view a breach of the Code of Ethics as a symptom of a deeper problem: the adviser lacks the internalised virtues – such as honesty, fairness or diligence – required for the job.

Advisers practicing this approach typically prioritise building trust and fostering meaningful relationships with clients based on mutual respect and empathy. They strive to demonstrate excellence in all aspects of their practice, from providing unbiased guidance to acting with genuine transparency in every transaction.

By embracing virtue ethics, financial advisers do more than just uphold high standards; they contribute to a broader culture of integrity and trust within the entire financial sector. This focus on character enhances the overall well-being of their clients while strengthening the profession’s reputation within the community. Ultimately, it creates a self-sustaining environment where ethical conduct is the standard rather than the exception.

In the context of the Code of Ethics, this approach aligns perfectly with the requirement for advisers to exercise ‘professional judgment’. While a rule can tell you what to do, virtue gives you the wisdom to know how to do it well in complex, real-world situations.

To illustrate deontological and virtue ethics in practice, let’s apply both lenses to a common dilemma: an adviser who recommends a slightly higher-fee managed account because it has a simpler administrative platform for the practice.

The deontological approach (the ‘duty’ view)

A Deontologist doesn’t care if the client ends up making money anyway; they care that a rule was bypassed.

The problem: The adviser did not act in the client’s best interests, potentially violating standards one, two and five.

The resolution: The adviser is disciplined because they failed to follow the Code. The solution is to reinforce the rules. The focus is on the fact that the action of choosing a higher-fee product for administrative ease is inherently a breach of the contract between the professional and the public.

The virtue ethics approach (the ‘character’ view)

A virtue ethicist looks at the adviser’s disposition. They aren’t just looking for a bad act; they are looking for a bad habit.

The problem: The adviser displayed the vice of self-interest rather than the virtue of integrity. They lacked the practical wisdom to see that their ease of doing business should never outweigh a client’s best interests.

The resolution: The solution involves mentorship; the adviser needs to be retrained to value the client’s outcome as their own. The goal is to develop a character so strong that even if a loophole in the rules existed, the adviser would still choose the lower-fee product because they always put their clients’ best interests before their own.

