China’s efforts to stem the market crash have had limited success so far. In our view, attempts to boost domestic demand via the policy banks will only help prevent further economic damage, while a rebound in exports is also unlikely. However, we believe a nascent recovery in the housing market could provide a more effective boost to economic growth than the government-sponsored initiatives.

Since July, after the Chinese equity market crashed, Beijing has resorted to heavy market intervention to support local equities and the stability of the renminbi (RMB), which was devalued by 2% on August 11. These moves have not yet borne much fruit, and have instead exacerbated global anxieties and risk aversion. Investors remain stuck in risk-off mode and are increasingly worried that China might eventually engage in competitive devaluation (which we do not expect) and could drag the global economy into a downturn.

Indeed, all eyes are now on China’s policy response and its ability to reinvigorate an economic upturn. In our view, the current policy focus on boosting public demand via the policy banks will merely prevent further economic slippage at best; it doesn’t address the real problem—the lack of private sector demand that has been the economy’s most dynamic growth driver for years. On private demand, although we’re doubtful that an economic lift from exports is imminent, we believe that a recovery in housing demand will eventually drive construction activity, should the current market consolidation proceed smoothly.

Costly Interventions

We have described China’s liquidity injection to prop up equity-market valuations after the big fall as a “liquidity war” (Asian Perspectives: “China Eyes Liquidity War as Equities Gyrate,” July 10, 2015).

So far, this battle must have cost the government more than RMB1 trillion (US$156 billion). Unfortunately, the aggressive moves have failed to reverse the market’s direction. Since the 2% devaluation on August 11, the massive, almost daily intervention in foreign exchange markets may have cost an estimated US$200–250 billion in cumulative depletion of the People’s Bank of China’s reserve assets.

Conducting a tug-of-war with market forces can be a long-drawn process. This week, new rules were issued that will subject banks to a 20% FX reserve requirement for their forward long USD position against CNY. Such heavy-handed controls on onshore forex forward trading to curb capital outflows may help stabilize the market temporarily. But it may also be viewed by many as a backward reform step.

Liquidity isn’t the problem. With reserve assets of some US$3.6 trillion, China has ample liquidity provisions—as long as the battle doesn’t get too protracted. However, the more controversial aspect of the latest policy response is the growing reliance on policy banks to fund government projects (injecting capital by utilizing forex reserves). In our view, this effectively replaces the old mistake of allowing the surge of local-government debt directly through the mushrooming of local-government financial vehicles’ (LGFVs) borrowing from state commercial banks.

Infrastructure Is the Lead Again

In a way, these sources of financing are really the same. Policy banks or the banking system—which is dominated by the large four state commercial banks—are all state entities. So when money is borrowed, liquidity or liability is actually being transferred from one hand to the other. Still, the latest expanded funding via the policy bank channel will lead to greater use of China’s forex reserves (instead of parking most of it in US Treasury markets).

As a result, the central government will ultimately share greater fiscal responsibility while local government’s direct borrowing will be constrained (outside the still developing municipal bond market). Still, these moves will boost funding of targeted infrastructure investments, and those public projects that have been identified or prioritized but had been delayed by local officials because of fears about the anti-corruption campaign.

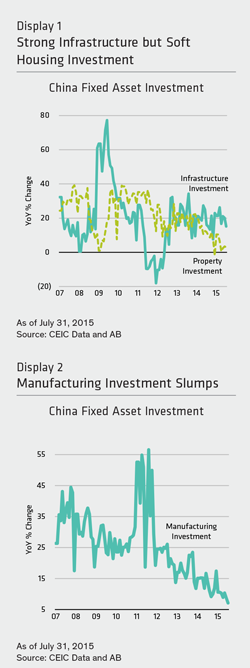

Infrastructure investment has already been growing at a relatively strong pace over the year. But, since it accounts for about 15%–20% of total investment, the overall impact on the economy has been quite limited (Displays 1 and 2).

And this is evident in the continued slowdown of economic activity over the past few quarters.

Private Demand Must Resume

Private demand from the housing market (i.e., investment plus the spillover effect onto commodity demand and household consumption of white goods, etc.) and manufacturing exports have been the main engines of China’s growth for decades. Once they slow, the downward spiral is significant, as seen in China’s current economic downturn. At this juncture, we do not see any light at the end of the tunnel in the current export down-cycle, given continued sluggish demand globally outside the US as well as the absence of a new export product cycle (Display 3).

Property is perhaps a brighter spot in China’s economic landscape. The housing market has genuinely been going through a market-based correction, with sales rebounding from a previous slump, an inventory correction underway and developers not rushing to kick start new projects too early in the cycle (Display 4). Of course, this recovery is still at an early stage. It remains to be seen whether stronger sales in major cities (such as Beijing, Shanghai and Shenzhen) will spill over into smaller cities in China, or whether liquidity provision will remain sufficient for housing purchases and developers’ investment appetite won’t be affected by a worsening economic environment or political uncertainty.

This potential rebound in the housing sector obviously won’t be enough to trigger a full-fledged economic recovery. However, since a housing rebound is driven by market dynamics, we believe that a recovery in this sector might provide a more efficient boost to China’s economic growth than all the government-induced investment projects.

By Anthony Chan, Asian Sovereign Strategist, Global Economic Research, AB

———-