Ever since China’s 2009 stimulus program, commentators have expressed concern over the swelling of Chinese local government debt burdens – a feeling that only intensified as GDP growth slowed, exposing increasingly limited revenue sources.

Local governments, in a rush to tap policy stimulus, used local government financing vehicles (LGFVs) to raise bank loans to invest in infrastructure development, thus promoting urbanization and growth. This led to excess investment and as the Chinese government clamped down on its booming property market, it cut a prime funding source for local governments, exposing creditors to default risk.

On 8 March 2015, China’s Ministry of Finance (MoF) issued a 1 trillion RMB quota for local governments to convert LGFV debts into lower-yielding municipal notes. By migrating to more formal financing channels, the debt swaps should give rise to more market discipline and more effective risk pricing, as well as improving financial markets’ perception of risk within the banking system.

In our view, the introduction of the debt swap program is significant, representing one of the first steps in addressing more fundamental issues within China’s fiscal framework. In this paper, we examine how LGFV debt grew to its current levels, the effect that the debt swap program will have on local governments and banks, how this is already affecting Chinese stocks and what further structural reforms we should expect.

2009 policy stimulus led to sharp increase in LGFV debt

LGFVs are not a recent phenomenon in China – they have been in existence since the 1980s when the first was set up in Shanghai to facilitate local infrastructure development. Many more were set up following the Asian Financial Crisis as China limited local government bond issuance and bank lending, and then again in 2009 in reaction to the government’s stimulus package.

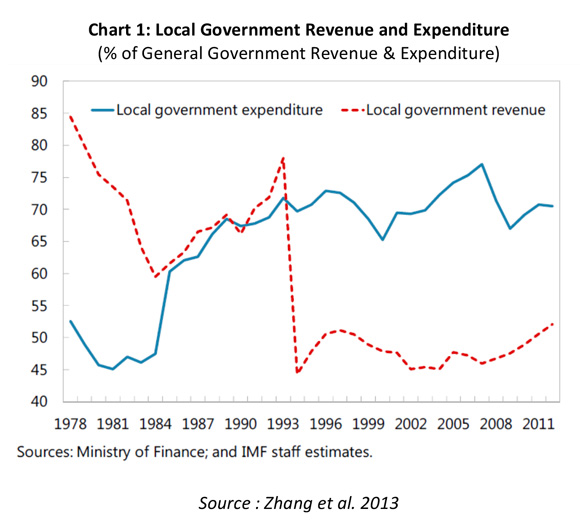

Following the central government’s rapid centralization of revenue sources in 1994, the only major remaining source for local governments was land sales, supplemented with some revenues from utilities, tolls and infrastructure projects. Indeed, they have little discretion over tax rates and policy, while central government transfers are mainly to cover current spending, leaving little for infrastructure investment without off-balance sheet financing. The central government intended that this would instil greater discipline on local government spending.

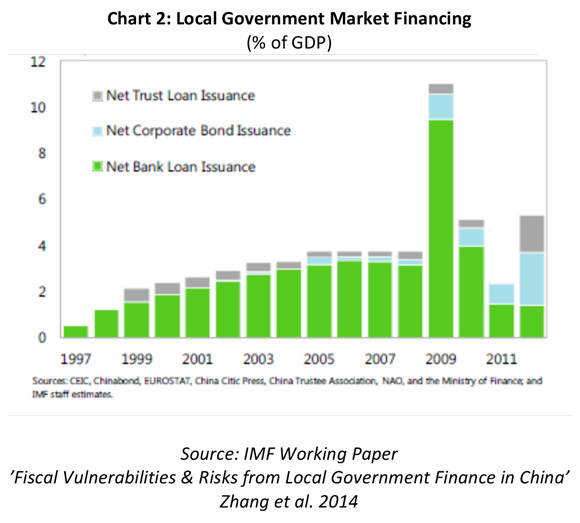

In 2009, as a policy response to the global financial crisis, China launched an unprecedented stimulus program to boost growth through infrastructure investment and urbanisation. But you will not find evidence of this in headline fiscal statistics because the majority was conducted through an expansion in bank credit. With limited capacity for local governments to borrow on-balance sheet and forbidden from taking on bank loans directly, LGFVs were used to access this stimulus program. The perception of an implicit central government guarantee made LGFVs attractive credits for banks and led to a surge in bank loans in 2009. As the economy recovered, these stimulus measures were unwound. With slowing growth, they were resumed in 2012, except that banks were now more reluctant to lend directly to LGFVs and this gave rise to Trust loans (see Chart 2) and more direct bond issuance by LGFVs.

