Portfolio diversification is one of the central tenets of modern portfolio theory. Along with fixed income and equities, both domestic and global, property is considered an essential inclusion in a diversified portfolio. In this article, DomaCom presents some findings from research undertaken by property experts Atchison Consultants, and discusses ways to simplify the inclusion of direct property in your clients’ portfolios.

Australians have long had a love affair with property – a home of one’s own forms the backbone of the ‘great Australian dream’; although for younger Australians, it seems that dream is slipping away. It’s because of this affinity with property ownership that Australians understand the value of direct property as an asset.

The benefits of investing in direct residential property

Property is an asset that resonates with everyone – we work in it, we live in it, we use it for our recreation. It’s a tangible asset we can see and touch. While some types of property can be accessed via listed vehicles or managed funds, there are a number of benefits that an investment in direct property offers that distinguish it from these other forms of property investment:

Return – the income from rent and capital appreciation from rising property prices is sourced from a single asset and is not diluted by under-performing investments in a portfolio.

Beneficial ownership – beneficial ownership means the investor is only responsible for the specific property they have invested in; this includes capital gains tax, stamp duty, land tax, maintenance, management and other costs.

Diversification – direct property offers diversification benefits, access to regular income and returns that are not correlated to listed assets; listed property and managed funds that invest in property securities are more closely correlated to equity market returns.

Greater control – because they own the property themselves, investors have control over how it’s managed, enabling them to make strategic business decisions to maximise profitability.

Tax benefits – there are potential tax benefits from direct ownership, with investors able to write off depreciation and claim tax breaks for maintenance and other costs; income from listed property is fully taxable, although some may pay partly or fully franked dividends.

Finance – there are a range of mortgages available to property investors and, now that borrowing can be undertaken within a self-managed superannuation fund (SMSF) structure, direct residential property is more accessible to all investors.

Low volatility – unlike the sharemarket, property prices do not fluctuate daily.

The return impact of investing in residential property

There are numerous benefits provided by investment in direct residential property. For all investors, the most important outcome is the contribution an investment makes to their overall wealth.

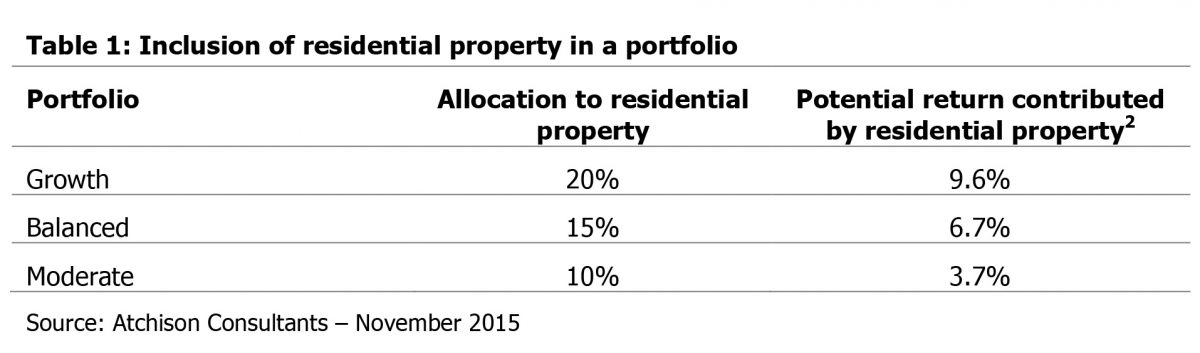

DomaCom recently commissioned Atchison Consultants to model the impact that an investment in residential property can have on three risk categories; moderate, balanced and growth.

Taking an average[1] asset allocation across domestic and international equities, fixed interest and cash as generally applied to moderate, balanced and growth portfolios as a base, Atchison’s research suggests that including 20% in residential property can enhance total returns on a growth portfolio by up to 9.6% over a rolling 20-year period.

[2] The asset allocation breakdown for each of the growth, balanced and moderate portfolios is based on the asset allocation of a typical portfolio of a similar nature as applied in the industry. The statistics were drawn from the average allocation of Super Fund managers from the Australian Superannuation Survey produced by a number of data providers.

The industry average allocation to direct property is very limited; typically, it is 3.8% in growth portfolio, 3.0% in a balanced portfolio and 2.9% in a moderate portfolio. As such, a 20%, 15% and 10% residential property allocation would necessarily result in proportional decreases in the allocation of other asset classes.

There is a downside

Direct residential property investment has some drawbacks, including:

It can be costly – transaction costs in direct real estate transaction costs are generally significantly higher when compared to other investment classes; stamp duty and other costs outweigh the brokerage and transaction costs of investing in listed property or funds. The ongoing maintenance required of direct property assets is an additional layer of costs.

Management – real estate investments require ongoing management, which comes at a cost; even if handled by the owner, it requires time and resources.

Property is expensive – it seems that not a day passes where the media reminds us that property prices are breaking records and moving beyond the reach of many. As a result, an investment in property can tie up a significant amount of capital.

Cyclicality – as will all asset classes, real estate is cyclical; however, residential property has been less effected by the cycles that impact commercial and industrial properties.

Liquidity – unlike listed property, direct property investment has a longer sales process and much longer lead time to return capital to the investor upon sale of the asset.

Fractional property investment

The negatives of an investment in direct residential property can be addressed by a new concept in property investment; fractionalised property investment. It enables investors to reap the benefits available from an investment in residential property, while mitigating some of the downside.

What is fractional investment?

The sharemarket is fractionalised investing. By breaking a company into shares, it makes it possible for investors to buy a portion of a company for a relatively small outlay. Similarly, fractional property investment is an asset allocation solution for the property asset class; it breaks property down into affordable segments, and enables investors to buy a portion of a property.

Fractionalisation provides financial advisers with an opportunity to easily invest a portion of their clients’ investment portfolio in direct property. Being able to offer this opportunity prevents clients from going ‘offsite’ to invest, and ensures you have oversight of their entire portfolio.

A secondary market in property fractionalisation means greater liquidity than is available when a client is the sole investor in an entire property.

Benefits of fractional property investment

The fractional model democratises property investment and enables many more people to invest in this asset class, with as little as $2,500. Other benefits of fractional property investment include:

- Scaled entry into property market, which is particularly important for Gen Y and Millennial clients, who may otherwise have limited opportunities to buy residential property

- Fractional investment allows a limited amount of funds to be spread across multiple property assets, providing diversification from different geographic locations and property types

- Fractionalised property is an asset of a registered managed investment scheme and the property title is held by a registered custodian; this provides security to buyers

- Each property asset is segregated into a sub-fund, so returns and costs pertinent to each property are kept separate and applicable to investors in that property only

- It offers advisers the potential for enhanced fees by including direct property investment in your offering to clients

- Savings can be transferred to fractional investment where it tracks the property market, rather than sitting in the bank earning low rates of interest.

Importantly, fractional property investment provides an opportunity for financial advisers to groom future clients from the younger generations looking for an entry level to property investment. The children of Baby Boomers and the upper end of Gen X are the next generation of accumulators; any measures you can take to help them build an investment portfolio that includes direct property will auger well for the future of your business.

[1] The asset allocation breakdown for each of the growth, balanced and moderate portfolios is based on the asset allocation of a typical portfolio of a similar nature as applied in the industry. The statistics were drawn from the average allocation of Super Fund managers from the Australian Superannuation Survey produced by a number of data providers.

[2] The residential return figures are calculated out of the REIA Housing Index produced by Atchison Consultant. The index is constructed based on the houses and units prices across all states and territories weighted by population.

———–