The Congressional Budget Office estimates that the budget deficit for fiscal year 2015 will narrow further, extending to six consecutive years a trend of shrinking deficits. But the longer term looks bleak. In fact, continued economic growth over the next decade won’t likely generate enough revenue to cover rising costs of entitlements and interest payments on US debt. Legislative changes are needed to combat the rising tide of deficits.

US Budget Position: Good in the Near Term…

For fiscal year 2015, the Congressional Budget Office (CBO) estimates that the US budget deficit will be $468 billion, down $25 billion from the 2014 deficit. This modest improvement is primarily driven by continued relatively strong gains in revenues (+5.9%) and somewhat slower growth in outlays (+4.9%).

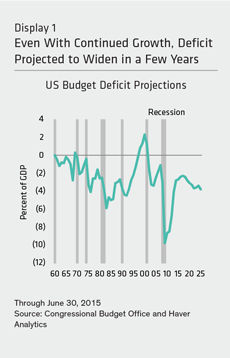

This marks the sixth consecutive year in which the deficit has declined relative to gross domestic product (GDP). And at 2.6% of GDP, the scale of the current deficit is back to levels last seen in 2005, and it stands very close to the 50-year average of 2.7%.

…but Longer-Term Picture Is Bleak

But the long-term budget projections from the CBO aren’t as rosy. In June, it updated its 10-year budget baseline projections. They show the US budget deficit remaining at current levels over the next few fiscal years, but then show them starting a steady climb—hitting 3% near the start of the next decade and 4% in 2025 (Display 1).

To be fair, the longer-run budget projections, which are prepared by the CBO on an annual basis, are not done for the sole purpose of predicting actual budget outcomes. Actually, their main purpose is to provide a perspective on the future trends of revenues and outlays (and resulting deficits), as it frames the current set of tax and spending laws against a backdrop of consensus economic growth and interest-rate projections.

Continued Growth Does Not Generate Budget Balance

Understandably, the economic and interest-rate projections are critical to any long-run budget projection. Yet as a rule, the CBO employs conservative assumptions in framing the outlook. In fact, the current 10-year budget projections are based on a continued economic growth of 2.2% per year, a consumer price inflation of 2%, and a normalization of near- and longer-term interest rates to 3.5% and 4.5%, respectively, starting in 2018.

One of the key takeaways from the CBO’s 10-year budget projections is that a prolonged economic growth cycle is not likely to generate a sufficient enough increase in revenue to cover the rise in outlays associated with an aging population, increased federal health costs and rising interest payments on the outstanding federal debt. Ordinarily, budget deficits are highly cyclical in that they rise during recessions and narrow during economic growth cycles. But CBO estimates show that even if the economy continues to expand at its potential pace of 2.2%, the budget deficit will start to widen within five years from today and then steadily increase into the next decade.

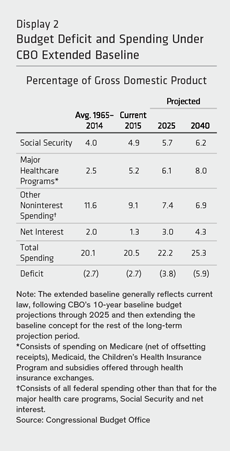

The spending side of the budget is mainly responsible for the rising tide of higher deficits. Indeed, by 2025 the CBO estimates that federal spending will equal 22.2% of GDP, which is more than 200 basis points above the 50-year average. And all of the higher spending is concentrated on mandatory programs (entitlements and healthcare) and interest payments.

Time for a Long-Term Reality Check

In Washington right now, there’s almost no attention being placed on the US budget outlook beyond the next year or two. After all, projections over the next few years paint a picture of budget tranquility, with deficits that are broadly in line with historical averages.

But the US faces a rising tide of unaffordable outlays that will ultimately force us to take on a mountain of additional debt in order to pay for all of the promises that have been made in the past. The country would be well served if our leaders started crafting a list of options to deal with the prospect of rising deficits. By postponing necessary changes in spending and tax law, the scale of the required fiscal actions will become progressively larger. Indeed, CBO budget projections beyond the next decade are even more ominous (Display 2).

The current environment is ripe with examples of countries, states and municipalities that have postponed making hard fiscal decisions. In the end, the scale of the adjustment had to be much larger than what would have otherwise occurred if the decision makers started sooner. Currently, the US still has a window of opportunity to phase in incremental changes that would likely be less disruptive and less costly over the long term. The question remains whether the US will harness the political will to make effective changes in time.

By Joseph G. Carson, US Economist and Director, Global Economic Research, AB

———–