Weekly market & economic update – week ending 14 November, 2014

17

Nov

2014

From Shane Oliver - AMP chief economist

Investment markets and key developments over the past week

- Shares were mixed over the last week with Japanese shares up on prospects for a delay in the next sales tax hike, Chinese shares gaining as the start of the Shanghai-Hong Kong share market link was confirmed, US and European shares little changed not helped by renewed worries regarding Ukraine and Australian shares down led by the banks. Bond yields were little changed – up a bit in the US but flat to slightly down elsewhere. With the $US consolidating after its surge since June, the $A managed to rise slightly.

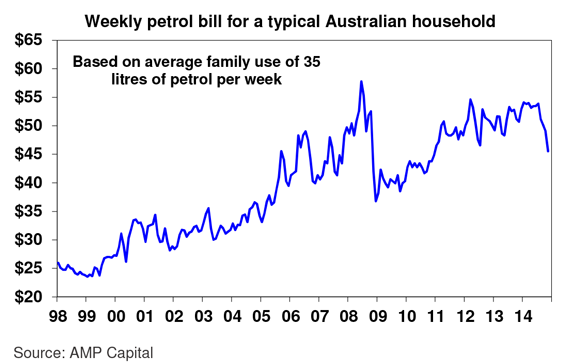

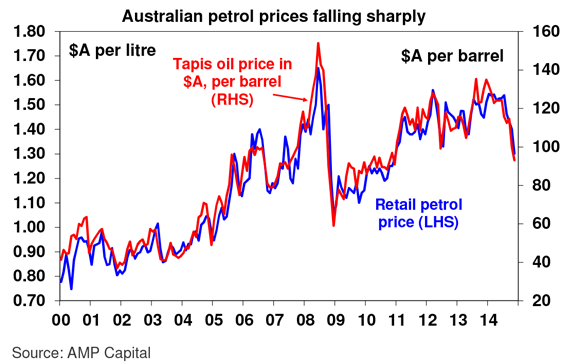

- The most significant move over the last week has been the continuing fall in oil prices. They are down 30% since June and if sustained will add about 0.6% to US economic growth over the year ahead, offsetting the negative impact from the rising $US. The fall in oil prices is likely to push average Australian petrol prices below $A1.30/litre which would represent a saving to the average family petrol bill since June of $8 a week.

- The Catalonian independence referendum has passed without much impact. Sure 80% of those who participated voted in favour of independence from Spain, but it lacked the official status of the Scottish poll and only saw around 40% of the Catalonian electorate participate. As a result it’s hardly definitive and the issue looks more like something to watch over the next decade, which is why Spanish shares and bonds ignored it.

- The focus of the G20 leaders’ summit on boosting global GDP by 2% is welcome, but bear in mind this is largely going to be driven by economic reforms which come with a lot of uncertainty as to whether they will happen and when the benefits will appear. The main drivers of the plan for Australia are already announced policies – less regulation, privatising infrastructure and reinvesting the proceeds, reducing tax and government spending, etc – which are all positive but face various uncertainties in terms of the need to get Senate support and for various state governments to be re-elected. So I won’t be revising up my growth expectations.

- Likewise the impending Australian-China trade deal – its great news but we have signed several trade deals over the last few years with talk of billions being added to the economy and yet it’s hard to discern any real impact on economic growth. That said, they are still welcome and were it not for such deals growth might be lower.

- The Shanghai-Hong Kong share market link to start November 17 is a further opening up of the Chinese financial system. This should help improved the efficiency of the Chinese share market making it less speculative and boost sentiment in Chinese shares which remain undervalued globally.

- A thought on Australian banks. While APRA Chairman Wayne Byres’ recent speech regarding the stress tests of Australian banks highlights that more can be done to improve the resilience of the Australian financial system, the fact that all 13 Australian banks passed very severe stress tests involving 13% unemployment and a nearly 40% fall in house prices actually makes me question whether they really need more capital.

Major global economic events and implications

- US economic data added nothing new with small business confidence up slightly and labour market indicators showing further improvement.

- Eurozone industrial production rose in September after a weak August but by less than expected.

