Michael Goosay

Policy, conflict, and credit

At the start of the year, the macro environment was defined by resilient growth and moderating inflation—supporting expectations for gradual Fed rate cuts. Combined with attractive starting yields, this created a constructive backdrop for fixed income. That outlook has shifted with the escalation of conflict in the Middle East. With inflation still running above the Fed’s target, higher energy prices risk limiting the Fed’s ability to respond if growth slows or labor market conditions weaken. For now, economic growth and credit fundamentals remain intact, but the path forward is less certain. Despite heightened volatility, investor demand for income and portfolio ballast has not abated. While the conflict has pushed rates higher and modestly widened credit spreads, elevated yields provide improved compensation and support continued allocations to bonds.

1. Policy volatility: Navigating geopolitical and economic challenges

The current environment is marked by geopolitical volatility, as markets grapple with the war in Iran, surging oil and gasoline prices amid already sticky inflationary pressures, and a complicated U.S. labor market. The Fed’s easing cycle, occurring amid sustained inflation exacerbated by geopolitical tensions (with Iran now top of the list), creates a backdrop of uncertainty. This scenario complicates investor sentiment and contributes to a steepening yield curve. While this creates opportunities for agile investors, it also calls for close risk monitoring.

2. Credit fundamentals: Resilience amidst market dynamics

From a credit perspective, resilience is key. Investors should maintain a focus on robust technicals and credit fundamentals while remaining attentive to the overall economic conditions. Companies still have healthy balance sheets, and earnings are running above expectations. Nevertheless, geopolitical headline risks, primarily the war in the Middle East, and lingering trade sensitivities can lead to significant sector dispersion, underscoring the importance of active issuer selection and credit discipline.

3. Valuations: Spreads widen in response to the Iran war and supply

Valuations present a complex picture as spreads widened in the first months of the year, driven by a surge in new issuance and uncertainty surrounding the war in Iran. While further spread widening is possible as the war continues, opportunities persist, especially within municipal bonds, investment-grade credit, and high yield. As geopolitical and Fed policy uncertainty continue, careful security selection is critical. In this environment, disciplined active management will be essential to identify durable income, manage downside risks, and capture pockets of value amid ongoing volatility.

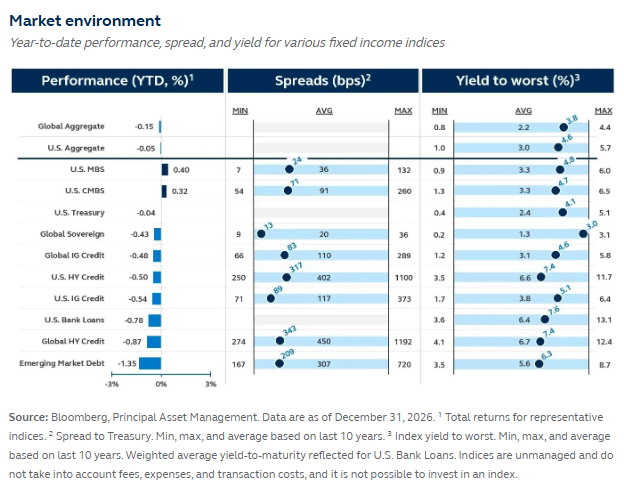

Global outlook

The escalation in the Middle East has introduced a new layer of uncertainty into the global macro backdrop, creating competing forces for markets and policymakers. Higher energy prices are inflationary in the near term, but also risk weighing on growth—particularly in energy-importing regions such as Europe and Asia.

At the same time, governments are likely to increase fiscal spending to support energy markets and domestic economies, adding pressure to already stretched public finances. For central banks, this creates a difficult balancing act: inflation argues for patience, while slowing growth supports eventual easing.

The result is likely a period of policy inertia and heightened dispersion across regions and asset classes. In this environment, maintaining flexibility, emphasising income, and managing downside risks remain key as geopolitical developments continue to unfold.

Investment implications

While economic challenges remain, we see opportunities in fixed income.

Investment grade credit

Investment grade credit remains well positioned despite a surge in issuance. While supply has been elevated, demand has kept pace, supported by attractive all-in yields and a broad investor base. Strong order books and continued access to global funding markets have helped the market absorb large deals efficiently.

