Weekly market & economic update – week ending 22 August, 2014

25

Aug

2014

From Shane Oliver - AMP chief economist

Investment markets and key developments over the past week

- Share markets continued to move up over the past week helped by a combination of good economic data in the US, expectations that central banks will remain supportive and as geopolitics took a back seat. Good earnings results also helped boost the Australian share market to a post GFC high. Reflecting better US data and an abatement of safe haven demand bond yields mostly rose. Commodity prices were mixed though with oil and gold down but metals up. A stronger $US saw the Yen and euro down but the $A little changed.

- The message from the last week hasn’t really changed much. The US looks good but continuing low inflation is giving the Fed plenty of breathing space, Japan seems to be gradually emerging from the tax induced June quarter slump but Europe remains soft and Chinese data came in a bit softer than expected. Reflecting this, August business conditions PMIs rose nicely in the US and Japan, but slipped in China and Europe. The overall global recovery remains on track, but its gradual and it is not an environment where central banks will be in a hurry to take away the punch bowl.

- Rates on hold for a while yet, is also the key message in Australia. Governor Steven’s Parliamentary Testimony providing a good insight to the RBA’s thinking. In essence, Governor Stevens thinks the RBA has done enough on rates and we are seeing a pick-up in financial risk taking, but we now need to see a pick-up in “animal spirits” to drive more real economy risk taking via increasing non-mining investment. So it’s now a matter of keeping rates stable and low until this flows through. So the RBA has no real inclination to raise or cut rates. Given likely sub-trend growth in the near term and benign inflation and the still strong $A, the cash rate could be stuck at 2.5% out to mid next year at least.

- The Ebola threat is worth keeping any eye on as its continuing to rage in West Africa and the chance of travellers returning with it from Africa to a western country sooner or later can’t be ignored. In terms of assessing the market impact, signposts to watch are: the number of new cases (for signs of a peak or otherwise), its rate of spread into Nigeria, cases showing up in Western countries and transmission within Western countries. Just bear in mind though that it’s about as transmissible as HIV so if it does find its way into western countries modern medical facilities and higher hygiene standards should mean it is contained. So for investors I think it remains a case of being alert, but not alarmed.

Major global economic events and implications

- US economic data remains pretty positive with strong gains in home builder conditions, housing starts, existing home sales and the Markit and Philadelphia Fed business conditions indexes but softer than expected inflation in July of just 1.9% year on year at a core level. The rise in housing indicators confirms that the housing recovery is getting back on track but at the same time benign inflation gives the Fed plenty of breathing space. So while the Minutes from the Fed’s last meeting saw a more hawkish tone and acknowledgement of progress on the labour market, the majority on the Fed are still cautious having seen a few false starts before and in no rush to tighten.

- It was a similar story on inflation in the UK with the July CPI actually falling and adding to signs that the Bank of England’s first rate hike is still some time away.

- Japanese economic data is showing signs the economy is shaking off the tax hike hit with the Markit manufacturing PMI up more than expected in August and gains in leading indexes and machine tool orders.

- Eurozone business conditions PMIs disappointingly, but not unsurprisingly, fell in August. While they remain at levels consistent with quarterly growth of around 0.3% they highlight that the recovery remains fragile and that the ECB has more work to do.

- Chinese economic data economic data is a mixed bag with profit growth up in July and the MNI business confidence indicator rising to its highest in nearly three years, but the flash August HSBC PMI falling back more than expected and the decline in house prices picking up in July with 64 of 70 cities seeing price declines and average prices falling by around 1%. The HSBC PMI is just stuck in the same range around 50 it has been in for the last three years now which remains consistent with growth around 7.5%, but the risks from the housing slowdown mean more mini-stimulus measures may still be required.

Australian economic events and implications

- There were only second order data releases in Australia, but the ANZ/Roy Morgan weekly consumer confidence survey and skilled job vacancies both rose nicely highlighting that there is a bit of light at the end of the tunnel for the Australian economy.