These waves of liquidity undoubtedly led to some reckless lending and ambitious projects as local governments competed for growth. Estimates of the total amount of local government debt outstanding vary, but the last official estimate by China’s National Audit Office (NAO) put the figure at around RMB 17.9 trillion by mid-2013. Based on the MoF’s disclosures, independent research house BCA estimates this figure will have risen to around 20 trillion by end 2014[1], with Goldman Sachs estimating it slightly higher at 21 trillion[2].

In September 2014, the State Council issued Article No. 43 to resolve local government financing issues. One key recommendation of this article was that from 2016 onwards all government-funded projects would need to be financed by municipal bonds issued by provincial governments and would be included in fiscal budgetary planning. It also stipulates that for public projects with commercial viability, governments should finance via project-based bonds or PPPs and LGFVs should be shut down, consolidated or transformed from 2016.

On 8 March, China’s MoF issued a 1 trillion RMB quota for local governments to convert some LGFV debts into lower-yielding municipal notes, together with 600 billion of new approved municipal bond issuance (up from 400 billion in 2014). This swap arrangement represents around 56% of LGFV debt expected to mature in 2015, according to NAO’s survey.

Debt swap program could save local governments up to 5% in interest payments

This development has many implications, chief among them being lower borrowing costs for local governments, greater transparency in China’s debt markets and ultimately a lower equity risk premium for Chinese stocks, particularly banks. For debt markets, we are likely to see a swathe of new issuance in the municipal and corporate space, with the crowding out impact likely moving from loan markets to debt markets.

The MoF estimates that the 1 trillion debt swap program would save local governments 40-50 billion RMB in borrowing costs this year, an effective decrease of 4-5% in borrowing rates. Extrapolating this to the entire RMB 20-22 trillion outstanding would result in savings of around 1 trillion or 1.5% of current GDP, although this is a best case scenario.

It is important to note that this exercise does not lower leverage within the system; it is merely a transfer of off-balance sheet debt into more formal fiscal liabilities. By migrating to more formal financing channels, it should also give rise to more market discipline and more effective risk pricing compared with the previous system. Municipal debt should be formally included on broader government debt-to-GDP ratios giving market participants greater transparency on China’s true debt profile. The focus will likely shift away from LGFVs to other problem areas like overleveraged and inefficient state-owned enterprises (SOEs), which still make up the majority of corporate debt in China (see Chart 3).

Bank stocks should benefit from lower equity risk premium

Greater clarity on local government debts and reduced borrowing rates should improve financial markets’ perception of risk within the banking system. LGFV defaults were one of the main segments stress-tested by analysts when trying to gauge potential non-performing loan formation in the banking sector. Lower systemic risk should help reduce the equity risk premium of Chinese stocks and, in particular, bank stocks. For this to happen, the market needs to assume that the debt swap facility will be implemented on an annual basis covering those debts due that particular year, something that is difficult to do without further disclosures on the outstanding debt and the quality of underlying assets.

Shares in China Construction Bank, one of China’s largest banks by assets, de-rated considerably as asset quality concerns intensified following the 2009 stimulus, despite its return on equity remaining largely unchanged over the period (see Chart 4). We note here that its A-share listing has started to re-rate reflecting renewed optimism amongst mainland investors that the worst may be behind us.

The direct impact on banks is to free up capital and loan quotas whilst eroding net interest margins. LGFV loans account for approximately 5% of total loans and have a 100% risk weighting vs. municipal debts at 20%. Hence, this swap will lead to a reduction in risk-weighted assets (RWA) and an uplift in capital. Similarly, when LGFV loans are reclassified into municipal debt, they drop out of the loan-to-deposit ratio calculation, freeing up more capital to redistribute lending into under-served areas (private corporates and retail) of the financial system. It may also result in some release of provisions otherwise set aside for bad debts in this segment. This whole exercise should help to reduce the crowding out impact that local governments have had on private sector borrowers in bank loan channels.