- Japanese data was mixed but consistent with improving growth. Confidence fell in October, but against this machine orders have recovered to pre tax hike levels and corporate bankruptcies are continuing to fall.

- Chinese economic activity indicators slowed in October, but not dramatically so. Growth may end up coming in closer to 7% than 7.5% this quarter, but it’s still close enough to the Government’s target of “around 7.5%” for the year. Meanwhile there are tentative signs that property sales are starting to pick up and the Government appears to be putting pressure on to step up investment. More policy loosening is likely to ensure growth does not fall further, with very low inflation readings providing plenty of flexibility.

- The growth inflation trade-off in India seems to be on the mend with industrial production on the up and inflation falling. If inflation keeps falling (with lower oil prices helping) then RBI rate cuts are likely next year.

Australian economic events and implications

- Australian data continues to paint a rather mixed picture with: housing finance up strongly in September on investor loans, house prices rising solidly in the September quarter but with some loss of annual momentum and several cities only seeing moderate growth, business conditions reportedly up strongly but business and consumer confidence remaining relatively subdued and wages growth remaining at a record low. The surge in investor housing finance will have done nothing to allay the RBA’s desire to slow it down but the ongoing weakness in consumer confidence and wages highlights that rate hikes are not appropriate now or any time soon. So some sort of control of bank lending to investors remains most likely.

- The softness in wages and consumer confidence does beg the question: how come we are still seeing reasonable growth in retail sales? The answer is simple: record low interest rates, rising household wealth, newly completed homes spurring demand for household goods and lower petrol prices. So it’s not that bad.

What to watch over the next week?

- Thursday’s business conditions PMIs are expected to see more of the same with the US PMI remaining strong and those for China, Europe and Japan lagging.

- In the US, the Minutes from the Fed’s last meeting (Wednesday) will likely add little to the view that the first interest rate hike is unlikely until around mid-2015. What may be watched for though is any commentary around how the Fed is seeing the impact from softer global growth and the higher $US. On the data front expect to see a modest gain in industrial production (Monday), a rise in the NAHB home builders index (Tuesday), gains in housing starts and permits (Wednesday), a solid reading of around 56 for the Markit manufacturing conditions PMI (Thursday) and a slight fall in inflation (Thursday) to 1.6% due to lower gasoline prices.

- Eurozone PMIs (Thursday) will be watched for more signs of stabilisation as seen in October.

- Japanese September quarter GDP (Monday), is likely to show a return to growth with GDP expected to rise 0.5%. The November PMI (Thursday) will be watched for further signs Japan’s recovery is continuing.

- China’s HSBC flash PMI (Thursday) will be watched for further signs of stabilisation/improvement.

- In Australia, the Minutes from the RBA’s last meeting and a speech by Governor Steven’s Tuesday will be watched for clues on interest rates but the message is likely to remain one of interest rate stability continuing for a while yet. Data for car sales, the Westpac Leading index and Skilled Vacancies will be released.

Outlook for markets

- With the September/October correction letting off a bit of steam, shares are well placed to see gains into year-end as the cyclical bull market that started in 2011 remains alive and well. Valuations particularly against the reality of low bond yields are good, monetary policy is set to remain easy with QE in Europe and Japan replacing that in the US and rate hikes in the US and Australia being a long way off, and investor sentiment remains cautious which is positive from a contrarian perspective. Australian shares will benefit from the positive global lead and the lower Australian dollar. My year end guesstimate of 5800 for the ASX 200 remains a stretch, but it’s not out of the ball park.

- Low bond yields will likely mean soft medium term returns from government bonds. That said, in a world of too much saving, spare capacity and low inflation it’s hard to get too bearish on bonds.

- Despite a dip below $US0.86 a week or so ago, the $A still looks to be consolidating its September fall. However, with the $US trending up, commodity prices on the slide and the $A still too high given Australia’s relatively high cost base the trend remains down, with $US0.75-0.80 likely to be seen sometime in the next year or so. A relatively greater fall in the $A/$US rate is also necessary, as the $A is unlikely to fall much against the Yen and Euro.

By Dr Shane Oliver, Head of Investment Strategy & Chief Economist