Does debt matter? The diverging tales of the eurozone and the emerging markets

Bond markets are full of surprises. Core government bonds have been one of the strongest performing asset classes in 2014, propelled in part by worrying signs of emerging market stress.

Emerging market (EM) debt has suffered relentlessly for nearly a year, scant reward for those emerging economies that spent most of the last decade bolstering their finances. Meanwhile, in the eurozone, Greece, Portugal, Spain, Italy and Ireland are among the world’s most indebted countries, and yet their bond markets have witnessed one of the most explosive rallies in history. Is this fair, and what explains this dichotomy?

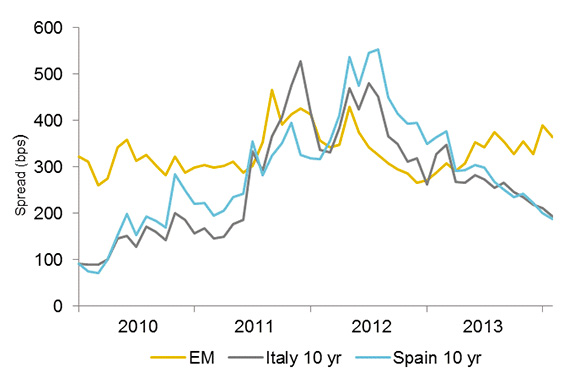

Figure 1: Peripheral bond spreads vs. EMD bond spreads

Source: Bloomberg, February 2014. EM denotes the spread on the JPM EMBI Global Index. All the periphery plots show the spread between the periphery country’s 10-year yield and the 10-year Bund.

Source: Bloomberg, February 2014. EM denotes the spread on the JPM EMBI Global Index. All the periphery plots show the spread between the periphery country’s 10-year yield and the 10-year Bund.

In reality, the stock of debt is a poor indicator of the level of interest rates, sovereign default risk, or the near-term likelihood of a debt crisis. More important is the type of debt (external vs. internal) and factors affecting the ability of a country to refinance. If we are to assess whether EM debt is a crisis-in-the-making, or whether the eurozone periphery is overvalued, we must first ask: how much debt is too much debt?

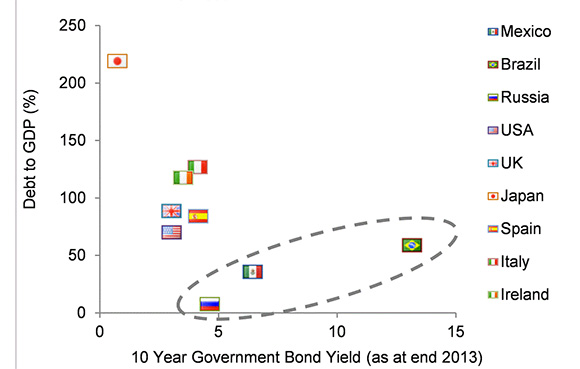

Figure 2: Debt-to-GDP ratios versus bond yields

Source: Bloomberg. For some countries, debt-to-GDP calculated using 2012 GDP as 2013 data not available at time of writing. For Brazil, the 2023 government bond yield has been used.

An elevated level of external or foreign currency debt is the poison that undermines sovereign debt stability. The lesson of emerging markets historically is that excessive foreign-denominated debts grow more ominous in the face of domestic deterioration. As strains grow, the accompanying currency devaluation makes these debts increasingly expensive to service. The combination of domestic weakness and higher debt burdens created a toxic and self-reinforcing downward spiral, ultimately imploding when foreign creditors turned off the lending taps.

Debt denominated in domestic currency is a different matter. The solution here is easier, as it requires policymakers to simply create more money, buying their own debt if necessary. Default can be averted but often at the expense of currency debasement and other economic side-effects such as inflation.

The toxic external debt dynamic is mostly absent today. We do not see an EM debt crisis unfolding. Economic rebalancing has reduced EM reliance on external debt, domestic conditions are more stable, and in many cases reserves have ballooned.