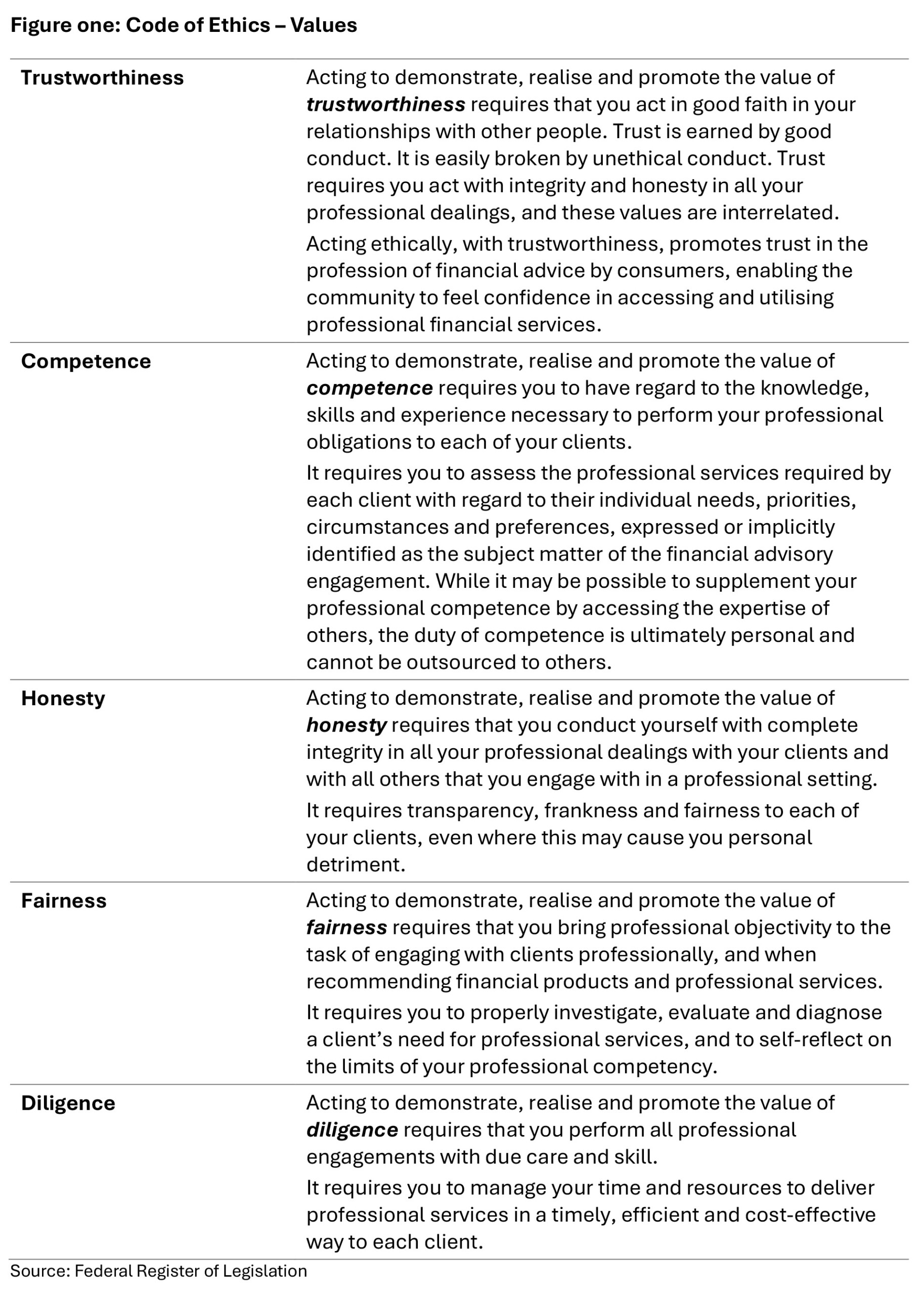

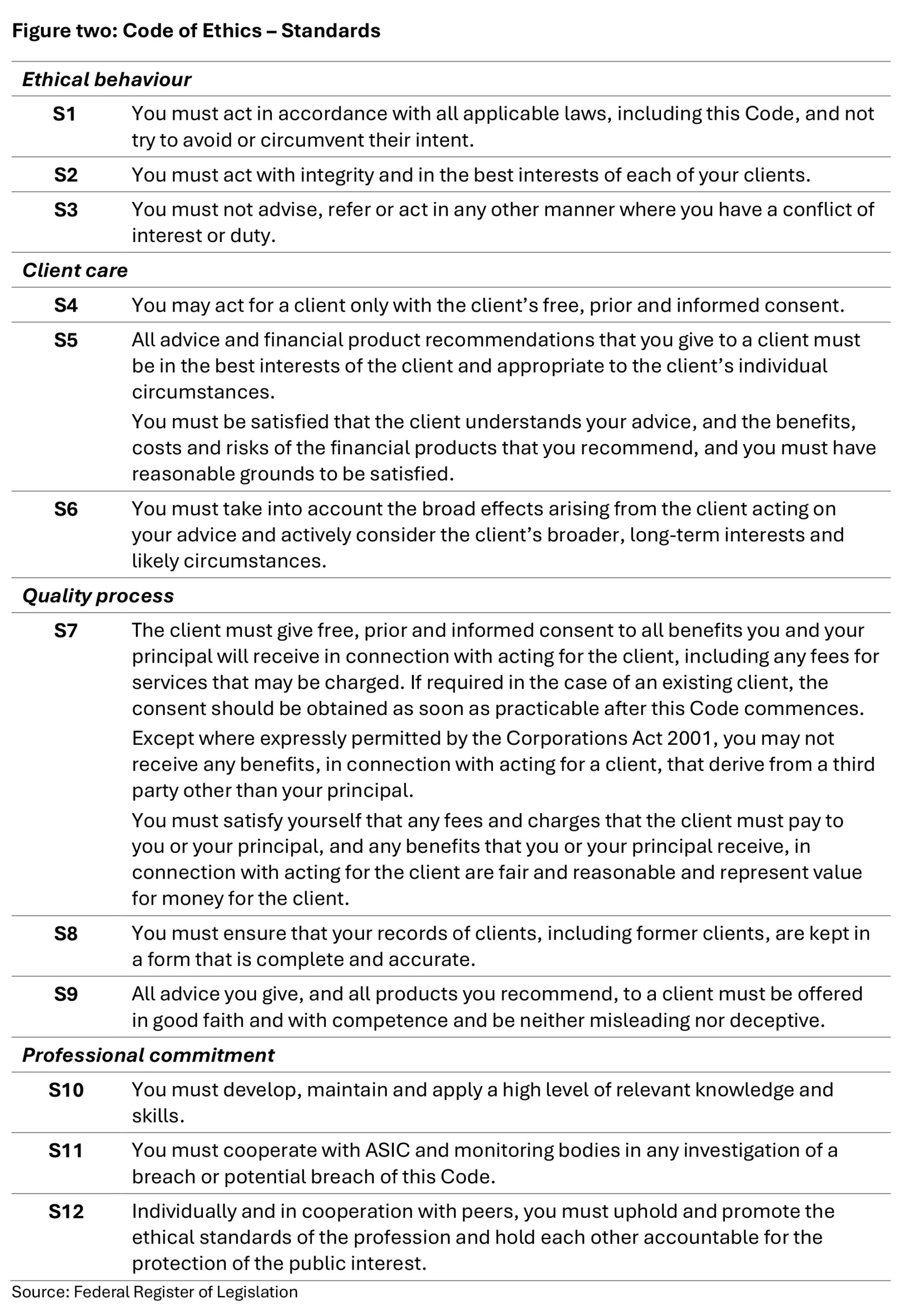

However, both deontological and virtue ethics are relevant to financial advisers. Both are enshrined in the values upon which the twelve ethical standards are based (figure one). Financial advisers are required to act in a way that demonstrates, realises and promotes each of these values. Further, the law intends that all provisions of the Code of Ethics are to be read and applied in a way that promotes the following values. While the values detailed in figure one can be said to enshrine value ethics, the standards themselves (figure two) are an example of deontological ethics.

Each of the five values relates to specific ethical standards (figure two) that must be applied to all interactions with every client. As such, to meet the spirit and legal obligations of the Code, advisers must embrace both deontological ethics and virtue ethics.

Ethics and criminal behaviour

Navigating the ethical landscape of financial advice is rarely simple. Advisers must manage a daily gauntlet of unforeseen conflicts of interest, competing fiduciary duties and regulatory loopholes that often create challenging grey areas.

In 2025, the Australian Securities and Investments Commission (ASIC) significantly increased its enforcement activity, driven by a 50 percent rise in investigations and a 20 percent increase in civil proceedings[1].

Enforcement actions range from numerous corporate matters, such as those related to insolvency or failing to maintain licence conditions even if not actively providing financial services, through to the more criminal: cases of fraud, pump and dump activity, insider trading, providing unlicensed financial advice and dishonest conduct.

Despite several sensational trade press headlines in 2025, criminal actions within the financial advice sector remains rare. There is a tendency to approach enforcement under civil rather than criminal law. However, when high-profile cases emerge, they typically gain a disproportionate level of notoriety.

By way of example, is the Shield and First Guardian Master Funds collapse. As of late 2025, ASIC is treating this collapse as a highly complex, large-scale civil enforcement investigation rather than a criminal prosecution, although criminal charges have not been ruled out. The regulator has over 40 people investigating the matter and anticipates further enforcement actions in 2025-2026. The headlines and ripple effects are expected to continue well into 2026.

Described by ASIC as ‘industrial-scale misconduct’ involving over $1 billion of investor funds, such media-driven ‘spectre’ of wrongdoing can unfairly cloud an industry predicated on trust. Such instances underscore the vital importance of standard twelve of the Code of Ethics, which mandates that advisers not only uphold ethical standards themselves but also hold their peers accountable to protect the public interest.

ASIC’s regulatory powers

ASIC’s primary objectives are to facilitate markets, promote trust and confidence in the financial system, and take action to enforce the laws it administers, which includes the Code of Ethics. Consequently, ASIC is empowered to take a range of criminal, civil and administrative action to address alleged misconduct within its jurisdiction.

ASIC investigates and takes enforcement action to detect, disrupt and respond to unlawful conduct. It aims to prevent and deter actual and future misconduct, improve standards and behaviours within its regulated population and importantly, reduce the risk of harm to Australian consumers and investors.

When deciding whether to investigate and take enforcement action, ASIC considers a range of factors that vary according to the nature and circumstances of the suspected misconduct. However, ASIC typically considers the following four factors when selecting matters for formal investigation and possible enforcement action:

- Areas of significant harm

- Broader public benefit

- Issues specific to the case

- Alternatives to formal investigation[2].

ASIC focuses its enforcement actions on preventing and addressing significant harm to consumers, markets and our financial system and prioritise those that involve:

- Actual or potential harm to vulnerable consumers or investors, particularly if the behaviour is predatory

- Misconduct that has caused or may cause widespread public harm

- Misconduct that is likely to have a significant market impact, which includes its impact on market integrity and the confidence of investors and consumers

- Misconduct that is systemic or widespread

- Misconduct that has recently emerged or is part of a growing trend.

