Beijing’s swift and high-handed policy response to the Chinese stock market’s sharp correction has raised eyebrows. In our view, however, a greater issue is whether policymakers will abandon their reform agenda and go the full monty to support the market. If they do, there is a huge amount of liquidity to be tapped, as well as slush funds at various government arms that can be marshalled for fiscal stimulus.

Unprecedented Policy Response The Shanghai A-Share Index has fallen more than 30% from its mid-June peak as panic selling has snowballed. Although the correction still isn’t all that extreme, compared with the 150%-plus rally from a year ago, Beijing’s policymakers have responded swiftly with an all-out effort to support the market with unprecedentedly heavy-handed directives.

It’s obvious that the fear of social discontent has been a key driver behind this prompt action. The potential impact of a stock-market crash on the already weak domestic consumption and investment in today’s “new normal” slow-growth era must also have crossed the policymakers’ minds.

The policy response so far includes some fairly standard measures, such as the suspension of initial public offerings, provision of emergency liquidity, and share buybacks by state-owned enterprises. What is eye-catching, however, is that the authorities are also effectively coercing local financial institutions into purchasing stocks and holding them for a certain period, as well as restricting short selling.

These measures, which set a controversial precedent, appear as though they are on the orders of senior politicians who may not have given much consideration to the potential market distortion or the consequences of hindering a normal market correction.

Moreover, the money collected from various institutions, such as asset management firms and brokerages, for these market-support measures has so far only amounted to hundreds of billions of renminbi (RMB)—a fraction of the total tradable market capitalization of some RMB47 trillion and significantly shy of the estimated RMB5 trillion in leveraged financing (margin lending and other stock-purchase funding) that has fueled the equity market frenzy over the past year.

Is the Slowdown out of Control?

This uphill fight against the market may go on for a while, with all its bureaucratic inertia. It’s important to realize, though, that the question about whether China can arrest the sharp downshift in growth had emerged well before this stock-market correction. Therein lies the root cause of the problem.

In our view, China has not run out of policy options, and it’s certainly not on the verge of adopting quantitative easing (QE) as the US, Europe and Japan did. A larger, longer-term consideration here is, if China really faced a hard landing or a financial crisis, would it abandon its reform and deleveraging drive and resort to outright reflationary fiscal and monetary stimuli à la 2009?

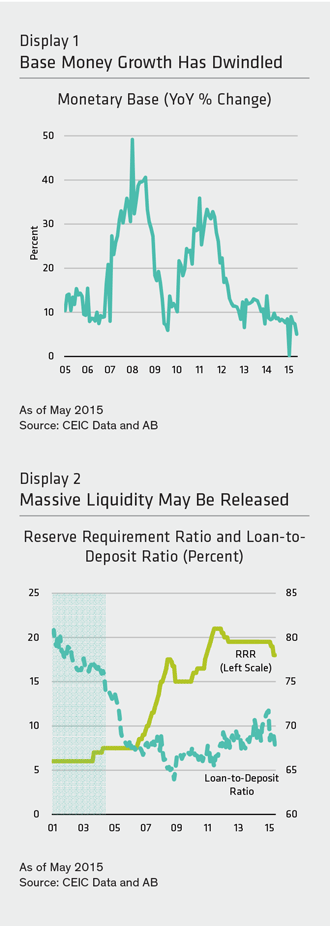

To date, the People’s Bank of China (PBOC) has stuck to a prudent course of action—a gradual, traditional monetary easing to cushion the economic down draft that has accompanied reforms. In any case, the PBOC has some way to go before going down the QE path, given that Chinese interest rates have yet to fall to zero percent and the central bank is struggling to prevent a further slowdown in base money growth. A rapid expansion in the central bank’s balance sheet, like those in the QE regimes, has not been observed (Display 1).

Potential for a Massive Liquidity Release

In a worst case scenario, where Beijing forfeits its reform agenda and commits to a total reflation policy, China has the firepower to inject a substantial amount of liquidity into the banking system, even though this may have negative side effects.

Consider this: the reserve requirement ratio (RRR) for Chinese banks was raised from a mere 6% in the early 2000s to a peak of 21% in 2011 in order to sterilize the excess foreign capital inflows and avoid a monetary overhang. But the net inflow has now turned into a net outflow, and domestic sterilization measures are no longer a structural necessity. Thus, an easing in the RRR may help release sizeable amounts of liquidity back into the system.

If the RRR is reduced from the current 18% level to, say, 5% in a short period of time, some RMB17 trillion (US$2 trillion) of fresh liquidity can be pumped into the system (Display 2).

Similarly, if the recent relaxation of banks’ loan-to-deposit ratio is pushed to the extreme, from the current 68% to, say, around 90%, about RMB29 trillion (US$4.6 trillion) of extra credit can be made available to the economy. The combined amount of these two measures wouldadd a staggering US$6.6 trillion to China’s US$10 trillion economy.

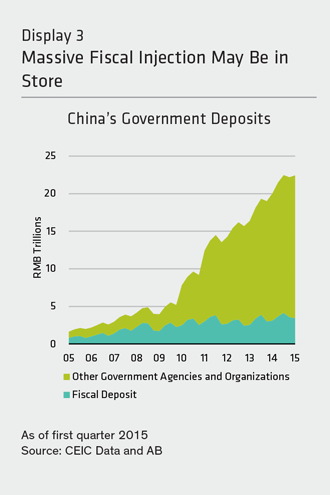

This might generate a significant lift for growth, but it would also re-leverage the economy. Furthermore, it’s not just monetary policy. Beijing can opt for a huge fiscal injection if need be. Underspending and over-budgeting at the local government level over the years have resulted in a cumulative RMB3.4 trillion (US$550 billion) worth of fiscal deposit. This money should be liquid and can be used flexibly in times of emergency to pump-prime the economy. On a wider scale, deposits belonging to the more broadly defined public sector, including government agencies and other public organizations, total some RMB19 trillion (US$3 trillion), although these would be less flexible for use as a policy tool (Display 3).

Near term, the authorities will be in a war of liquidity to stabilize the stock market. From its peak in mid-June, margin financing has shrunk by some 36%, and this was the trigger of the equity downturn. The current rounds of de facto market intervention will only cap or slow this unwinding process, which is crucial to a market’s correction phase.

Without a further unwinding of margin trades, however, the only way for the market adjustment to be complete would be for confidence to be somehow rebuilt, perhaps on relative value grounds or by government policy. The latter may mean continuous waves of liquidity injections to support the government-orchestrated stock purchase program.

By Anthony Chan, Asian Sovereign Strategist, Global Economic Research, AB