Investment markets and key developments over the past week

Global share markets mostly rose over the last week as mixed US economic data was seen delaying Fed hikes, an ECB official talked about front loading QE and talk of further Chinese easing continued. Australian shares slipped though as banks remained under pressure. Bond yields rose slightly but remained below recent highs with the bond sell-off looking like its lost momentum. The $US rose slightly and this weighed a bit on commodity prices and saw the $A fall slightly.

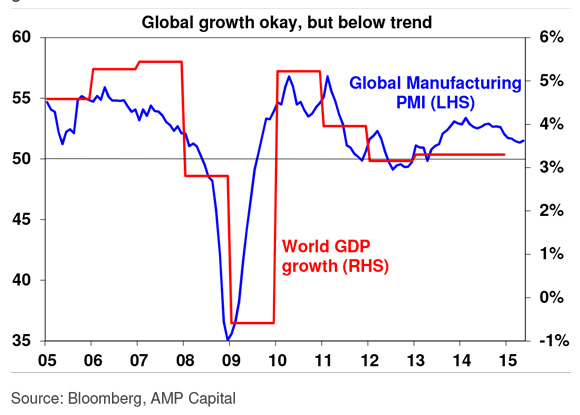

Global growth continuing but remains sub-par. The story of the last few years has been optimism regarding global growth at the start of the year and then a bit of disappointment as global growth remains uneven and below trend. This year looks the same. While “flash” manufacturing conditions PMIs rose in May (up in Japan, China and Europe but down slightly in the US), their level remains consistent with okay but still sub-trend global growth. See the next chart.

Against this backdrop, global monetary conditions are likely to remain very easy (with pressure for further easing in China) and it’s hard to get too bearish on bonds. In fact, there is a good chance that the bond sell off has run its course (at least for now).

Falling emerging world exports are worth keeping an eye on. A range of emerging and Asian countries, including Korea and Taiwan, have reported falling exports over the last few months. Part of this may reflect earlier strength in the $US, weakness in China and falling commodity prices. However, it may also be a sign of softer global growth generally. It’s too early to get too excited about, particularly as Europe and Japan have picked up a bit and the US is having just another soft start to the year, but it’s worth watching.

Still no Greek deal yet. It’s now close to crunch time for Greece which will need agreement on a funding release in the next week or so or else face a probable default event in June as it runs out of funds. Such a default or “Graccident” won’t necessarily mean that a Grexit (Greek exit from the Euro) is inevitable and by highlighting the difficult situation Greece is in could force it to agree to the necessary reforms. However, the political uncertainty – ie, whether there will be a deal? how long it will take to be approved by the Greek Parliament? whether it will have a referendum on it? what will happen if there is no deal? etc – has the potential to cause increased volatility in investment markets. Our base case remains that a deal will be reached as it’s in the interests of both sides, but whichever way it goes the rest of Europe is in far better shape now than was the case in 2010-2012 so contagion from Greece to other peripherals is likely to be kept to a minimum.

Major global economic events and implications

US data remains pretty mixed. While housing starts and permits rose strongly April and jobless claims remained low, a range of data was softer than expected including the NAHB home builders conditions index, existing home sales, the Markit manufacturing conditions PMI and regional manufacturing conditions indexes. The strong $US and the lower oil prices (via energy producers) has clearly weighed on the US growth. It will likely pick up in the months ahead but it’s another year where US growth is failing to meet expectations set at the start of the year. And that includes the Fed’s own forecasts. The minutes from the last Fed meeting offered little that was new with the Fed largely dismissing recent economic weakness as transitory, but seeing little support for a June rate hike with September looking more likely. The generally weak tone to US economic data since the last meeting make the minutes a bit dated though so it may be even more dovish now.

Eurozone data disappointed a bit, highlighting that any talk of an early end to the ECB’s quantitative easing program is way too premature. Although the manufacturing conditions PMI rose in May, services conditions fell and this dragged the composite PMI lower. While the overall PMI is still at a reasonable level, based on past relationships its pointing to growth remaining around 0.3/0.4% quarter on quarter for now. Consumer confidence also disappointed in May, albeit from a relatively solid level.