There are three types of enforcement action ASIC may pursue, and it may take one or more of these to address a contravention of the law:

- Criminal proceedings

- Civil proceedings

- Administrative and other enforcement action.

The type of action taken is subject to what the laws governing the particular misconduct allow.

In the case of criminal proceedings, the laws administered by ASIC permit the courts to impose criminal sanctions for conduct ranging from minor regulatory offences to serious offences involving dishonesty. Examples of the sanctions that may be imposed are prison terms, criminal fines and court orders such as community service.

ASIC is most likely to pursue criminal proceedings in cases of serious and harmful wrongdoing, with the view to deter similar misconduct in the future. It generally considers criminal proceedings for offences that involve serious misconduct that is dishonest, intentional or highly reckless, even when civil action is also available.

Criminality and advice

So, what sort of action could result in ASIC instigating criminal proceedings? Here are just a few examples.

Fraud

Fraud is, unfortunately, the most common criminal offence perpetuated by advisers against their clients. Defined as “wrongful or criminal deception intended to result in financial or personal gain” by the Oxford dictionary, fraud can take a range of forms including:

- Falsifying documents

- Forging signatures on documents to authorise transactions without the client’s knowledge or consent

- Having money paid into personal accounts

- Running ponzi schemes

- Fraudulent investment schemes

- Elaborate investment ruses.

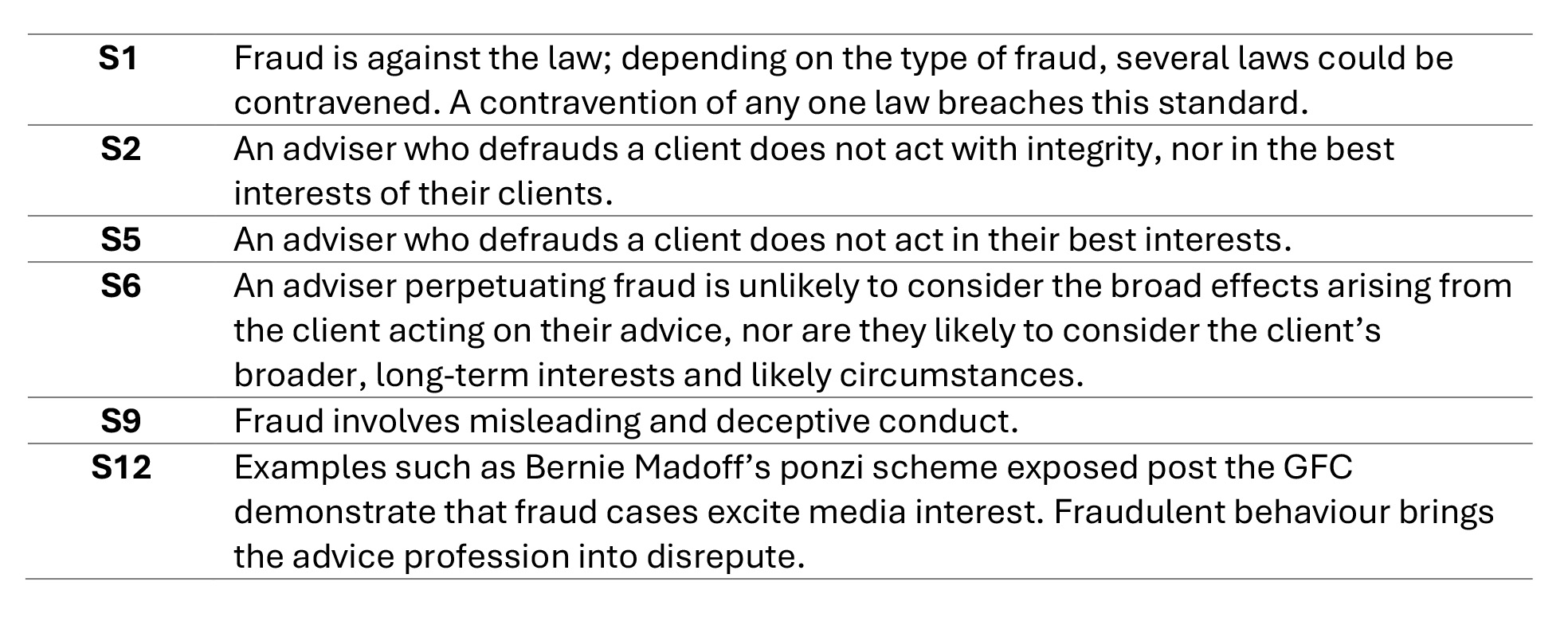

Fraud potentially breaches a number of ethical standards, including:

Money laundering

Financial advisers may knowingly (or unknowingly) facilitate money laundering activities by helping clients disguise the origins of illicit funds through complex financial transactions. This can involve structuring transactions to avoid reporting requirements or knowingly investing proceeds from criminal activities.

The Anti-Money Laundering and Counter-Terrorism Financing Act was introduced in 2006 and was designed to prevent and combat these crimes, which is essential to protect the integrity and stability of financial markets and the global financial system.

Holders of an Australian Financial Services Licence, including financial advisers, need to complete Part B of an AML/CTF program. Part B is focused on identifying clients and beneficial owners, including politically exposed persons.

However, it is important to note that major reforms to the AML/CTF Act and its rules are taking effect this year. For current reporting entities, such as existing AFSL holders, these new program requirements generally commence on 31 March 2026.

In broad terms, the new legislation officially removes the prescriptive requirement to separate AML/CTF programs into Part A and Part B. Businesses will now have the flexibility to organise their AML/CTF programs, provided they meet the overall obligation to identify, mitigate and manage risk.

Even though the Part B label is being phased out, the substance of the obligation remains:

- You must still identify clients and beneficial owners

- Identifying and managing risks associated with Politically Exposed Persons (PEPs) remains a mandatory component of due diligence

An adviser who is sloppy with paperwork may face enforcement action but is unlikely to face criminal proceedings. However, those found to have deliberately flouted the law with nefarious intent would face more serious charges.

