AI powers corporate rebound as cost pressures rise and geopolitical risks intensify – Fidelity International 2026 Analyst Survey

Niamh Brodie-Machura

Companies entered the year feeling better than at any point since the chaotic aftermath of the Covid pandemic, driven by a once-in-a-generation investment boom in artificial intelligence (AI).

These are the central findings of Fidelity International’s 2026 Analyst Survey[1], capturing insights from more than 120 equities and fixed income analysts, based on over 20,000 meetings with company management teams worldwide. The survey captured sentiment through early March; since then, the prolonged conflict in the Middle East, including escalating attacks on energy infrastructure, has introduced a more persistent cost and inflation shock that is shaping the near-term macro backdrop.

While corporate sentiment has strengthened, the survey also highlights emerging pressures beneath the surface. Elevated raw material costs and slowing wage growth are placing pressure on consumers, creating downside risks for the global economy. At the same time, the Middle East conflict has shifted from a headline risk to a supply disruption that tightens physical availability and raises prices, with the risk that prolonged disruption could sustain these pressures for longer than previously expected.

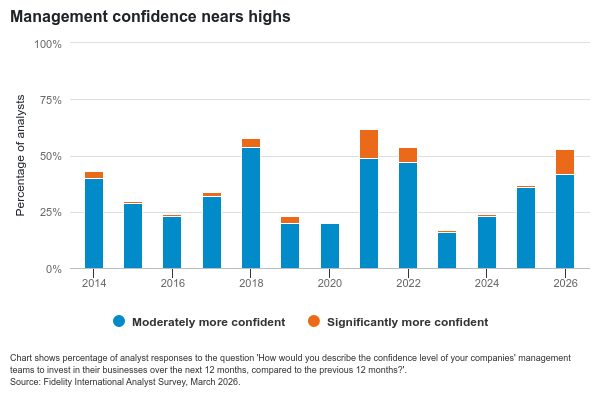

AI investment broadens

The survey shows the proportion of analysts reporting greater management confidence in business investment over the coming year has climbed back toward post-pandemic peaks.

Analysts are clear on the source of that optimism. The global economy is in the midst of one of the largest investment cycles in years, driven by spending on artificial intelligence and the infrastructure required to support it.

Niamh Brodie-Machura, CIO, Equities at Fidelity International comments: “Our global analyst team’s company-level insights show this is not just a narrow technology rally. AI investment is cascading through power and industrial supply chains, extending the cycle beyond the largest tech platforms.”

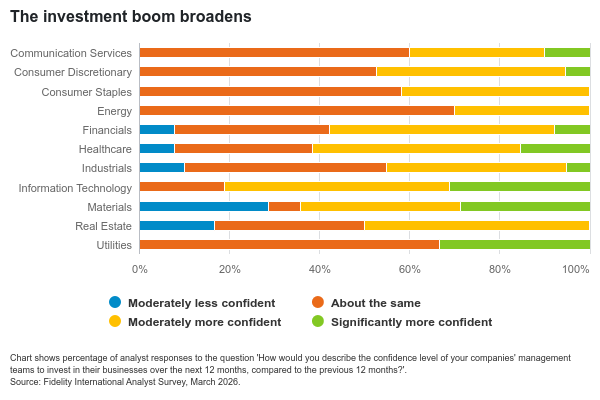

That investment is bolstering demand across supply chains and extending revenue visibility for years ahead. Information technology is the clearest beneficiary, but the effects are also visible in materials and energy, where demand for power and the commodities needed to construct datacentres and expand generation capacity is driving a boom in several areas.

Some 81 per cent of IT company managers are moderately or significantly more confident about the year ahead, alongside 65 per cent in materials.

Sam Heithersay, Portfolio Manager, at Fidelity International comments: “The initial phase of this AI rally has been dominated by investment in compute and data centres to the benefit of a narrow set of offshore tech companies but the productivity dividend of this investment is likely to be much more distributed as companies embed AI into workflows to drive operational efficiency. Australia is well placed to benefit from this AI diffusion and we have conducted our own company survey work to better understand which ASX companies are most mature in their AI adoption as we think AI can reset long-held competitive advantages.”

