The Ukraine-Russia crisis recently moved to the forefront of investors’ thoughts as Moscow mobilized its military power to influence developments in the autonomous Crimean peninsula.

Russia’s incursions into the Ukraine have been condemned around the world, have caused a steep sell-off of the Russian rouble and equities and have hurt financial markets in other central and Eastern European markets. However, any measures taken to isolate Russia from the global community will affect European countries more than the US given the former region’s closer economic ties with Russia, and especially given that Europe is only just emerging from recession. Russia has at least taken a step back from the brink by pulling some of its troops back to base and saying that it will only use the military as a last resort. Markets reacted positively but this story has definitely not gone away.

Ukraine’s economic problems remain a concern

While markets believe that the turmoil in Ukraine is unlikely to have broad-based implications for emerging markets (EM), any default in the EM world would prompt negative headlines. Certainly, the confrontation between Ukraine and Russia has distracted investors from a potential EU/IMF rescue deal for Ukraine, where there is a pressing need to address the US$13bn of debts (including obligations from the state-owned gas company Naftogaz), which are due to be repaid this year. Asian markets are not ignoring the possibility that the situation in the Ukraine will deteriorate.

Investors were quick to seek default protection, which resulted in a strengthening in Asian credit default swaps, or CDS, (i.e. the cost of buying protection against default rose). In China, the official PMI for February once again weakened, reinforcing the view that the slowdown in China will dominate 2014. Also in China, the government has successfully orchestrated two-way volatility in renminbi (RMB) trading. It has weakened the currency through its daily fixing mechanism, triggering a fall of more than 1% in both CNY (RMB traded onshore) and CNH (RMB traded onshore) over the past few weeks. This move is widely interpreted as a government warning to currency speculators following huge investment and trade flows backing the apparently one-way bet for the RMB to appreciate.

Despite the unsettling macro headlines, Asian fixed income markets have proven resilient recently. The hard currency J.P. Morgan Asia Credit Index returned 0.57% during the week ended 28 February (when the Ukrainian crisis broke) with Indonesian US$ bonds outperforming. The sudden return of investment flows to the once-troubled Indonesian market was reportedly due to EM funds seeking refuge from emerging Europe amid the Ukraine crisis. Similar performances were also seen in the local currency market where the Indonesian local currency bond market was the best performer in the week ending 28 February, returning 1.53% (this includes one percentage point of IDR appreciation). Overall, the local currency Citi Asian Government Bond Investable Index gained 0.61% during that week, and ended the month of February with an impressive 2.9% total positive return.

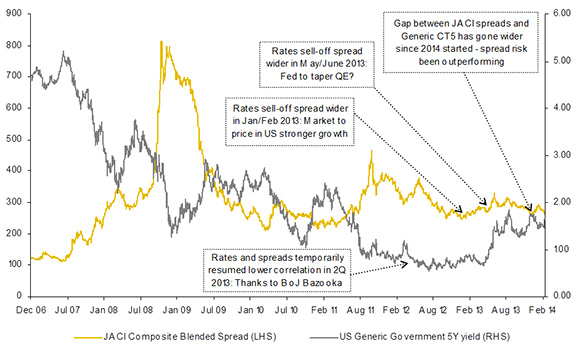

Figure 1: J.P. Morgan Asia Credit index (JACI) blended spread vs. US 5-year yield

Crowded calendar of political events ahead in 2014

Other notable newsflow came from Thailand where more negative headlines were generated by the rice purchasing scheme scandal. The continuing investigation by the anti-corruption body could lead to the Prime Minister being removed from office, while domestic violence continues to affect Bangkok. In addition, the 2014 presidential election in Indonesia has come to life with the incumbent Democratic Party conducting its presidential-nominating convention to boost the popularity of potential candidates such as Dahlan Iskan, the minister of state-owned enterprises. The reformist and current Jakarta governor Joko Widodo of the PDIP is likely to be the front runner if he is put forward as the party’s official contestant. Finally, politics has returned to the centre stage in India where 11 small political parties have joined forces (the up-and-coming, newly-formed AAP, however, is absent) to form a third-front to wrest power from the popular-opposition BJP and the underdog-governing Congress party.

Asia to see a correction?

Lately, the market has faced many “on-the-brink-of” situations. Ukraine appeared on the brink of civil war and Russia’s aggressive intervention in Crimea, and the uncertainty surrounding the Ukraine’s economic and financial position means it is still close to disaster. Meanwhile, the opaqueness of Chinese government policies towards interest rates and currencies means investors are close to resetting their consensus views (especially in terms of the currency) and perhaps resizing their investment allocations to China. Given the challenges facing Europe, China and the US, Asian fixed income markets are likely to experience some form of correction following the robust performance seen in February. We will monitor developments closely and use our active approach to exploit any opportunities created by further volatility.

Commentary by Clifford Lau, Head of Fixed Income, Asia Pacific