As we approach the end of the year, our research is leading us to the view that we’re also nearing the end of an investment era, and the beginning of a new one. We expect this to be a global trend which will be positive for China, but with potentially negative implications for risk assets.

There are signs, though only tentative, that the global investment and policy landscape in fourth-quarter 2015 could lead to a reversal of what, three years ago, were three key market-shaping events.

Then, markets were in an expanding “balance sheet world”, in which central banks were pumping more liquidity into the global financial system to keep economies afloat.

In September 2012, the US Federal Reserve launched its third round of quantitative easing (QE); in December that year, Shinzo Abe became a second-time Prime Minister of Japan and, two months later, launched his Abenomics reforms in an attempt to boost the country’s growth and inflation.

The central banks hoped that, by helping to lift asset prices, they would reignite the “animal spirits” in their economies. An important consequence of these actions was that financial markets—particularly risk assets—became dislocated from the macro environment, as liquidity drove valuations higher than economic fundamentals warranted.

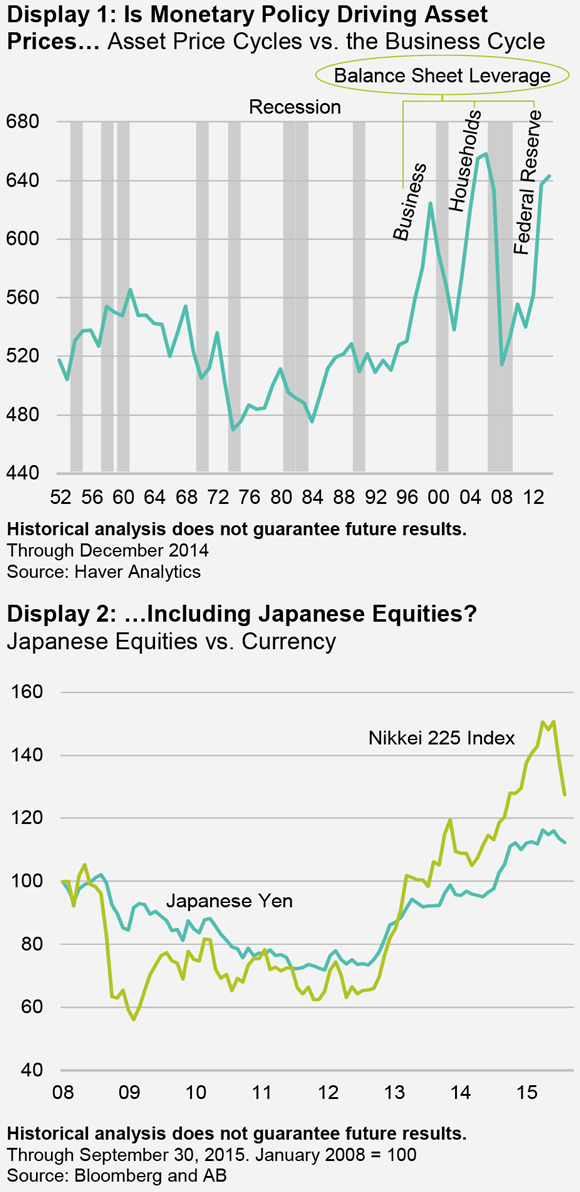

Display 1 shows asset price cycles (expressed as the ratio of household net worth to income) have become more dominant in the business cycle during the last two decades or so, at times of increased balance sheet leverage in various sectors. The most recent spike, beginning in 2012, coincides with the leveraging up of central-bank balance sheets.

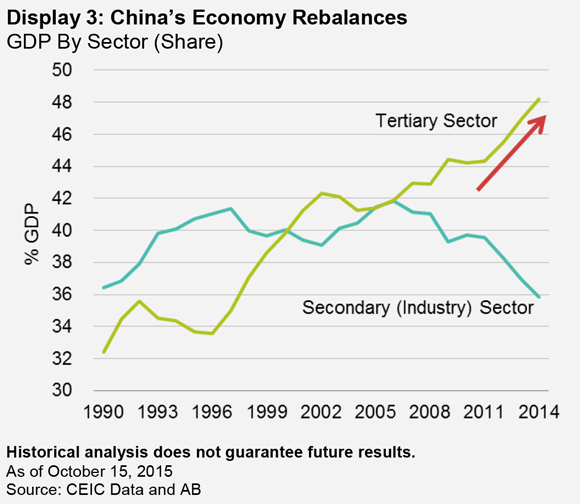

In Japan, equities have enjoyed a sustained rally until recently, beginning around the time that Abenomics was introduced in 2013 (Display 2).