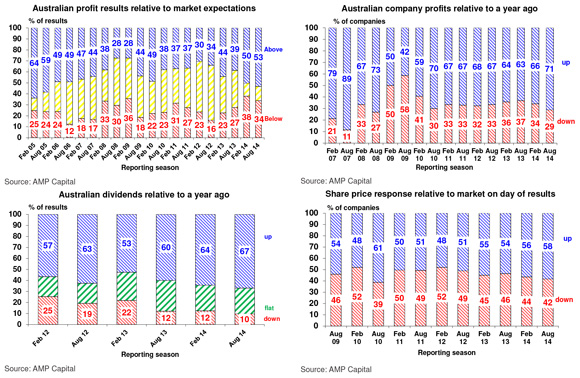

- The profit reporting season is now 75% done and is looking good. Sure it’s not been easy for non-financial industrial companies and there is still another week of results left with poorer performers often reporting late in the season. But the bottom line is that the June half earnings results are nowhere near as bad as many feared. In fact, the profit results overall are looking pretty good. 53% of companies have exceeded expectations (compared to a norm of 43%), which is the best result in nine years; 71% of companies have seen their profits rise from a year ago (compared to a norm of 66%); 67% of companies have increased their dividends from a year ago (up from around 60% in the last two years); and 58% of companies have seen their share price outperform the market on the day they released results, which is the best result in four years. Key themes have been continued strength for resources (notably Rio, although BHP disappointed), banks doing well (with a good result from CBA), ongoing cost control making up for still soft revenue growth and strong growth in dividends reflecting investor demand for income and corporate confidence in earnings prospects. Australian earnings for 2013-14 look to be on coming in a bit stronger than consensus expectations for growth of around 12 to 13%. This is being led by resources with a 28% gain, followed by banks up 10% and the rest of the market up around 4.5%. Consensus expectations for 5% earnings growth in the current financial year look a bit low to me.

What to watch over the next week?

- In the US, expect a solid bounce in new home sales after a weak June and continued strength in the Markit services PMI for August (both Monday), a continued trend rise in durable goods orders, modest gains in home prices, a slight fall in consumer confidence (all Tuesday), a rise in pending home sales (Thursday) and a continued benign reading for the core private consumption deflator (Friday) which is the Fed’s preferred inflation measure.

- In the Eurozone, expect a slight fall in confidence readings (Thursday) and continuing low inflation in August (Friday). Lending data (Thursday) will be watched for signs that recent improved momentum is continuing.

- Japanese data for household spending, industrial production and the labour market to be released Friday will be watched for further signs of recovery following the tax induced growth contraction in the June quarter. Inflation data will also be released Friday.

- In Australia, expect June quarter construction data (Wednesday) to be soft but supported by the ongoing housing construction recovery but June quarter capital spending (Thursday) to remain soft as mining investment continues to slow. The focus in the capex survey though will be on investment intentions which are expected to show further signs of an improving outlook for non-mining related investment. Expect new home sales (Thursday) to remain solid and private credit (Friday) to show a further modest improvement in momentum.

- It will also be the final week of the Australian June half profit reporting season with 50 major companies due to report, including Worley Parsons, Qantas and Woolworths. The final week often sees a few rough results as laggards sometimes come last.

Outlook for markets

- While we remain in the time of the year renowned for share market corrections, so another bout of volatility in the next month or so is possible, the broad trend in shares is likely to remain up.Valuations remain okay particularly once low interest rates and bond yields are allowed for, global earnings are continuing to improve on the back of gradually improving economic growth, monetary conditions are set to remain easy for some time and there is no sign of the euphoria that comes with major share market tops. Our year-end target for the S&P/ASX 200 remains 5800.

- Low bond yields, eg 10 year yields of just 0.5% in Japan and 3.5% in Australia, will likely mean soft returns from government bonds.

- The combination of soft commodity prices, the likelihood the Fed will start raising interest rates ahead of the RBA and relatively high costs in Australia are expected to see the broad trend in the $A remain down. Expect to see $US0.80 in the next few years, but as always with currencies getting the timing right is hard.

By Dr Shane Oliver, Head of Investment Strategy & Chief Economist

———–