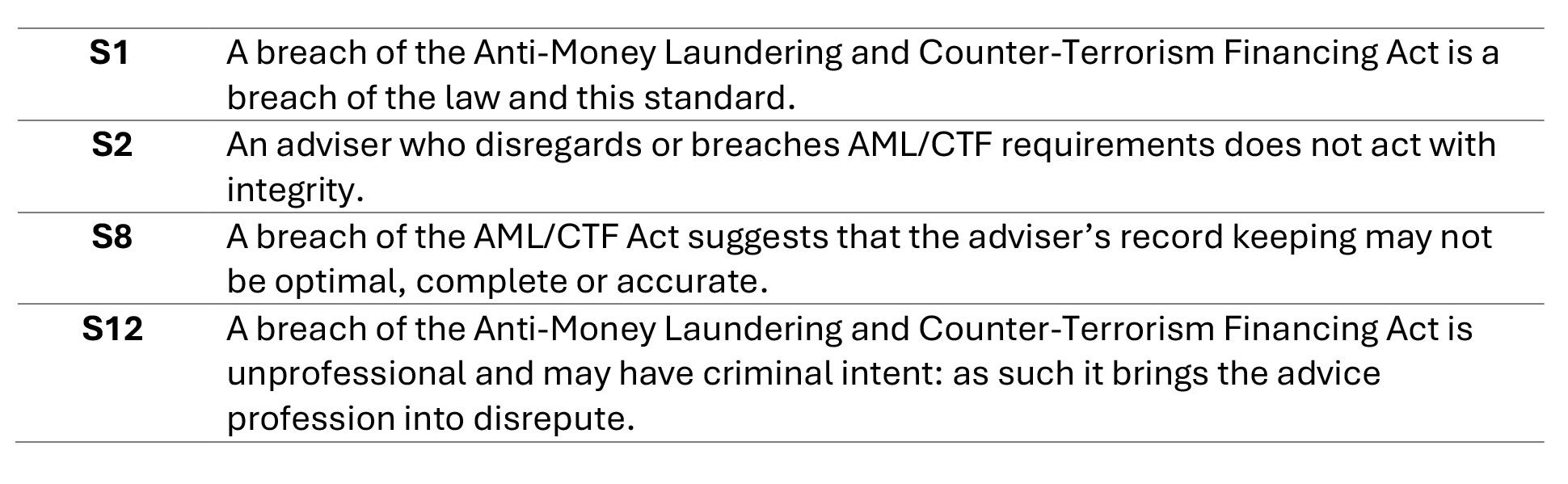

In the situation where an adviser has been found to breach AML/CTF requirements, it potentially breaches the following ethical standards:

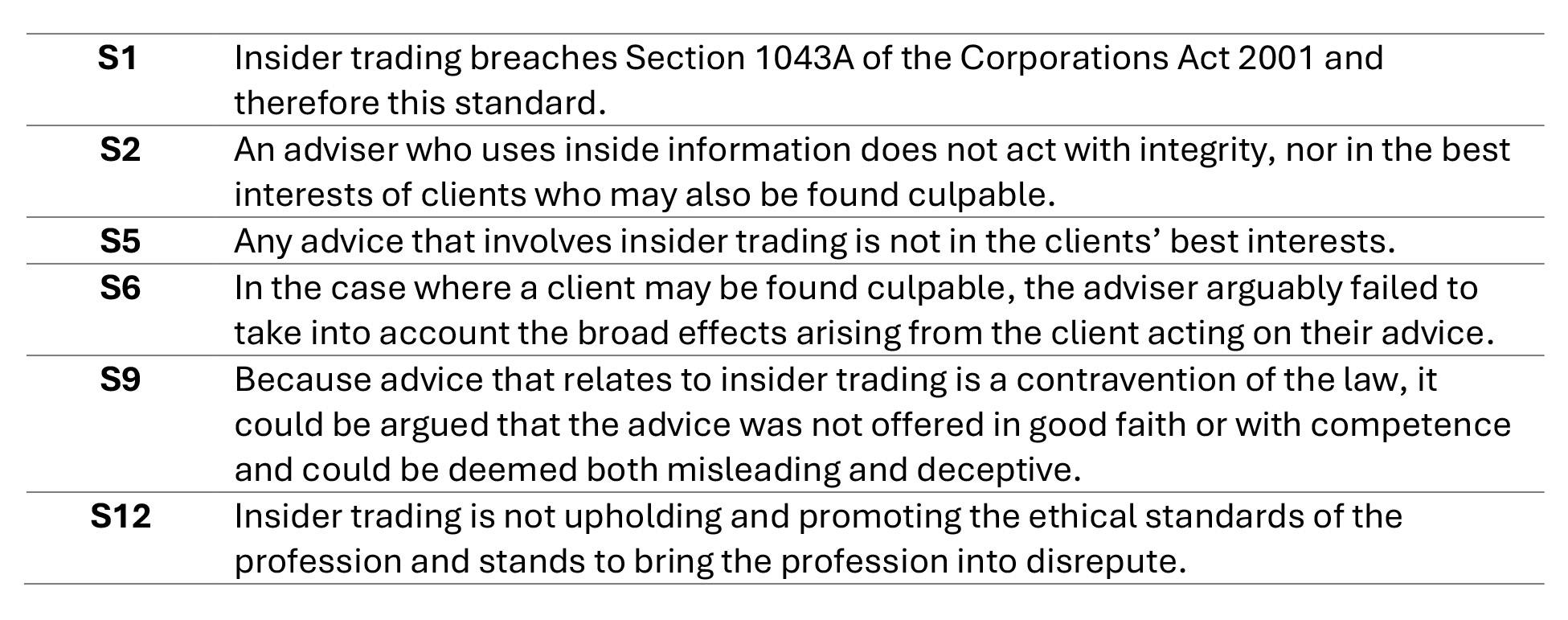

Insider trading

Strengthening investigation and prosecution of insider trading conduct is one of ASIC’s enforcement priorities for 2026. Insider trading breaches Section 1043A of the Corporations Act 2001 and prohibits a person from trading in listed securities while in possession of non-public, price-sensitive information.

The ASX regulatory guide explicitly states that Key Management Personnel, employees and family members are not permitted to trade when there is sensitive information not yet publicly disclosed. Inside information can easily come across an adviser’s path in the daily course of business and there’s nothing wrong with that – as long as they don’t act on it. Examples could include:

- A client who discusses a significant new contract won or issued by their business when either party to that contract is a listed company

- A friend who bemoans a substantial revenue hit for the listed company they work for and the potential ramifications

- Dinner party conversation in which you learn of a major merger between two listed companies

- An event at which a fellow attendee excitedly tells you how close his firm is to a significant innovation that will potentially boost the company’s share price

- An acquaintance working at the local council who happens to mention the reclassification of an area of commercial property to residential zoning.