At the same time, there was a counter-current to these events. In November 2012, Xi Jinping became President of China and—as part of a suite of reforms aimed at rebalancing the country’s economy—launched a crackdown on corruption.

As the US and Japan attempted to stimulate growth, Xi’s actions had a dampening effect, leading to a slowdown in infrastructure and other projects in China. This in turn effectively put an end to the global commodities boom and created economic headwinds for commodity-exporting countries.

All change

In October 2015, each of these three policy initiatives appears to be doing a U-turn. Having put an end to quantitative easing a year ago, the Fed—though weighing an improved US economy against global market volatility—is expected soon to raise short-term interest rates for the first time in nine years.

The policy debate in Japan now revolves around whether or not the Bank of Japan (BoJ) should ease further, with the BoJ governor arguing against it on the grounds that the country is through the worst of its deflationary spiral. If he’s right, we believe Japan could signal a tapering in its QE program next year. This is an out-of-consensus view as the market is still looking for an extension or top-up of the programme.

We expect China’s 13th Five-Year Plan, to be announced after the October Communist Party plenum, to focus on reforms that will continue to push the economy up the value chain, making it more efficient and innovative, with the aim of reducing the risk of the country falling into the middle-income trap.

We’re encouraged in this view by Xi’s recent engagement with the international community, including a state visit to the US in September and, more recently, the UK, with bilateral trade agreements high on his agenda. Premier Li Keqiang has been similarly active across Europe.

China, in other words, still seems to be moving in the opposite direction to that of the other countries in terms of policy—this time, however, it’s more pro-growth, while the US and Japan contemplate moving to tighter policy settings.

Macro factors back in play

Together, these trends point to a rebalancing in global markets during 2016. With the US poised to raise interest rates, Japan potentially tapering its QE and China experiencing a mild cyclical upswing, macroeconomic factors are likely to reassert themselves as key investment drivers, in our view.

For the riskiest assets which have been decoupled from fundamentals, this can only mean a reversion of valuations to more normal levels.

Silver lining in China’s clouds

While it may be too soon to rely on these straws in the policy wind as presaging a change in the global investment landscape next year, we see some fundamental trends— especially in China—which appear to support the case that such a change may occur.

This may seem unlikely, given that headlines about China’s economic growth continue to be overwhelmingly negative. The fact that the decline in China’s heavy industry sector is hurting western companies with significant exposure in that area is not to be taken lightly.

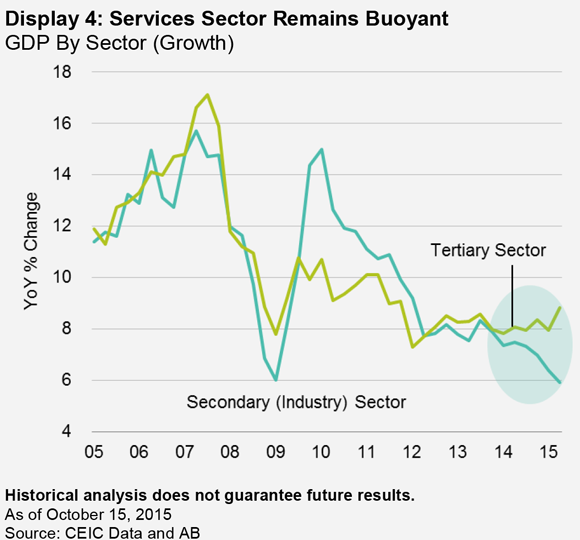

In our view, however, the headlines tend to overlook or underrate the key fact that the composition of China’s GDP growth has changed, as shown by Display 3.

The contribution of the secondary sector or industry— traditionally the main driver of growth—has declined as a share of GDP, while the tertiary (services) sector has boomed, to the point that it now accounts for 50% of GDP.

