Malaysia: capital controls to support ringgit would be disruptive

China’s surprise currency devaluation, which triggered a sell-off in many Asian currencies, has increased Malaysia’s headache as the country had already been struggling to halt the ringgit’s decline. Reintroducing capital controls to support the currency—as some in the market expect—would be counterproductive, but we believe that investors should be vigilant about such a tail risk.

Victim of Renminbi Devaluation

The Malaysian ringgit (MYR) has been a major victim of the Chinese renminbi’s surprise devaluation, which has triggered a broad sell-off in Asian currencies. The renminbi shock came at a particularly inopportune time for Malaysia, as Bank Negara Malaysia (BNM) had been trying to defend the MYR, draining 8% of its foreign reserves in July alone to US$96.7 billion.

The sharp fall in the MYR and the aggressive intervention by BNM has led to concerns in the market that draconian capital controls and a currency repegging, similar to the measures introduced in 1998, might be back on the table. In our view, such attempts to wrestle with the market will only induce more turbulence in Malaysian financial markets, given the hefty positions of foreign investors.

The differences between today’s economic fundamentals and those of 1998 suggest that such capital controls would be costly and yield no benefit from an economic standpoint. Be that as it may, we believe that investors should remain vigilant about the risk of such a policy misstep, as the deteriorating political situation could result in various nationalist or populist moves.

Different Policy Considerations

So what are the differences in today’s economic environment from that of 1998?

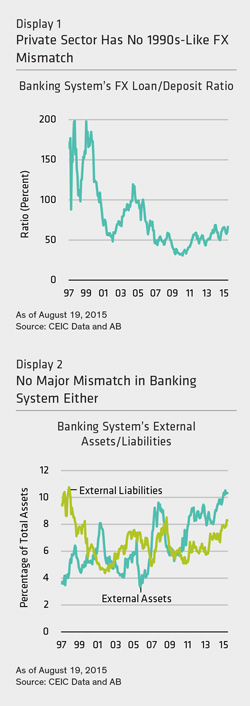

First, foreign exchange asset/liability mismatches in the late 1990s were severer, both in the private sector and in the banking system. The foreign exchange loan-to-deposit ratio was as high as 200% back then (Display 1)—in other words, private sector companies’ foreign currency borrowings from banks were double their foreign currency deposits. The net foreign exchange liabilities of banks themselves also stood at nearly 7% of the banking system’s balance sheet (Display 2). Any sharp MYR depreciation could have resulted in a significant balance-sheet crunch. Now, however, both private sector businesses and banks have positive net foreign asset positions, which means that there is not as much need to stabilize the MYR at all costs.

Second, foreign reserves had dwindled to more alarming levels before the 1998 capital controls. The reserves covered only three months of imports, and short-term external debt rose to 60% of the reserve levels. Now, the need to protect reserves is less urgent. Even though BNM has been draining reserves, the reserve level still stands at six months of imports, which is a more comfortable level than those of many other emerging-market countries outside Asia.

Third, even if BNM were to impose capital controls, such measures would not be very effective in rebuilding foreign reserves at present owing to underlying external payment dynamics. Back in the late 1990s, external demand was healthier and net foreign direct investment (FDI) inflows were more sizable. Moreover, an import compression pushed the current account balance back into a surplus—offsetting the capital outflows and keeping the net external position in a surplus.

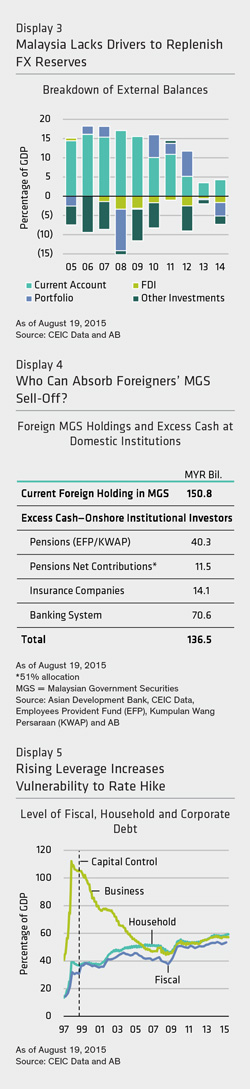

But now, Malaysia is suffering from a structural decline in the current account surplus that is exacerbated by deteriorating terms of trade and sluggish export demand—and there is no positive driver for improvement in sight (Display 3). Even if BNM reintroduced capital controls, foreign investors would merely unwind their positions after the holding periods expired, and BNM might remain under pressure from the risk of a portfolio outflow for years to come.

Disastrous Outcome of Capital Controls

The key argument for capital controls is that they would help to restore monetary policy autonomy. By imposing capital controls in 1998, BNM was able to cut its policy rate by 300 basis points to mitigate the economic shock from the Asian Financial Crisis.

At present, we are not seeing any liquidity stress in the domestic financial system. However, if BNM opts to impose capital controls, foreign investors are likely to promptly unwind their huge positions in Malaysian debt securities in a knee-jerk reaction. Foreign investors hold a staggering 46% of outstanding Malaysian Government Securities (MGS), the highest foreign ownership in Asia, and this will be the key to the vulnerability of the country’s external position. The amount of foreign holdings is greater than the excess cash holdings of pension funds, insurance companies and the banking system—the major investors that hold the other half of outstanding MGSs (Display 4). There is not enough onshore liquidity to digest an abrupt unwinding of foreigners’ MGS holdings.

As such, the consequence of a reintroduction of capital controls would be a sell-off in the domestic fixed-income market, which pushes up interest rates and threatens the highly leveraged economy (Display 5). This would defeat the original purpose of capital controls.

BNM’s Policy Options

All in all, BNM has limited policy options in responding to currency attacks. First, a rate hike to support the currency is not feasible—incremental adjustments would not be effective, while a significant monetary tightening would badly hurt the leveraged economy.

Second, intervention to facilitate an orderly exchange rate adjustment would not be sustainable, as BNM is running out of ammunition. With less than US$100 billion in foreign reserves, BNM would be fair game for currency speculators. The more actively BNM intervenes, the more incentive for speculators to further sell the ringgit.

A more likely outcome is for BNM to introduce macro prudential measures such as limits on short selling of the MYR or on banks’ foreign exchange derivatives exposure—similar to ones imposed by Indonesian and South Korean authorities before. Still, there’s a limit to how far BNM can go with this approach as it seeks to slow down the MYR weakness but not overreact and scare off foreign investors. BNM may be able to mitigate the downward pressure on the MYR but not reverse the currency’s trend. It will eventually need to allow the market to make adjustments on its own.

All in all, we believe that a reintroduction of capital controls will yield no benefit and only cause a spike in domestic interest rates, risking significant economic disruption. In the tail-risk scenario, where politics dictate, we think that investors should be alert not just for MYR volatility but also for a potential spillover to other Asian markets.

By Vincent Tsui, Economist, Global Economic Research, and Anthony Chan, Asian Sovereign Strategist, Global Economic Research, AB

———-