Weekly market & economic update – week ending 4 April, 2014

07

Apr

2014

From Shane Oliver - AMP chief economist

Investment markets and key developments over the past week

- The past week has seen gains in share markets and a further increase in bond yields on the back of mostly good economic data, dovish comments from central bankers and some lessening of risks regarding Ukraine. As a result the grind higher in share markets is continuing. On the currency front, the $A, Euro and Yen all fell slightly against the $US.

- Policy stimulus from China but only incremental. China’s State Council has backed up assurances by Premier Li that the Government will support growth by announcing various measures – including spending on railways in central and western regions, finance for more low income housing and tax support for small companies. So help is on the way but it’s only incremental and a lot of the projects were already in the pipeline and are just being accelerated. Don’t expect anything like the 2008-09 stimulus or a big growth rebound – rather the authorities are just aiming to ensure growth comes in north of 7% this year.

- QE getting closer from the ECB. As expected the ECB left monetary policy unchanged, but President Draghi’s comments were more dovish than normal and left little doubt that active consideration is being given to deploying quantitative easing, unless the outlook for inflation quickly improves. This is positive for Eurozone shares, but the combination of an easing ECB at a time when the Fed is tapering is a negative for the euro.

- In Australia, there were no surprises from the RBA which left rates on hold and presented a fairly neutral view on interest rates. It’s still a balancing act between an improving outlook for home building and consumer demand on the one hand and the slump in mining investment and the still high $A on the other. As Governor Stevens said it’s “far too soon to think about counting chickens yet”. For now this means rates will remain on hold. But as the signs of recovery build we remain of the view that the RBA will commence a gradual rate hiking cycle around September/October. The continuing surge in house prices – while not a problem for financial stability yet – is likely to see the RBA gradually step up its warnings to households not to get too optimistic in their house price expectations and not to take on too much debt and to banks not to ease their lending standards.

Major global economic events and implications

- US economic data provided further evidence the US is shaking off its winter chill with the ISM business conditions indexes improving in March, the final readings for the Markit PMIs remaining solid at just above 55 and better than expected gains in construction and factory orders. Labour market reports were mixed though and the trade deficit was wider than expected in February. Meanwhile, in a dovish speech Fed Chair Janet Yellen seemingly backed away from her “six months” comment about the gap between the end of quantitative easing and rate hikes, rather pointing out that due to economic slack the extraordinary support from the Fed will be needed for some time. My view remains that Fed rate hikes won’t commence till around mid-next year, but they are likely to become an increasing focus for investors over the remainder of this year.

- In the Eurozone growth is not yet strong enough to push unemployment down by much, but at least the unemployment rate has peaked at 12%, and has been unchanged at 11.9% since October. The next move will be down. Meanwhile an unexpected gain in retail sales adds to confidence that the recovery is broadening.

- Japanese data was a mixed bag and will likely be rather messy over the next month or two reflecting the April 1 sales tax hike. Japanese industrial production fell in February as did its manufacturing conditions PMI but the services PMI rose strongly. Our assessment remains that while the tax hike will create an air pocket a return to recession as followed the 1997 sales tax hike is unlikely because Japan now has quantitative easing (with the BoJ looking at doing more) & fiscal stimulus, unemployment is falling, property prices are rising, bank lending is rising, banks no longer have large non-performing loans and business confidence has been rising.

Australian economic events and implications

- Australian economic data was broadly consistent with a rebalancing in the economy. The AIG’s business conditions PMIs disappointed with falls in March, although they all remain well up on last year’s lows. Against this retail sales rose for the tenth month in a row, building approvals fell in February but this looks like normal volatility and they remain around past cyclical highs pointing to a boom in dwelling construction ahead, this is also supported by another solid gain in new home sales, credit growth is gradually strengthening albeit from a low base and the trade surplus remained strong in February helped by strong exports and constrained imports. The overall impression remains that the economy is rebalancing towards a greater reliance on housing, consumer spending and trade volumes which should help make up for the continuing slide in mining investment.

