Clients who moved into residential aged care before 1 July 2014 may think they are lucky to remain under the old rules. These rules calculate the ongoing care fees on assessable income only, instead of the new means-tested calculation which can mean lower fees.

But if these clients have defined benefit super pensions or high levels of income they can still pay high daily care fees without the protection of a lifetime cap. And if they recently sold their former home, they may have seen not only a reduction in age pension entitlements but also an increase in care fees.

Clients who moved into care before 1 July 2014 could be asked to pay an income-tested fee up to $75.42 per day which equates to $27,528 over a year (current to 19 September 2015) in addition to the basic daily care fee and the cost of their accommodation.

Strategies to reduce assessable income may help to reduce the cost of care for these clients. The strategy to invest in an investment bond through a discretionary trust may be effective as it is designed to reduce assessable income.

The cost of care (pre 1 July 2014 rules)

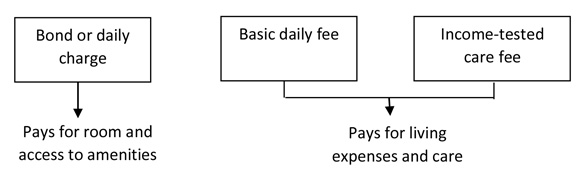

Clients who moved into residential care before 1 July 2014 paid either a lump sum (bond) or a daily charge for accommodation. In addition they contribute to their cost of care through daily fees. How much they contribute depends on their level of assessable income.

The income-tested care fee is calculated as a percentage of the client’s assessable income (using Centrelink income test assessment rules) plus payments received from Centrelink/Veterans’ Affairs (less some supplements). A portion of this total income over an allowable threshold sets the fees.

The income-tested care fee is calculated as a percentage of the client’s assessable income (using Centrelink income test assessment rules) plus payments received from Centrelink/Veterans’ Affairs (less some supplements). A portion of this total income over an allowable threshold sets the fees.

Income-tested care fee (ITF) = (Assessable income – threshold) x (5/12)

Example:

Rachel is a widow who moved into residential aged care in June 2014 and paid an accommodation bond of $200,000. She has the following income and assets:

Rachel has been receiving a small age pension of $1,786 per annum and her care fees are currently $25,933 per annum ($17,334 basic care fee plus $8,599 income-tested fee).

Rachel has been receiving a small age pension of $1,786 per annum and her care fees are currently $25,933 per annum ($17,334 basic care fee plus $8,599 income-tested fee).

Rachel’s family decide to sell her former home and invest the $870,000 sale proceeds into term deposits. She will lose the age pension and her care fees increase to $37,526 per annum due to the income-tested care fee increasing to $20,192 per year.

Reducing the income-tested care fee

When calculating the ongoing care fees, income includes amounts received from Centrelink or Veterans’ Affairs (less some supplements) as well as assessable income from assets and investments using Centrelink income test rules. For example, cash, term deposits and shares are assessed under deeming rules.

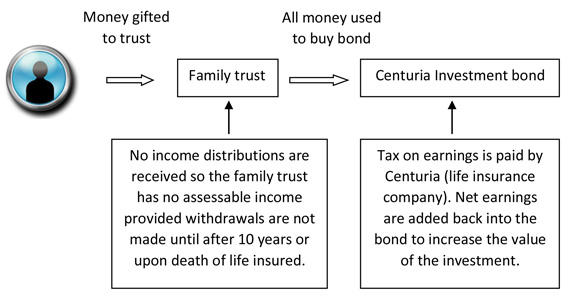

Clients may be able to reduce fees by structuring their investments using the trust/investment bond strategy to reduce assessable income.

If a client is likely to pay a high income-tested fee, the client may benefit from setting up a new discretionary family trust and gifting money into this trust. The trust then invests this money into an Investment Bond. This won’t change how much the client has in assessable assets but assessable income may reduce because fee calculations use the actual taxable income generated by the family trust. As long as the client does not make withdrawals from the bond within the first 10 years (or until death of the life insured) there is no taxable income for the trust so no assessable income is generated.

Example:

Rachel’s family seek advice on how to structure her investments to pay the additional care fees.

She is advised to set up a family trust and transfer enough of her investments into the trust to reduce the income-tested care to approximately the same level she was paying before she sold her house.

Rachel sets up a new discretionary family trust and gifts $850,000 of the sale proceeds into the trust. This money is then used to buy an insurance bond inside the trust. Rachel will still not qualify for any age pension due to the assets test assessment but her daily care fees will reduce back to $25,984 per year (with an income-tested fee of $8,650).

This strategy reduces Rachel’s care fees by $11,542 per annum but a full financial analysis is required to determine whether it is an appropriate strategy and how much she should be advised to transfer into the trust.

Developing an advice solution

Before making a recommendation it is important to review the client’s full situation to ensure sufficient cash flow can be generated and to determine the full impact on their net wealth. The savings in income-tested fees need to be considered in conjunction with cash flow, eligibility for Centrelink or concession cards, aged care fees, taxation and estate planning.

To determine whether this strategy is appropriate for a client it is firstly important to consider cashflow needs. The money invested into the trust remains accessible but to benefit from the strategy, withdrawals should not be made within the first ten years or until the client’s death. Therefore, clients need to be able to generate sufficient cashflow to pay their care fees and living expenses from their other sources.

In the first year clients will incur expenses to set up the trust and investment strategy. They may also incur ongoing fees for reviews and operation of the trust. The insurance company pays tax at 30% which may be higher than the client’s personal tax rate but it is the after-tax return which is important to compare.

Clients may also need to restructure their wills and estate planning due to this change in assets and consider whether to nominate a beneficiary on the investment bond.

Note: Calculations in this flyer are based on rates current to 30 June 2015. A single person can have assessable income up to $25,264 per annum before an income-tested care fee is payable.

————