While being in possession of said inside information is not against the law, advising a client to act upon it is, or acting on the client’s behalf, would likely breach the following standards:

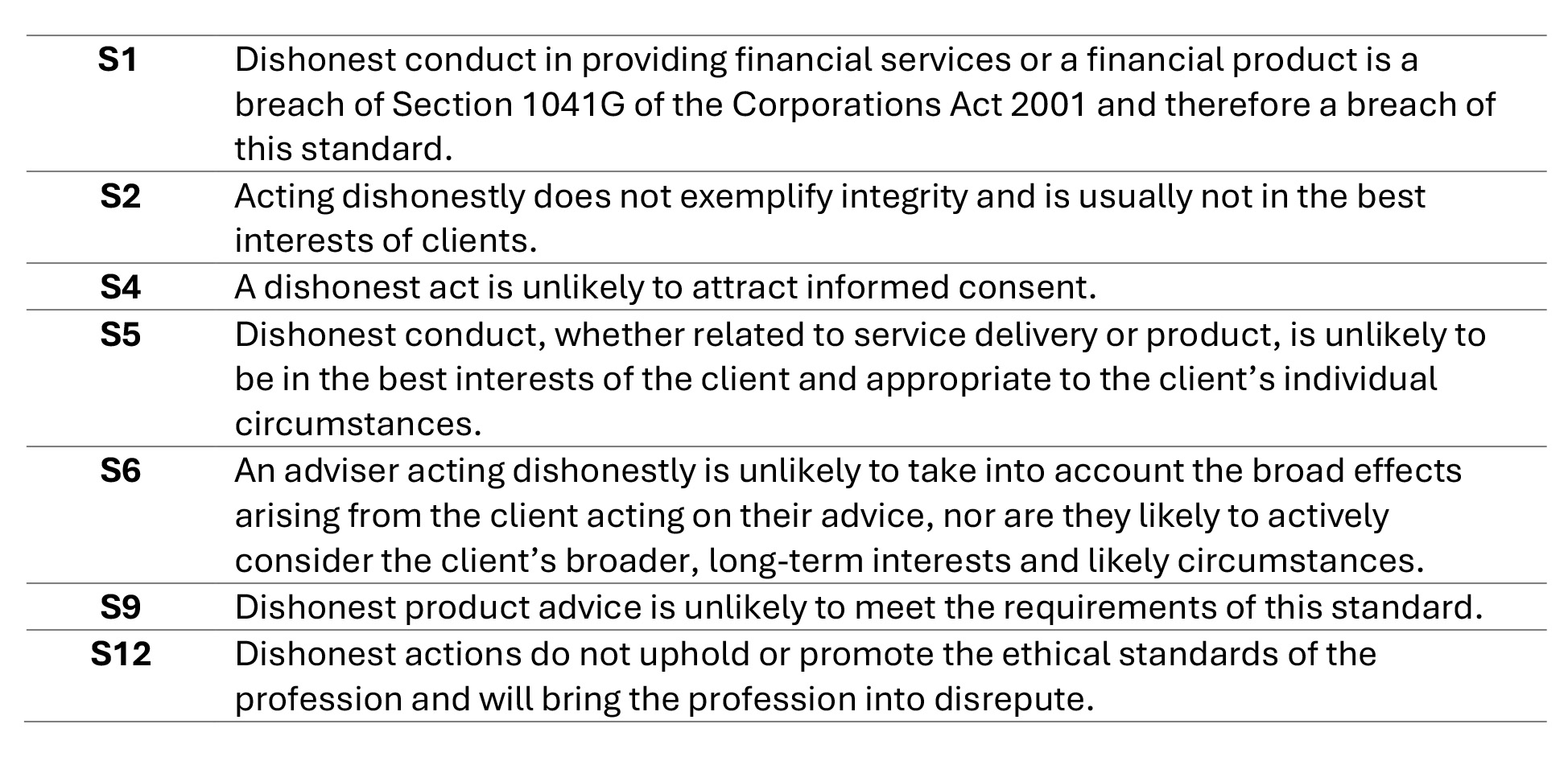

Dishonest conduct

As with so many acts of criminal behaviour, dishonest conduct can be viewed on a continuum, one where a first or minor misdemeanour may result in a minor enforcement action, through to more serious cases that face a criminal trial. Examples can include:

- Misrepresentation of a service offering

- Misrepresentation of qualifications and abilities of individuals and/or a business

- Misrepresentation of financial products

- Churning

- Ponzi schemes

- Pump and dump schemes

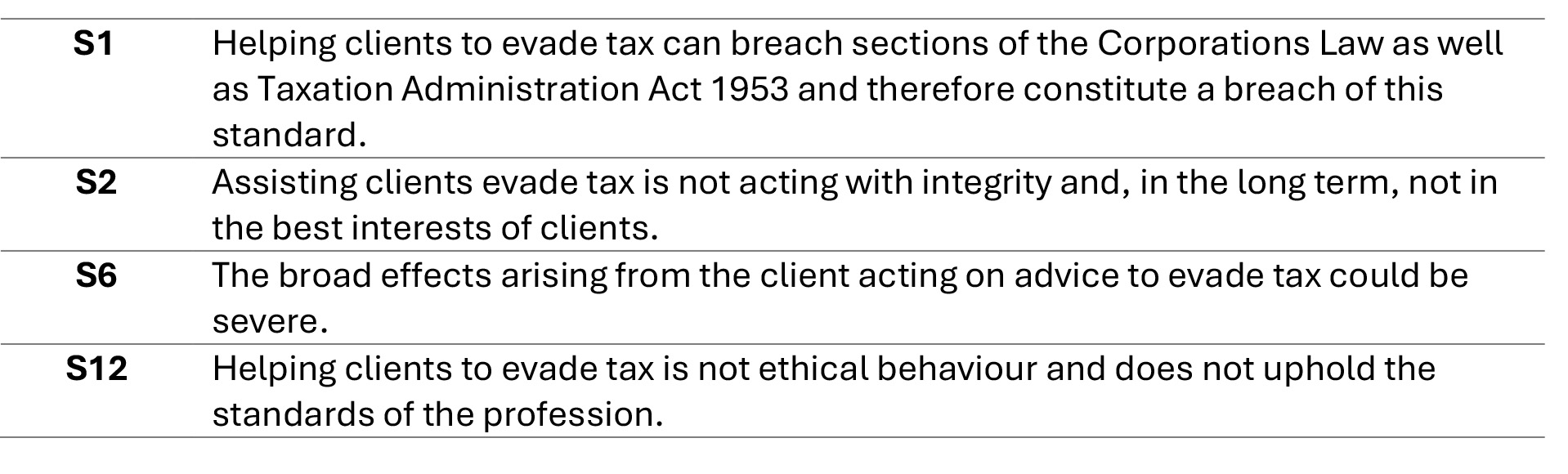

Tax evasion

While some tax minimisation strategies may be legal or exploit the grey zone between right and wrong, tax evasion is illegal. A small number of advisers may assist clients to evade tax by providing false information for tax returns, hiding income and assets offshore, or by using other tax avoidance strategies. Tax evasion is a serious crime that can result in criminal charges and severe penalties from both ASIC and the ATO.