Costs remain a constraint

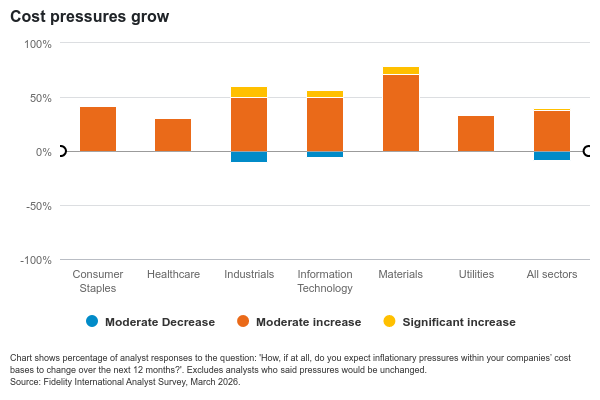

Yet the survey also highlights mounting pressure on corporate cost bases. Only 8 per cent of analysts expect inflationary pressures to ease over the next 12 months. Around half anticipate costs pressures will remain at current levels, while 40 per cent foresee further increases. Materials and industrial sectors report particularly strong upward pressure.

Higher raw material prices, energy costs and trade frictions, intensified by geopolitical tensions, are sustaining supply-side inflation and adding to pressure on demand.

Justin Teo, Investment Analyst, Equities at Fidelity International comments: “The Reserve Bank of Australia increased interest rates by 25 basis points at each of its last two meetings in February and March, leading to a cash rate of 4.10 per cent. This is contrary to some central banks around the world that are looking to cut rates in 2026. Supply-side inflation – in particular oil and gas – has increased the probability of higher interest rates globally due to inflation concerns. Finding companies with pricing power will be critical for investors as these companies are more likely to maintain margins, as was the case during the COVID related supply-chain inflation period over 2020-22.”

Fidelity’s quarterly indicators also show expectations for labour cost growth moderating to their lowest level in three years. The divergence between sustained input costs and softer wage momentum raises concerns about household purchasing power.

Sam Heithersay comments: “Australia is a relatively high-cost jurisdiction, labour costs increased materially post-Covid and are sticky downward so remain above pre-Covid norm. Company management seems resigned to a higher for longer cost base given low unemployment and a skills shortage. Australia’s resources exposure provides a partial offset to this persistent inflation as commodities have historically provided a natural hedge against global cost inflation.”

A widening divide

For analysts covering consumer staples and discretionary companies, affordability and demand risks are now the primary concern. While AI-exposed industries benefit from capital markets strength and infrastructure spending, middle-income consumers face rising fuel costs and limited wage growth. Healthcare analysts similarly point to fiscal trade-offs as governments increase defence spending, potentially intensifying pressure on public healthcare budgets.

The result is an increasingly uneven economic landscape. Companies tied directly to AI infrastructure are seeing confidence, capital deployment and expected returns improve. In contrast, sectors dependent on stretched consumers or exposed to political pricing pressures face tighter margins and demand headwinds.

Niamh Brodie-Machura comments: “The investment backdrop is supportive, but it is becoming more selective. Companies with pricing power, strong balance sheets and exposure to AI are positioned differently from those reliant on stretched consumers. As the gap between winners and losers widens, detailed fundamental research and active stock selection become increasingly important. Against a more volatile geopolitical backdrop, the survey’s overall message remains that AI investment is reshaping the corporate cycle. The breadth of spending across infrastructure and supply chains suggests that the impact extends beyond technology giants. However, the interaction of prices, politics and wage dynamics means the benefits are not yet evenly distributed, reinforcing signs of a K-shaped global economy.”

Justin Teo adds: “The K-shaped economy seen in the United States is also present in Australia where people in the top quartile of income are experiencing positive wealth effects from asset price inflation, whereas people in the bottom quartile are experiencing tighter household budgets due to limited wage growth and cost inflation for necessities like groceries and fuel. What’s unique to Australia is interest rates have been rising, so consumers with mortgages are facing higher servicing costs and lower disposable income, whereas retirees who have no mortgage and invest largely in term deposits are experiencing greater disposable income. This is a tough environment for consumer discretionary stocks.”

———–

Notes:

[1[ https://www.fidelity.com.au/learning-hub/analyst-survey/ Source: Fidelity International 2026 Analyst Survey. The survey was conducted 20 Feb – 2 March 2026, with follow-up interviews with the team following the start of the Middle East conflict. The survey features responses from 122 analysts around the globe.