Treasury yields remain a key anchor, particularly at the intermediate and long end of the curve. Even if policy rates decline, yields in the five- to ten-year segment should remain supported, offering compelling carry and income opportunities.

Fundamentals also remain solid, with corporate earnings holding up and balance sheets generally healthy. Against this backdrop, opportunities are concentrated in high-quality issuers and sectors with durable fundamentals, while more cyclical areas warrant greater selectivity.

High yield credit

High yield is entering a cautiously constructive but uncertain environment. Elevated starting yields in the mid-to-high single digits provide a strong income cushion and remain a key driver of return potential, even if spreads remain rangebound.

At the same time, spreads are increasingly sensitive to macro and geopolitical developments. Ongoing tensions in the Middle East and evolving rate expectations could lead to periods of volatility, with risk assets vulnerable to further repricing if uncertainty persists.

Selectivity is becoming more important across sectors. Consumer-facing industries face pressure from higher energy costs and persistent inflation, while more defensive areas and certain infrastructure-linked sectors offer relative stability. Primary market opportunities may also provide attractive entry points.

Overall, a disciplined, selective approach remains critical in the current environment.

Securitised debt

Securitised debt enters the quarter on a balanced footing, supported by steady demand and generally solid fundamentals, even as rate volatility and geopolitical risks persist.

Mortgage-backed securities remain a key focus. Agency MBS performance has been sensitive to rate moves, with prepayment risk a central consideration, particularly if rates decline meaningfully. In non- agency markets, improving affordability and selective refinancing activity are supporting credit performance, with opportunities in higher-quality and structurally protected segments.

Across consumer credit, performance is diverging by income cohort. Higher-income borrowers remain resilient, while lower-income segments face pressure, contributing to elevated delinquencies in areas such as subprime auto.

Elsewhere, CMBS fundamentals are stabilising, while CLOs face mixed conditions. In this environment, careful security selection and disciplined underwriting remain essential.

Municipal bonds

Municipal bonds enter the coming quarters with a strong income profile and defensive characteristics, supported by robust demand and solid credit fundamentals. Tax-exempt yields remain compelling on an after-tax basis, continuing to attract both retail and institutional investors even as issuance stays elevated.

Supply has been concentrated in longer maturities, contributing to a steeper curve and enhancing income opportunities for investors willing to extend duration. The intermediate-to-long end of the curve offers particularly attractive compensation relative to other fixed income sectors.

Credit quality across the market remains generally stable, with many issuers benefiting from diverse revenue streams tied to essential services. While certain credits face localised fiscal pressures, municipals overall continue to offer resilience.

In this environment, municipals stand out as a reliable source of tax-efficient income with defensive portfolio benefits.

Emerging market debt

Emerging market debt faces a more uncertain backdrop as geopolitical tensions and higher energy prices reshape inflation, policy, and investor behaviour. A higher structural oil price is likely to persist, creating inflationary pressure and limiting central bank flexibility across many emerging economies.

The impact is increasingly uneven across regions. Commodity exporters, particularly in Latin America and parts of Africa, may benefit from improved fiscal and external balances, while energy importers face rising costs, weaker growth, and currency pressure. Fiscal dynamics are also becoming more challenging as governments respond to higher energy prices with subsidies and support measures.

Despite these headwinds, investor demand for yield remains supportive in the near term. However, flows are likely to concentrate in higher-quality issuers, leading to greater dispersion and a more differentiated opportunity set across markets.

Private credit

Private credit is approaching an inflection point, with strong demand and attractive deal flow set against rising scrutiny and emerging structural risks. The asset class continues to benefit from durable borrower fundamentals and steady capital inflows, particularly in middle-market lending.

However, dispersion across managers is becoming more pronounced. In some areas, looser underwriting, higher leverage, and strategy drift have introduced vulnerabilities, particularly among larger platforms and vehicles facing liquidity and valuation pressures. Recent dislocations have highlighted the importance of structure and alignment.

At the same time, market conditions are shifting in favour of lenders. Terms and pricing have become more attractive, and core middle-market direct lending continues to offer a consistent pipeline of opportunities.

The long-term case for private credit remains intact, but outcomes will increasingly depend on manager discipline and underwriting quality.

By Michael Goosay, Chief Investment Officer