Ethics, criminality and your practice

In a financial advice practice, maintaining ethical standards is not just about your own conduct but also about the actions of your colleagues and referral partners. Regular education and reinforcement of ethical practices are crucial to ensure the integrity of your business and relationships.

Dealing with ethical dilemmas, which can sometimes exist in shades of grey, requires time and effort for resolution. However, addressing these challenges can offer valuable insights and contribute to the ongoing improvement of your practice, helping to prevent or resolve similar issues in the future. In cases where dilemmas edge on criminality – or are well down that path – quick action is required.

It is easier to take appropriate action when your practice has procedures in place to deal with issues. These could include:

- A code of conduct that embodies the Code of Ethics and ethical practice

- Well documented policies and procedures that include an escalation policy in the event of malfeasance or criminal behaviour

- Regular training sessions for staff that use real-life examples and case studies to facilitate meaningful training and discussion within your team

- Support for team members who raise issues, including whistle-blower protection

The presence of ethical grey areas underscores the importance of alignment among all employees. You cannot assume that each of your team shares a highly developed ethical sense consistent with your expectations. Therefore, ongoing education, restatement, and reinforcement of integrity, corporate values and ethical behaviour are essential components of your educational efforts.

Case studies

The following case studies are based on real events; however, the names of people and organisations have been changed, and some details altered. The case studies have been drawn from ASIC and for each, potential breaches of the Code of Ethics are identified.

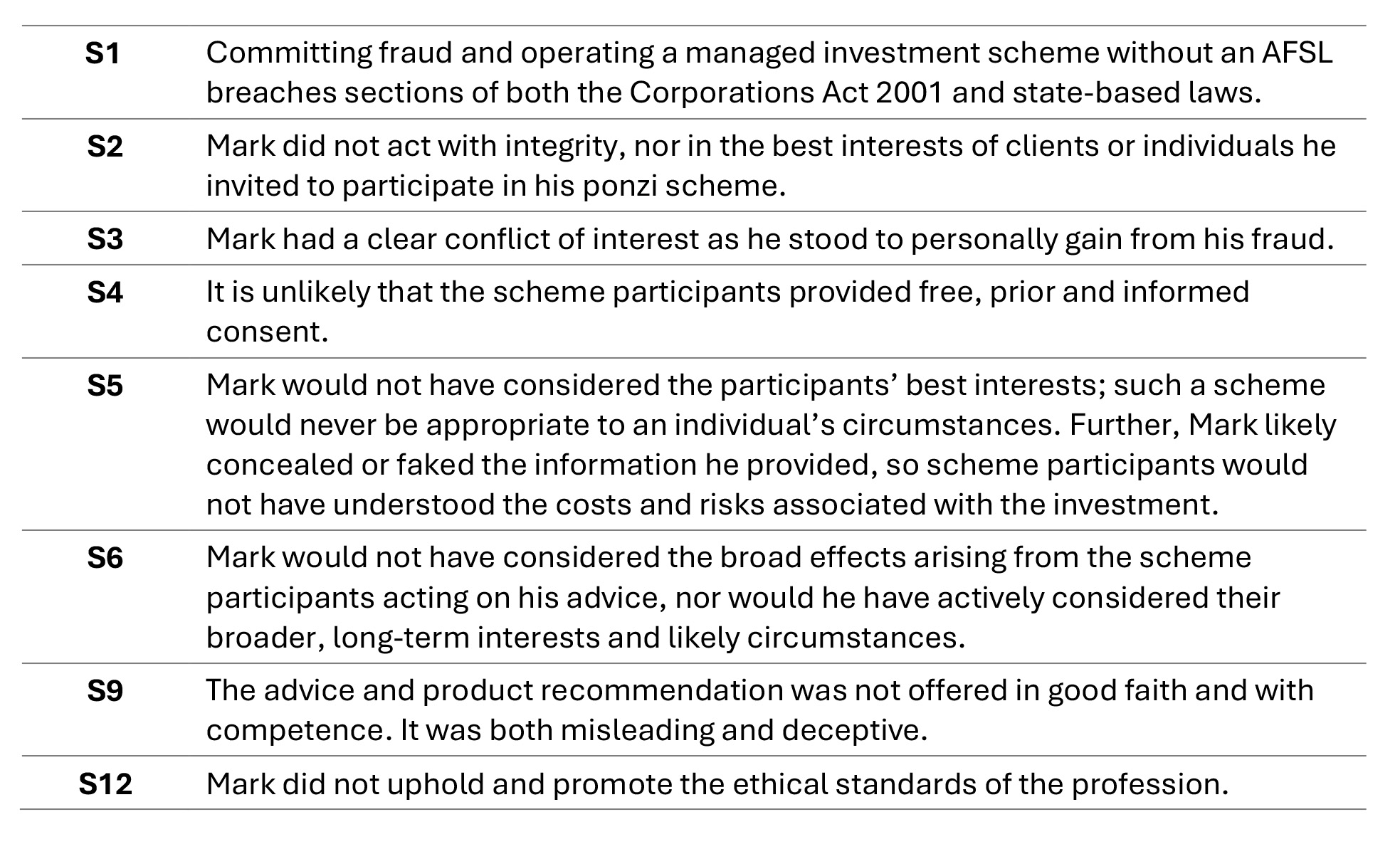

Case study one: The ‘mega returns’ fraud – ponzi scheme

In 2025, a long-running and significant ponzi scheme investigation reached its legal conclusion with the sentencing of Perth-based adviser Mark from ACME Advice. Between 2014 and 2019, Mark ran an unregistered managed investment scheme through his personal company, one that was unrelated to ACME Advice. However, he used his role as an adviser to promote his illegal scheme.

Mark targeted select high net wealth investors, many from his own social and community circles, promising ‘mega returns’ by supposedly leveraging international debt markets and high-yield private placement programs. In reality, no such investments existed.

The mechanics of the scheme

Mark operated a classic ponzi scheme. Instead of generating profit through market trading, he maintained the illusion of success by:

- Pooling investor money into personal and company bank accounts

- Paying ‘interest’ to early investors using the capital deposits of newer investors

- Building false trust; he provided investors with regular updates painting a positive picture of imminent massive payouts to discourage them from withdrawing their principal.

The investigation and collapse

The scheme began to unravel in 2019 when ASIC obtained asset preservation orders. In December 2020, the federal court ordered the winding up of the scheme and noted that it was operated by an entity that did not have an AFSL. The court appointed liquidators, with the primary role to identify, seize and sell Mark’s assets to distribute any remaining value to creditors.

Early in the investigation, it was revealed that while over $250 million had flowed through the scheme’s accounts, the majority had either been paid out to earlier investors as ‘returns’ or had been spent; this left a substantial gap between what was owed to investors and what was available.

Mark was eventually charged with more than 40 counts of fraud.