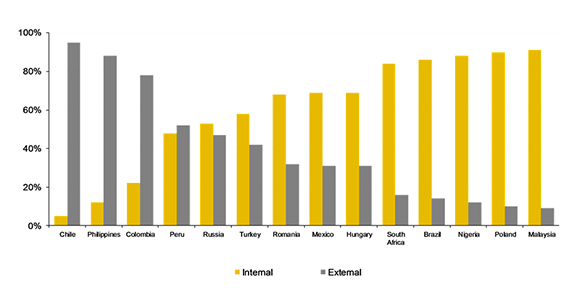

Figure 3: Aggregate amount of internal vs. external debt for EMs

Source: Threadneedle, January 2014. Based on countries which are present in both the JPM GBI EM (local currency debt) and JPM EMBI Global (external credit) indices and then comparing the dollar equivalent outstanding/face value debt amount.

Source: Threadneedle, January 2014. Based on countries which are present in both the JPM GBI EM (local currency debt) and JPM EMBI Global (external credit) indices and then comparing the dollar equivalent outstanding/face value debt amount.

This is not to say the recent EM sell-off is unfounded. Idiosyncratic risks are extreme in some regions such as Argentina, Venezuela and Ukraine. In others, such as the BRICs, rapid credit growth and misallocation of capital have fostered broken economic models that are now in desperate need of structural reform. There is more work to do, but the likely release valve in this cycle should be weaker currencies rather than crisis and default. Much of this adjustment is already behind us.

The eurozone is an entirely different matter. The region in aggregate does not have a serious debt problem, but individual countries most definitely do. In a robust monetary union, this would have been easily overcome via reflationary policies. Central banks can address liquidity problems through reflationary policies, which allow countries such as Italy and Spain to go on refinancing their enormous debt loads. The ECB was always going to struggle with Greece and Cyprus; even central banks cannot rectify true insolvency. But the ECB’s mistake was that it nearly allowed liquidity problems to morph into a solvency crisis. Nearly all eurozone debt is denominated in domestic currency – euros. By exposing deep fissures within the EMU, policymakers allowed the market to price peripheral debt as external debt. Speculation of a eurozone break-up and debt restructuring were evidence of the lack of faith in the monetary union.

In July 2012, Mario Draghi made his famous proclamation that the ECB would do ‘whatever it takes’ to preserve the euro. The ECB followed up with its programme of Outright Monetary Transactions (OMT). Draghi later labelled this, rather immodestly, as one of the greatest monetary policy tools ever crafted. He was right. In one fell swoop, the ECB managed to switch trillions of debt from being perceived as ‘external’ debt to ‘domestic’ debt. And with that change, default premiums in the eurozone debt rightfully plummeted. Rapid improvement in the balance of payments, less draconian austerity measures, and lower debt costs have since contributed to a now self-reinforcing cycle of improvement.

Eurozone economic sentiment is now on the mend. GDP will likely creep higher this year on the heels of broad-based but modest improvement in the weaker countries. The irony is that this modest recovery is perceived by markets as the ‘all-clear’ sign that eurozone debt problems are rapidly receding. A brighter growth outlook is certainly encouraging, but growth is not the key driver of investment returns in debt deleveraging events. Rather, it is typically the last piece of the jigsaw to fall into place. Modestly positive growth will make little or no difference to the debt sustainability of the indebted eurozone countries. Most of these look considerably worse than a majority of emerging market economies on most debt metrics, and this is not going to change.

It is difficult to identify tipping points in debt accumulation, but two critical factors portending crisis are the level of external debt and the actions of policymakers. European sovereign debt has performed phenomenally well precisely because it addressed both issues simultaneously. The ECB replaced policy ineptitude with policy magic by reassuring markets that eurozone debt was local debt. As long as there is no reason to doubt the sanctity of the eurozone going forward, the dreadful debt metrics of its weaker constituents will remain dormant concerns. The rally in peripheral debt has been justified. Sadly, that rally is almost over. Misplaced confidence fuelled by a better growth outlook may allow for an overshoot, but there is no hope for an immediate sustainable debt solution and spreads now offer little excess compensation.

Whereas euro countries snatched victory from the jaws of defeat, emerging economies have accomplished the opposite feat. Growth and strengthening finances have given way to excessive credit growth and a desperate need for structural reform. Aggregate debt levels, however, remain largely under control. Manageable debt levels should preclude a widespread crisis, allowing weaker currencies to bear the brunt of adjustment. Buying opportunities will abound in the coming year, but it may be necessary to dodge the occasional policy-induced catastrophe along the way.

Commentary from Jim Cielinski, Head of Fixed Income, Threadneedle Investments