This is fully consistent with China’s goal of rebalancing its economy in order to avoid the middle-income trap, and counts as a major policy achievement. It’s good news for investors, because it points to more sustainable, if lower, GDP growth over the long term.

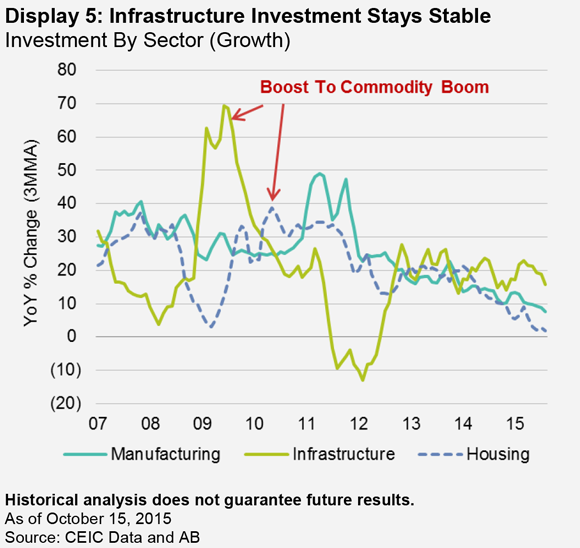

As Display 4, next page, suggests, year-on-year growth in services is buoyant, while the industry sector remains in a steep decline. That said, we detect some silver linings in the clouds hanging over China’s non-services sector.

Display 5 shows how growth in the infrastructure and housing sectors peaked during the commodity boom and how they have fared since President Xi came to power in 2012. Infrastructure has stabilised, while housing and manufacturing have continued to decline.

While we don’t see any turnaround in manufacturing in the short- to medium-term, we are more positive on infrastructure and housing. In the case of infrastructure, we expect the new Five-Year Plan at the very least to maintain investment at current levels and, possibly, to increase it.

There is any case a great deal of liquidity waiting to be invested in infrastructure—a result of the exponential growth in the municipal bond market, created earlier this year after the central government forced local and provincial governments to reduce their reliance on bank finance.

Current outstandings are RMB3.7 trillion (US$580 billion).

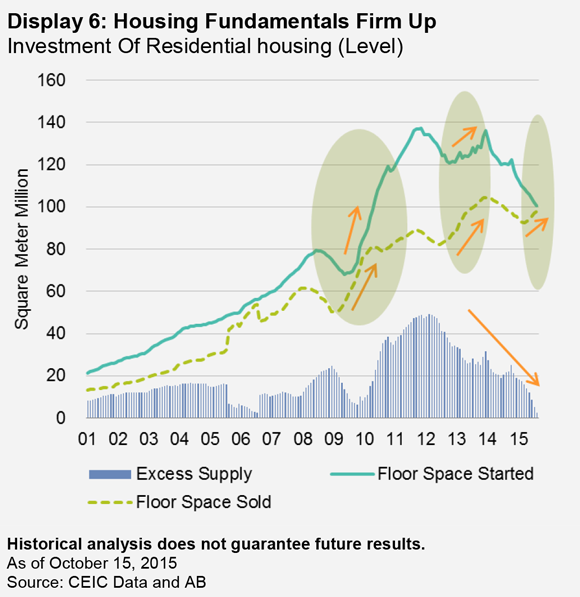

In housing, we see the possibility of a cyclical upswing, possibly by the middle of next year. Display 6 indicates that supply (as represented by Floor Space Started) and demand (Floor Space Sold) are now in balance, and that excess supply is diminishing steadily.

Our research shows that house prices in Tier 1 and Tier 2 cities have begun to rise, and that the trend is spilling over into Tier 3 cities.

If these trends continue into next year, we expect them to trigger a revival in property development. This will surprise the market, which has interpreted the downturn in the sector as the bursting of a bubble, rather than a cyclical change.

A revival in property development would also be supportive for the broader economy, in our view, and positive for the global commodities market—although we’re not suggesting that demand for commodities will return to anything like pre-2012 levels in the foreseeable future.

By Hayden Briscoe, Director, Asia Pacific Fixed Income, AB

———