Verdict and sentencing

Most investors experienced substantial losses, with many unlikely to recover their full principal investment. Mark was found guilty of all counts of fraud, totalling nearly $35 million and relating to six specific investors. He was sentenced to 14 years in prison, with a non-parole period of 12 years.

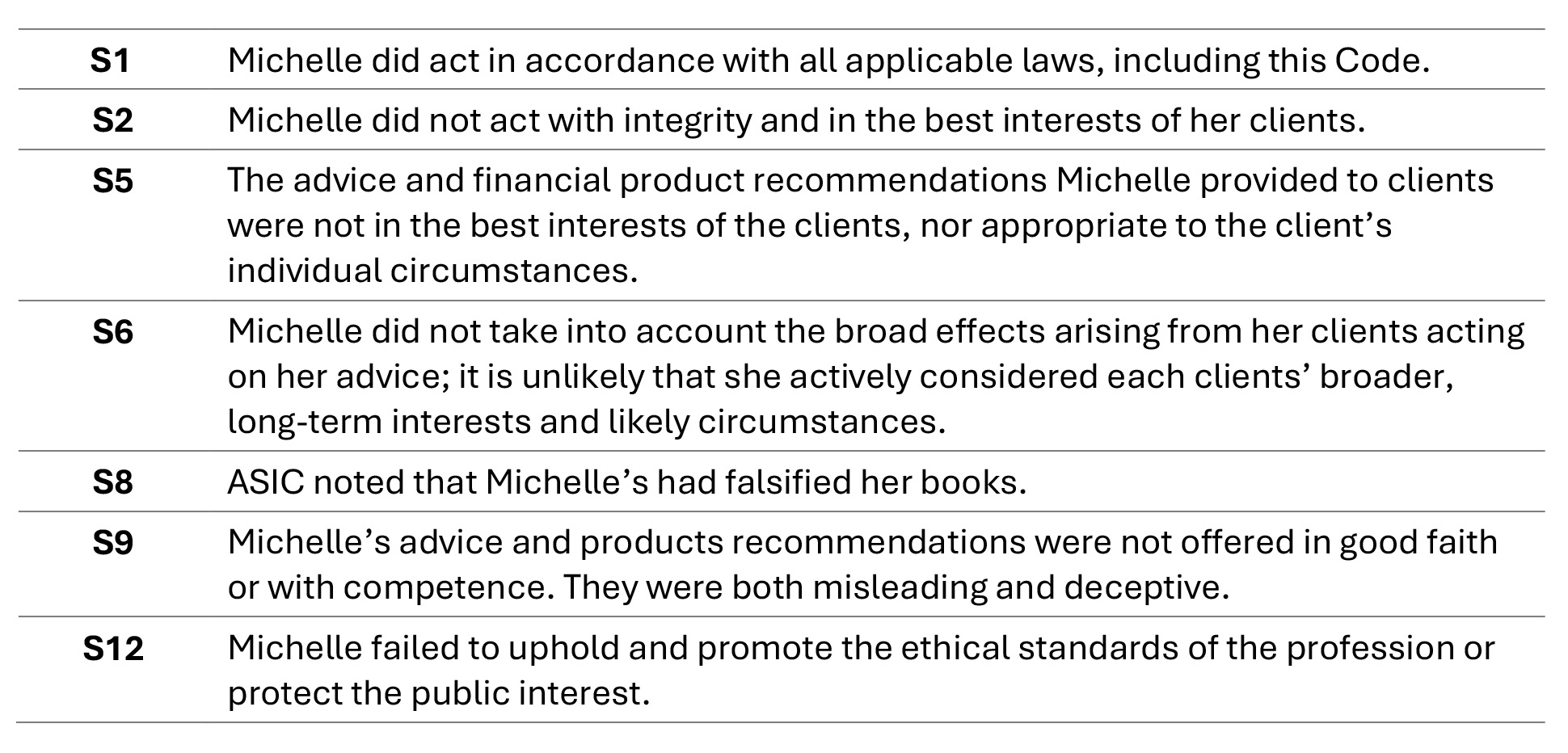

Mark’s actions saw him potentially breach several standards in the Code of Ethics, including:

Case study two: Fraud

Following an extensive ASIC investigation, adviser Michelle, director of ACME Investment and Coaching, currently faces criminal prosecution. The case centres on an unregistered investment scheme that allegedly defrauded investors of millions of dollars through misrepresentations and the improper handling of funds.

In March 2023, the federal court found that ACME Investment and Coaching was operating an unregistered managed investment scheme and carrying on a financial services business without a licence. It also noted the falsification of books relating to the company, specifically concerning the company’s annual returns.

The court ordered that the firm be wound up on just and equitable grounds. Liquidators found that the business had minimal legitimate revenue and exhibited the hallmarks of a ponzi-style structure.

The red flags noted by ASIC include:

- Promises of guaranteed high returns – Michelle allegedly enticed investors with promises of consistent, high-yield returns, often cited as being around 15% per annum

- The scheme was framed as a ‘private loan’ arrangement or part of a ‘wealth coaching’ program rather than a financial product

- A lack of legitimate revenue streams as identified by the liquidators; it was discovered that the company had no discernible business model or significant source of legitimate income

- Lack of an AFSL, which means no professional indemnity insurance, dispute resolution memberships (such as AFCA) or regular audits. Operating without an AFSL means investors have almost no regulatory safety net

- The scheme grew through social referral networking, word-of-mouth and social connections, which created a false sense of security and exclusivity.

The charges brought against Michelle include a combination of state-based criminal law and Commonwealth corporate regulations. In total, more than 20 counts of fraud relating to more than $4 million in investor funds. As well as charges under the state-based laws, Michelle faces additional charges under federal corporate law, including:

- Section 184 (5 counts): failing to act in good faith in the exercise of her powers and duties as a director. These charges relate to the use of approximately $2.5 million.

- Section 1307 (5 counts): Falsifying books relating to a company, specifically concerning the company’s annual returns.

While the case won’t be heard until later in 2026, potential penalties include:

- a maximum of 15 years’ imprisonment per offence in relation to Section 184

- a breach of Section 1307 carries up to five years per offence.