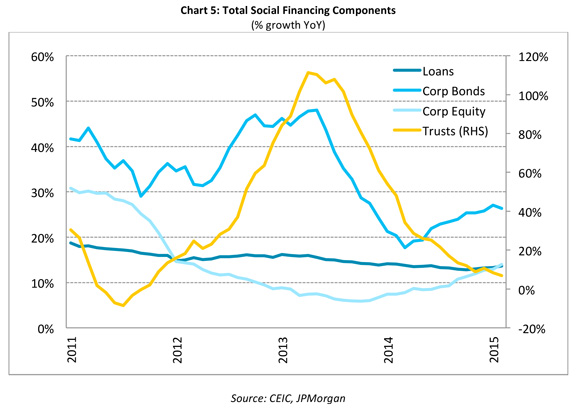

We do not expect that this move will lead to a dramatic uptick in new credit formation and would be concerned if this were to occur. This is less about the quantum of credit and more about the move toward more efficient allocation within the credit system. The migration from off-balance sheet to more formal channels is also well underway in other segments of China’s credit system. ‘Shadow banking’ finance channels have slowed significantly since mid-2013, while growth in corporate debt issuance, equity raising and conventional bank loans has picked up (see chart 5).

One unanswered question is: ‘Who is the end buyer?’ The answer will determine whether this measure is akin to fiscal stimulus and/or a liquidity injection by the government or People’s Bank of China (PBoC). We will watch this closely, but our base case is that banks will be the initial buyers in a straight swap of loans for debt and will then sell them in secondary markets to insurers, institutions and retail investors (likely via wealth management products and money market products like Alibaba’s Yu E’Bao). We think the Chinese government would want to avoid placing more funds in the hands of local governments following their recent track record, but it is an option if growth started to materially disappoint. Whilst writing this article, the state council moved to allow the Social Security Fund to invest, for the first time, up to 300 billion RMB into local government debt, adding another sizable investor to the list.

Confident investors have driven Shanghai Composite up 13% since March announcement

Despite the western world’s conclusions that China was headed for a shadow banking/LGFV-induced financial crisis, it has demonstrated that it still has plenty of tools at its disposal to avoid such a scenario. A key reason why China has been able to avoid a crisis has been the central command function of the state, together with its closed financial system. In such a system, so long as confidence is maintained, it is unlikely that widespread bankruptcies or bank runs can occur without intention.

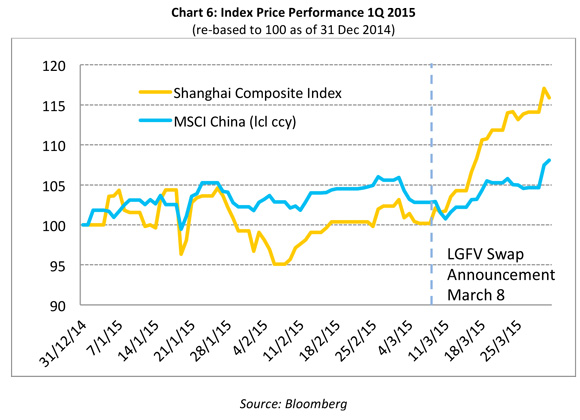

We believe LGFV debt swaps are a game changer, but must be complemented with strategic reform in terms of how local governments allocate capital, raise revenues and finance infrastructure projects. In isolation this debt swap event should help to reduce the equity risk premium priced into China’s equity markets, in particular the banking sector. We note here that mainland investors have reacted a lot more positively than overseas investors, with the Shanghai Composite Index up 13% since the announcement and MSCI China up only 4% (through 31 March; see Chart 6).

The Shanghai Composite Index now trades at a price to earnings multiple of 19.4x, while MSCI China trades at only 11.4x. While A-share markets have, to some extent, been driven by strong retail buying and margin finance, it is premised on confidence in China’s leadership and their ability to structurally correct system vulnerabilities and drive its next economic chapter. We expect international investors will gradually reach similar conclusions.

