Over the past five years, the average annual growth of 2.1% in real gross domestic product clearly fits the narrative of the new normal. Yet the economy’s recent performance has been impacted by “abnormal” factors as well, and their reversal in coming years should alter the parameters of the new normal pattern.

Economy Impacted by “New Normal” and Abnormal Factors

Proponents of the “new normal” for economic growth point to several factors that argue for a sustained period of subpar growth—at about 2% or so. These include slower productivity (lack of innovation and little new investment), slower labor force growth (decline in participation rate), tighter lending standards and higher capital requirements for banks, and relatively high debt levels for the private and public sectors.

Certainly, these economic and financial headwinds have been powerful and persistent over the past five years, and the new normal crowd has accurately captured their impact. But there are also two unprecedented—or abnormal—factors that have played an equal role in suppressing gross domestic product (GDP) growth.

Certainly, these economic and financial headwinds have been powerful and persistent over the past five years, and the new normal crowd has accurately captured their impact. But there are also two unprecedented—or abnormal—factors that have played an equal role in suppressing gross domestic product (GDP) growth.

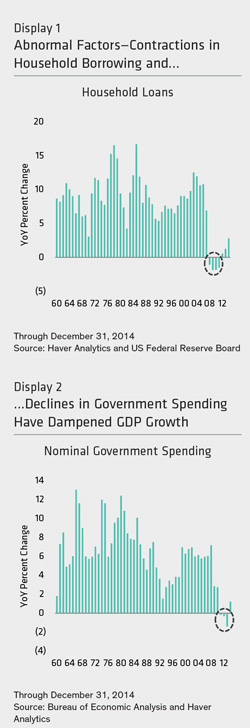

Once in a Generation or Even Longer

First, there was an outright contraction in household borrowing in two of the past five years (Display 1). This is unprecedented on its own, let alone during the start of a recovery. The only other years that household borrowing declined were 2008 and 2009—during the most severe market-induced credit crunch since the Great Depression. To be fair, the new normal crowd was correct in arguing that the household sector would delever and that would restrain spending and GDP growth. But the household sector’s classic deleveraging path consists of slower growth in borrowing relative to growth in income. Never before did household deleveraging include an outright contraction in borrowing. Moreover, the 1.0% cumulative change in household borrowing from 2010 to 2014 is the smallest gain in any economic recovery in the postwar era.

Second, nominal government spending in the GDP accounts declined in three of the past five years, also another first (Display 2). Here, too, the cumulative growth for the five-year period (2.0%) is the smallest gain of any recovery during the postwar era. Taken separately, each of these occurrences is a once-in-a-generation event, or even longer. The odds of both happening concurrently are something for others to figure out.

Gauging the Effect of the Abnormal Pullbacks

In order to illustrate the impact on the economy from each of these abnormal events, we estimated the elasticity of government spending to GDP, and of household borrowing to consumer spending—and the latter’s consequent impact on nominal GDP. (Note that these statistical results of estimating the impact of the growth in government spending and household borrowing on nominal GDP are not additive.)

Based on our research covering the last 60 years, the historical elasticity of government spending to nominal GDP is 1.07. That means a 1% growth in government spending would increase the growth in nominal GDP by a similar (just slightly higher) amount. And, if there had been no fiscal drag over the past five years, nominal GDP would have increased 1.4% faster each year. Thus, instead of an average annual growth rate of 3.8%, nominal GDP growth would have been 5.2%.

In terms of household borrowing and consumer spending, we estimate the historical average elasticity of borrowing to spending at 0.84. Thus, if household borrowing had merely matched the growth in disposable income since 2010, nominal personal spending would have increased 2.7% faster each year—and nominal GDP would have increased 1.9% faster, all else being equal.

Each of these abnormal factors directly exerted a powerful and persistent retarding influence on nominal GDP growth. And the deliberate maintenance of zero interest rates, along with the implementation of quantitative easing, by the Federal Reserve over the past several years was intended to offset these (and other) headwinds.

Resetting the New Normal Parameters

As the economy enters 2016, these abnormal factors are in the process of reversing their course. We expect that to be reflected in a faster pace of nominal GDP growth before very long.

On the government side of the equation, we can confidently conclude that the fiscal drag is over. State and local budgets are much improved, and nominal spending has been rising for two consecutive years. Additionally, federal government spending is poised to rise in 2016, given the recent congressional agreements on spending levels for defense and nondefense. It also appears that next week Congress will pass a five-year, $305 billion bill to fund highways and mass transit projects. This is the first multiyear highway bill in more than two decades, and most of the spending increase will show up in state and local government accounts, since the monies are disbursed to each state. Taking these developments together, we estimate that the growth in nominal government spending could increase 200 basis points in 2016—the largest acceleration since 1999.

Household borrowing has also started to increase at a faster rate. Indeed, according to the Federal Reserve Bank of New York, third-quarter US household borrowing increased $212 billion—the largest quarterly gain since 2007. And with lending standards becoming more relaxed and household balance sheets in much better shape, we will expect continued growth in household borrowing in 2016. Albeit, we don’t expect the household sector to relever (i.e., raise the growth in borrowing above that of income). But if households resume borrowing proportionately to underlying income growth, that will result in a 200-basis-point increase in the growth in borrowing, which will give a powerful lift to spending and GDP growth.

Next year should prove an interesting test of which factors—the new normal or abnormal ones—had the greatest impact in producing the economy’s subpar growth trends over the past five years. Certainly, both sets of factors were operative. But the abnormal factors appear to be reversing direction, moving from retarding to promoting growth.

Interestingly, that change isn’t currently reflected in the market or the Fed’s nominal growth and interest rate expectations. But that directional shift may be large enough to disrupt the new normal narrative before long. n

By Joseph G. Carson, US Economist and Director, Global Economic Research, AB

———