Michelle’s actions saw her potentially breach several standards in the Code of Ethics, including:

Case study three: Misappropriation of retirement savings

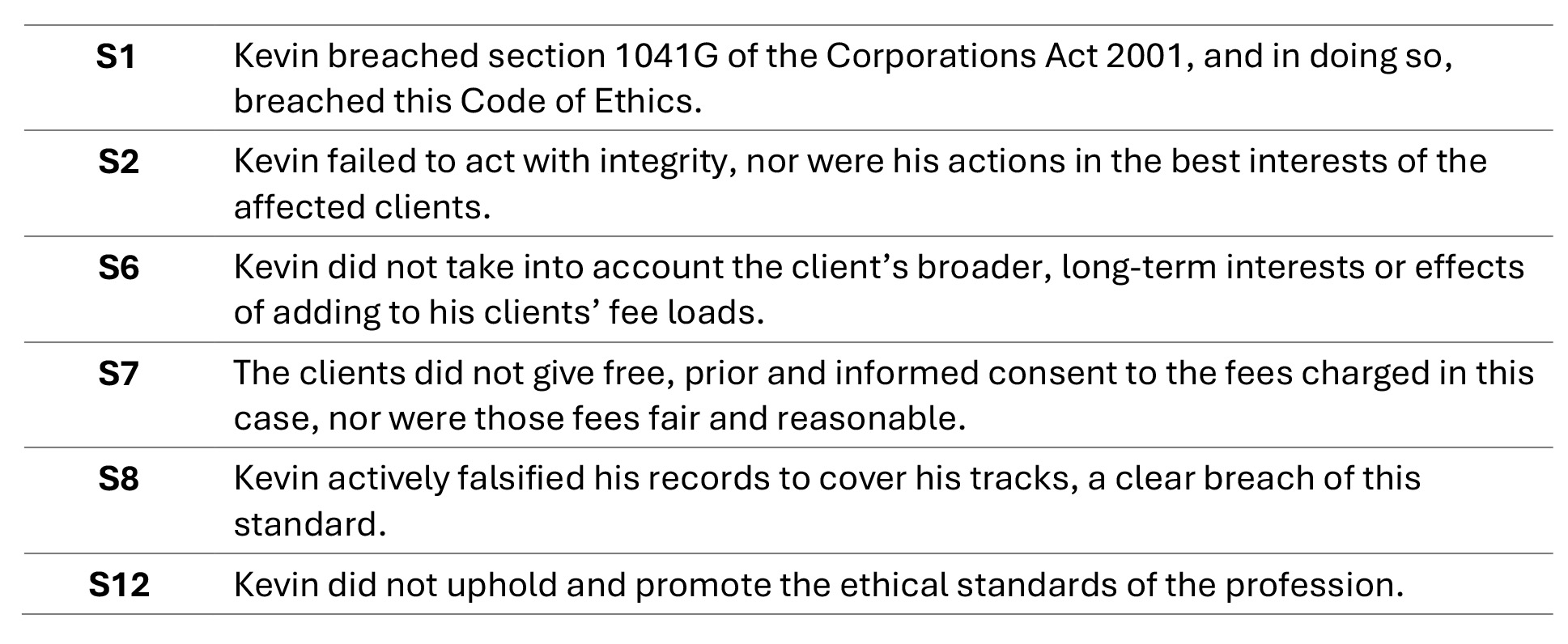

In early 2025, Kevin, former financial adviser and director of ACME Financial Freedom, was sentenced in relation to a scheme that targeted the retirement savings of his clients.

An ASIC investigation found that over 2019-2020, Kevin abused his position of trust to misappropriate funds from his clients’ superannuation accounts. He did this by submitting ad-hoc adviser fee forms to a specific super fund trustee. These forms purported to authorise the withdrawal of fees from his clients’ ACME Super superannuation accounts.

The clients had no knowledge of these fees, had never signed the forms and did not consent to the withdrawals. To cover his tracks, Kevin created fictitious client file notes that detailed non-existent conversations where clients supposedly agreed to the fees.

Kevin was prosecuted under the Corporations Act 2001 (Cth), specifically section 1041G, engaging in dishonest conduct in the course of carrying on a financial services business.

Kevin pleaded guilty to a consolidated charge of dishonest conduct and was sentenced to three years’ imprisonment, suspended on the condition of a five-year good behaviour bond. He was ordered to pay a $20,000 pecuniary penalty and make full reparation to the trustee for the money stolen.

Kevin’s actions saw him potentially breach several standards in the Code of Ethics, including:

The preservation of the industry’s integrity is a collective mandate. From regulatory bodies to individual practices, every stakeholder must be a guardian of the highest ethical standards. By proactively confronting ethical dilemmas and rooting out criminal conduct, the profession can secure a future where financial advice is defined by an unbreakable bond of trust, transparency and accountability. This is good for advisers, consumers and the industry as a whole.

Take the FAAA accredited quiz to earn 0.75 CPD hour:

CPD Quiz

The following CPD quiz is accredited by the FAAA at 0.75 hour.

Legislated CPD Area: Professionalism & Ethics (0.75 hrs)

ASIC Knowledge Requirements: Ethics (0.75 hrs)

please log in to start this quiz

———

Notes:

[1] ASIC Media Release: ASIC’s annual report reveals strong growth in enforcement action and investigations and keen focus on strengthening markets, October 2025

[2] https://asic.gov.au/about-asic/asic-investigations-and-enforcement/asic-s-approach-to-enforcement/

CPD Quiz

The following CPD quiz is accredited by the FAAA at 0.75 hour.

Legislated CPD Area: Professionalism & Ethics (0.75 hrs)

ASIC Knowledge Requirements: Ethics (0.75 hrs)

please log in to start this quiz

———

Notes:

[1] ASIC Media Release: ASIC’s annual report reveals strong growth in enforcement action and investigations and keen focus on strengthening markets, October 2025

[2] https://asic.gov.au/about-asic/asic-investigations-and-enforcement/asic-s-approach-to-enforcement/

Have feedback on this article? Contact Us

Earn CPD Points

CPD: The spectrum of growth

CPD: The spectrum of growthCompanies that generate strong, sustainable growth are valuable sources of long term capital appreciation in a portfolio, but these businesses are rare, difficult to identify and exist on a broad [...]

CPD: Record-keeping in financial advice – the key to compliance and consumer protection

CPD: Record-keeping in financial advice – the key to compliance and consumer protectionIntroduction The financial services regulatory framework is a key pillar of financial consumer protection. Regulatory compliance is therefore not merely about avoiding penalties, but is a critical step in building [...]

CPD: Trust and ethics in financial advice

CPD: Trust and ethics in financial adviceIn 2024, trust in financial advisers reached an all-time high. This article, proudly sponsored by GSFM, explores the inseparable links between trust and ethical practice when providing financial advice. Defined [...]

CPD: Retirement Income Strategies

CPD: Retirement Income StrategiesIt has been almost 40 years since award superannuation was introduced in Australia, and 33 years since the introduction of mandatory occupational superannuation. This means the next decade will see [...]

CPD: Free cash flow works

CPD: Free cash flow worksThe difference between earnings and free cash flow is an important investment concept, one explained here by GSFM’s investment partner TD Epoch. Earnings have long played a dominant role in [...]