- It’s too early to consider rate hikes just yet, but with capital city house prices surging 3.5% in the March quarter according to RP Data and the TD Inflation Gauge remaining in the top of half of the target range for inflation rate hikes for later this year are gradually coming into focus.

What to watch over the next week?

- In the US, the Fed’s minutes (Wednesday) will be looked at for further clues as to how long after the end of tapering the Fed will start to raise interest rates, but they will be a bit dated given more recent relatively dovish comments by Fed Chair Janet Yellen. April consumer sentiment data is expected to show a modest improvement and while producer price inflation is expected to bounce back a bit after recent softness it is expected to remain benign (both due Friday).

- In China, expect March trade data (Thursday) to show a bounce back in exports after their collapse in February, but softer growth in imports. The consumer price index (Friday) is likely to have fallen in the month of March, but base effects are expected to see the annual inflation rate rise to 2.4%. A further contraction in producer prices will provide a reminder that underlying price pressures are benign.

- In Australia, expect to see business confidence and conditions in the NAB survey (Tuesday) remain consistent with a gradual trend improvement, a small bounce in consumer confidence (Wednesday) after several soft months, a continued rise in housing finance (Wednesday) and a softer employment report for March (Thursday) after February’s surprise 47,000 surge with the unemployment rate likely to be unchanged at 6%.

Outlook for markets

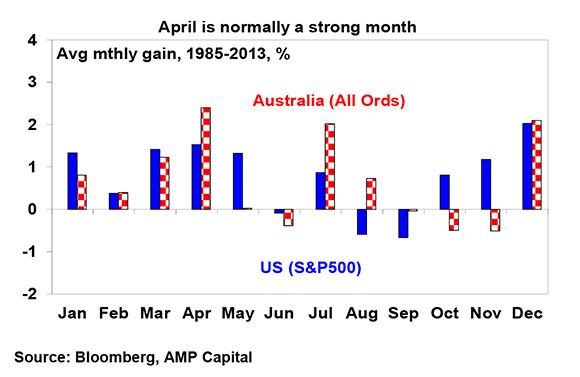

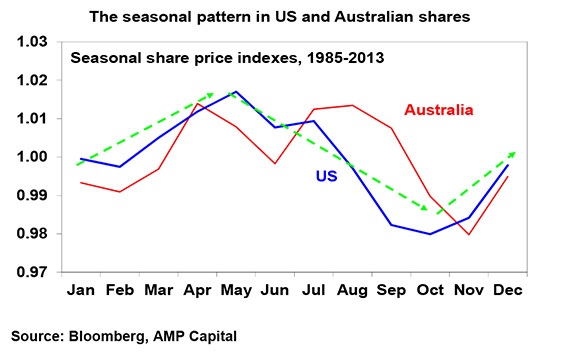

- Past experience based on the seasonal pattern in shares tells us that while April is a strong month in Australian and US shares we often see a correction around mid-year that can start about May and continue into the September quarter. See the charts below. In fact both 2012 and 2013 saw mid-year corrections of around 10% in Australian shares and 12% and 8% respectively in global shares despite both years being solid for shares overall. Something similar is likely this year and is behind our view that investors should allow for a 10 to 15% correction at some point along the way this year. A trigger could be worries about when the Fed will start to raise in interest rates as US growth recovers from its winter soft patch.

- However, just as we saw in the last two years this would just be a correction in a rising trend as share market fundamentals remain favourable with reasonable valuations, improving earnings on the back of rising economic growth and easy monetary conditions helping entice investors to switch out of cash and into shares. So any such dip should be seen as a buying opportunity. Our year-end target for the ASX 200 remains 5800.

- Bond yields are likely resuming their gradual rising trend and this combined with low yields is likely to mean pretty soft returns from government bonds. Cash and bank deposits also continue to offer poor returns.

- The short covering rally in the $A is likely to take it up to around $US0.95. However, the broad trend in the $A is likely to remain down reflecting softer commodity prices, a reversion to levels that offset Australia’s high cost base and a stronger recovery in economic growth in the US relative to that in Australia.

By Dr Shane Oliver, Head of Investment Strategy & Chief Economist

———-