Key to private markets is understanding the opportunities and the risks

Dugald Higgins

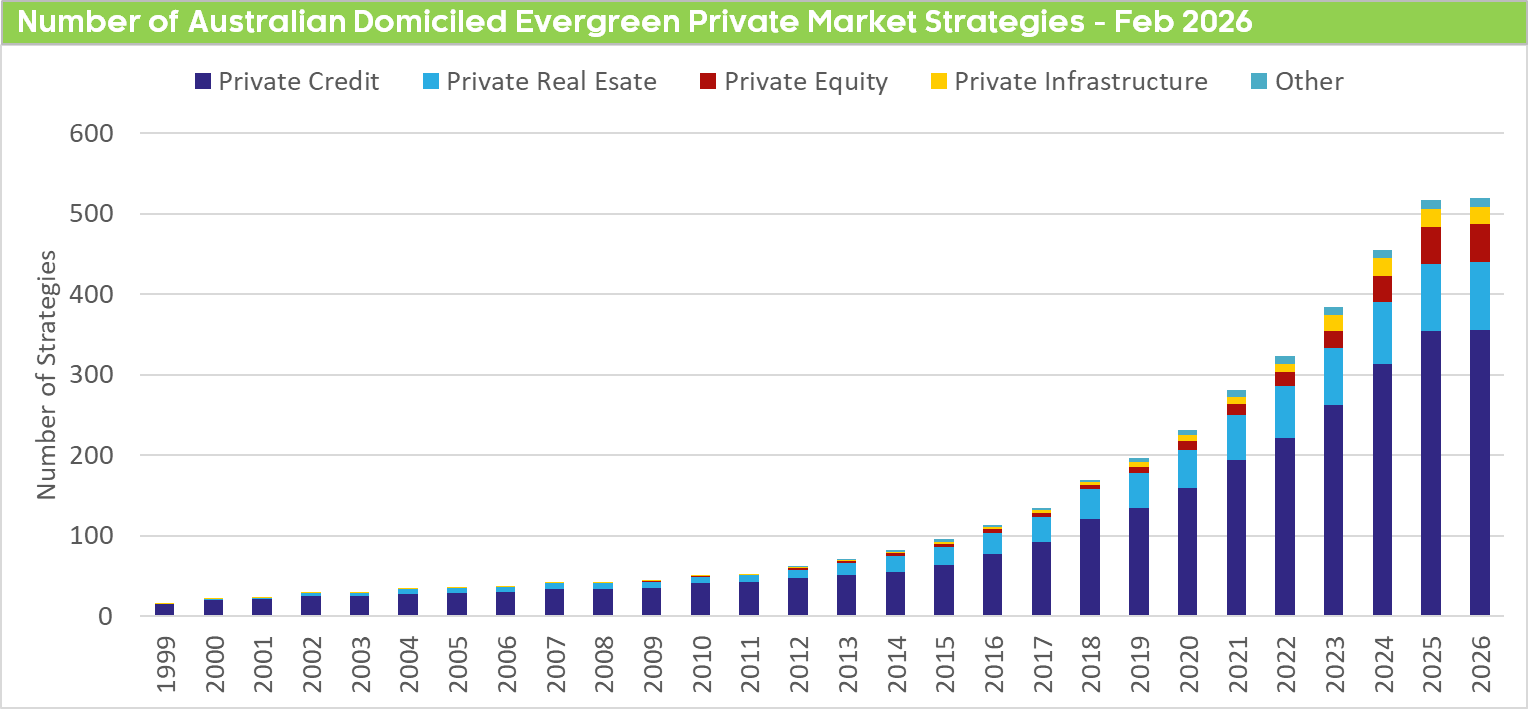

Once exclusive to large institutions, inflows to private markets funds have been strong as investors flock to access well-performing asset classes such as private equity, credit, infrastructure and property. But while these structures provide exposure to those markets, Dugald Higgins, head of responsible investment and real assets at Zenith Investment Partners, says investors also need to be aware of the liquidity constraints of the asset class.

“The industry has experienced a period of real growth, which is typical of the later stages of a market cycle. But now we’re reaching the point where investor expectations around access to capital will meet the reality that many private market assets simply can’t be sold quickly,” Higgins says.

“Private assets are less traded, less transparent, and often require active, hands-on management to realise value. Natural liquidity stems from the underlying assets, not the fund structure.

“This shouldn’t be a disincentive to pursue attractive opportunities, but it should be done in a way that doesn’t make your portfolio vulnerable to shocks.

“Private market funds often look smoother than listed markets because assets aren’t priced daily. But that doesn’t mean the underlying value isn’t changing. When valuations are revised, this can force a market adjustment – and fast.

“Illiquidity shouldn’t come as a surprise to investors. But they often seem to forget its implications when navigating market turbulence and portfolio rebalancing. Liquidity gives asset allocators free reign to adjust to market conditions. Private markets are by nature unwieldy. Failure to critically assess these implications usually leads to disorderly behaviour when the market turns, as we are starting to see in some areas, particularly offshore. The winners will be not just those who’ve planned to navigate through these periods, but can take advantage of pockets of market dislocation.”

Andrew Yap, head of portfolio solutions at Zenith, says despite these risks, private markets remain an important component of diversified portfolios, particularly in sectors such as infrastructure and real estate.

Improved fund structures, greater platform capability, and growing adviser sophistication have steadily lowered the barriers to entry. What was once operationally complex or structurally inaccessible in private markets, is increasingly being delivered in investable formats suitable for diversified portfolios.

“For investors, allocations to private markets are best viewed as complementary exposures designed to sit alongside daily liquid portfolios, not replace them.

“The benefits of private markets don’t come without trade-offs – specifically, liquidity. Unlike daily-liquid portfolios, private market strategies typically offer periodic redemption windows, structured to align investor liquidity with the underlying assets. Illiquid assets require patient capital, and portfolios are more resilient when redemption terms reflect that reality.

Yap emphasised the critical role of deep investment research and experienced portfolio managers in incorporating private markets into client portfolios.

“You can’t assess liquidity risk, unintended portfolio biases or volatility exposure without sophisticated systems – you need to drill into the underlying holdings and understand how a portfolio would behave under stress,” he says.

Yap says investors considering private markets should go in with eyes wide open.

“Over the long term, private market funds have delivered solid returns. But investors should go in understanding that their money may be tied up for longer than they initially expect, and those funds may not always be available when they want it.”