Japanese data provided a bit of confidence that its latest economic recovery is continuing. March quarter GDP growth was stronger than expected (albeit much of this was due to inventory accumulation), machine orders rose more than expected and the manufacturing PMI for May improved more than expected. As expected the Bank of Japan made no changes to monetary policy.

Chinese economic data was a bit more positive with the flash HSBC manufacturing conditions PMI improving in May (albeit by less than expected) and property prices coming in roughly flat for April (in contrast to falls averaging around 1% a month in mid last year) adding to signs that the property market may be stabilising. People’s Bank of China monetary easing has also resulted in a collapse in money market interest rates, with the overnight rate falling to around 1%.

Australian economic events and implications

A 6% bounce in consumer confidence has confirmed that the Budget has gone down far more positively than last year’s Budget did (when confidence fell 7%). This is very welcome, as confidence has been lacking for some time now. However, with confidence still only just above long term average levels a further improvement is required to get confident that the growth outlook is on the mend. Meanwhile, the minutes from the RBA’s last Board meeting and comments by Deputy Governor Lowe to the effect that there is still scope to lower the cash rate if needed support the interpretation that the RBA retains a mild easing bias. Our base case remains that 2% is the low for the cash rate, but that the risks are on the downside particularly if the $A fails to behave. However, going by the recent experience another cut in rates is unlikely to occur before August as the RBA would probably prefer to get a look at its next set of economic forecasts (which won’t be available till August).

What to watch over the next week?

In the US, March quarter GDP growth (Friday) is likely to be revised down to -0.9% annualised from 0.2%. However, there is greater than normal confusion around it, as it appears that the Bureau of Economic Analysis’s seasonal adjustment process is understating March quarter GDP growth and a re-adjustment would put it around 1.8% annualised. In other data, expect a slight improvement in underlying durable goods orders, continued strength in home prices, a rebound in new home sales (all due Tuesday), a further gain in pending home sales (Thursday) and a rise in consumer sentiment (Friday) should all help allay fears that the US economy has slowed too much.

Eurozone confidence data for May (Thursday) will be watched for evidence that the pick-up in Eurozone growth is being sustained. And of course, progress towards a “reform for funding deal” with Greece will be watched very closely given Greece is now close to crunch time.

In Japan, expect to see labour market indicators remain solid, a slight improvement in household spending and a bounce in industrial production, but inflation to fall back to only just above zero as the sales tax hike a year ago falls out of the annual inflation figures (all Friday).

In Australia, expect to see a 1% fall in both March quarter construction activity (Wednesday) and business capital expenditure (Thursday) driven by the ongoing slide in mining investment. The key to watch will be business investment plans for any signs of an improvement in the outlook for non-mining investment. Data for new home sales and private credit will also be released Friday. Clues on the interest rate outlook will be watched for with RBA officials Lowe and Edey both speaking.

Outlook for markets

Given the uncertainties around the bond sell off, the Fed and Greece the next few months could remain volatile for shares. However, notwithstanding near term risks, the conditions for an end to the cyclical bull market in shares are still not in place: valuations against bonds remain good; economic growth is continuing at a not too cold but not too hot pace; and monetary conditions are set to remain easy. As such, share markets are likely to see another year of reasonable returns. My year-end target for Australian shares remains 6000. It’s just that the market got ahead of itself with the surge earlier this year and it’s been working it off ever since.

Still low bond yields point to soft medium term returns from bonds, but it’s hard to get too bearish on bonds in a world of too much saving, spare capacity and deflation risk. Central banks won’t be ratifying a bond crash like in 1994.

Despite the risk of a further short term bounce in the $A – possibly up to the 200 day moving average around $US0.83 – the broad trend is likely to remain down as the Fed is still likely to raise rates later this year whereas the RBA retains a mild easing bias (which is likely to turn into an easing if the $A doesn’t soon head back down) and the long term trend in commodity prices remains down. We expect a fall to $US0.70 by year end, and a probable overshoot into the $US0.60s in the years ahead.

Shane Oliver, AMP Capital

——