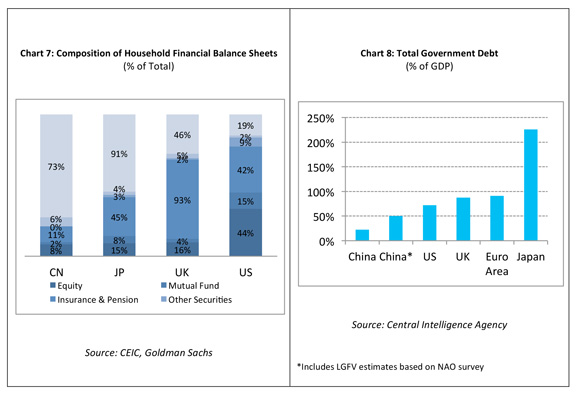

While there are over-leveraged segments in the Chinese economy, there are two significant components of the system’s balance sheet that remain largely under-utilised: the central government and the consumer (and arguably large parts of the private sector (excluding property) which have been crowded out by local governments and SOEs). While the debt swap program should alleviate some of this crowding out effect, deposit insurance (announced 31 March) and better social security systems are two prerequisites for ‘unleashing’ the Chinese consumer. These are necessary if China is to achieve its goal of transitioning its economic growth model more towards consumption from investment. We note that the Chinese consumer still holds 73% of their financial assets in cash deposits, far more than their developed market peers (see Chart 7). The central government remains under-leveraged by international standards and still has a very strong asset side of the balance sheet which provides further room to manoeuvre (see Chart 8).

Authorities likely to implement much-needed strategic reforms

The debt swap program buys time for authorities to address more fundamental issues within China’s fiscal framework. The country needs to develop a more streamlined mechanism between central and local governments for capital allocation and budgetary decisions to ensure a repeat of this debt build-up cannot occur. The most pressing issue for buyers of municipal debts is that of the chronic mismatch between local government revenue sources and expenditures.

As discussed previously, local governments have been overwhelmingly reliant on land sales as a source of revenues ever since the central government centralised revenue sources in 1994. Their reliance on land sales for financing resulted in an over-supply of real estate that, in turn, makes the property market highly susceptible to a cyclical downturn.

VAT implementation and distribution, direct property taxes (currently being piloted in Shanghai and Chongqing), SOE restructuring and asset sales are some of the key measures required to improve revenue sources on a sustainable basis. China’s public sector asset base is still huge and there is plenty of potential for restructuring inefficient SOEs and selling assets. It is difficult to get accurate and timely data on the asset side of the government’s balance sheet, but as we see from the International Monetary Fund’s (IMF’s) estimates in Chart 9, there are still significant quantities of capital in natural resources and for-profit non-financial SOEs.

As LGFV repayment issues subside, the focus shifts to restructuring and possible selling underperforming and inefficient SOEs. From a capital allocation perspective, we would also like to see policies to gradually remove implicit state guarantees, improve profitability and eventually allow weaker institutions to fail. This is a pre-requisite for more efficient and market-orientated capital allocation by banks and credit markets. We note from recent bank management briefings that they have started to discuss the possibility of SOE defaults, something that was unheard of before the era of Xi Jinping and the new leadership’s unprecedented anti-graft campaign.

Another important change would be to develop more sustainable metrics, other than pure GDP growth, to assess provincial government performance. This would lead to more productive investment decisions helping to alleviate the threat of new bad debts arising. In October 2014, the State Council announced it would establish assessment accountability mechanisms where local government debt levels would be used as one of the hard measures for evaluating performance and this is a step in the right direction. We would also note that Shanghai has decided not to set a GDP growth target at all this year, the first province to do so.

Conclusion: Debt swaps demonstrate government’s intention to implement strategic reforms

The importance of President Xi Jinping’s strong leadership cannot be stressed enough. Under him, China is undergoing dramatic changes. While the most thorough cleansing of state corruption is ongoing, elements of China’s grand strategy are becoming more evident. Domestically, we are seeing efforts to correct financial system vulnerabilities, promote market based risk-pricing and open up capital markets. On foreign policy, key examples include China’s ‘One Belt, One Road’ initiative and its setting up of the Asia Infrastructure Investment Bank (AIIB).

We remain optimistic that China is emerging from a tough period in its economic development cycle and the LGFV debt swap program is one of the first steps in addressing system vulnerabilities. However, the debt swaps must be complemented with strategic reform in terms of how local governments allocate capital, raise revenues and finance infrastructure projects. These reforms are essential if China wants to ensure a similar debt build-up will not occur in the future.

While the debt swap program does not alter the trend for slower GDP growth, it should provide greater confidence in the country’s ability to deal with other well-documented issues. Mainland investors have grasped this concept and we believe it will not be long before western investors start to reach similar conclusions.

Peter Monson, Senior Equity Analyst, Nikko Asset Management Asia

——–

[1] ‘China Investment Strategy – Weekly Report’, BCA, 18 March 2015

[2] ‘Untangling China’s credit conundrum‘, Goldman Sachs, 26 January 2015