Using investment bonds to increase age pension and manage the intergenerational transfer of wealth

Utilising investment bonds to manage intergenerational transfer of wealth post 1 January 2017 may have the by-product of increasing Age Pension entitlements – Case Study Bob (78) and Margaret (68).

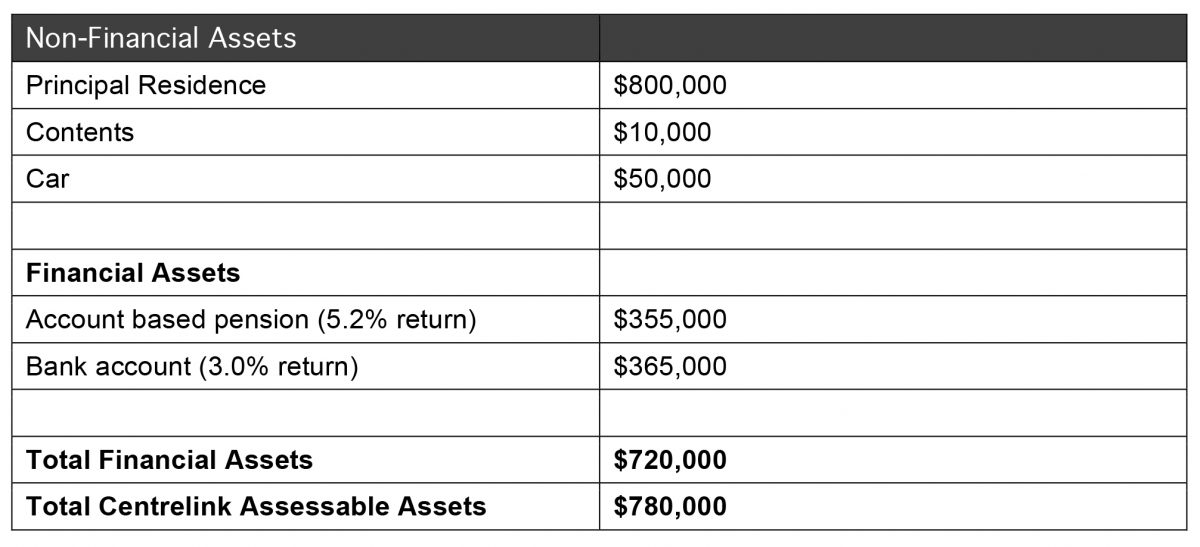

With changes to the age pension assets test that came into effect from 1 January 2017, existing part–pensioners may be considering their options to retain their current Age Pension entitlements. Let’s take a look at the options Bob and Margaret may consider. Bob and Margaret have total assessable financial assessable assets of $780,000, let’s review a number of options to assist maximising their age pension entitlements over the next 10 years.

Bob (78) and Margaret Smith (68)

Current financial and non-financial assets:

Let’s take a look at four strategies Bob and Margaret may want to consider:

- Retain their current investments in the current structure

- Purchase a lifetime annuity – $270,000 for Margaret and $100,000 for Bob.

- Purchase an investment bond in joint names with 1 Child $370,000 (3% net return after fees and taxes on the bond)

- Purchase an investment bond in joint names with 1 child $270,000 and $100,00 Annuity for Bob 3% return after fees and taxes on the bond)

Things to consider:

- Bob and Margaret’s estate planning needs

- Bob and Margaret’s cash flow needs

- Bob and Margaret’s risk profile

- Bob and Margaret’s health

Strategy 1 – Bob and Margaret retain their current investments:

Post 1 January 2017, Bob and Margaret’s Age Pension entitlement will drop from $15,526 (combined) to $3,456 Combined. As a result of retaining their assets in the current structures their Age Pension entitlement will reduce by $12,070 (combined) in the first year and a similar amount each year going forward as long as their assessable assets remain the same. If their assets increase over time they can expect their Age Pension entitlement to continue to fall.

The current structure provides Bob and Margaret with liquidity and access to their funds at any time.

Strategy 2: Bob and Margaret purchase 2 lifetime annuities for both Bob ($100,000) and Margaret ($270,000)

Bob and Margaret will receive a regular lifetime income stream from an annuity by investing in this structure. The annuities provide an asset test benefit for Bob and Margaret, and provide a cumulative increase in their Age Pension entitlements of approximately $44,022 over a 10 year period when compared to retaining their current investment structure.

The strategy may result in some liquidity limitations for Bob and Margaret and on death/withdrawal the funds are subject to a commutation.

Strategy 3: Bob and Margaret purchase an investment bond in joint names with a child for $370,000 (with a net return of 3% after fees and taxes on the bond.)

Through intergenerational planning by gifting to a child via joint ownership into an investment bond, there is a long term Age Pension benefit that results due to the deprivation rules associated with gifting.

Centrelink will assess deprivation on half of the $370,000 less the $10,000 allowable yearly gifting limit, but after 5 years deprivation will cease and Bob and Margaret would have removed $185,000 from Centrelink assets test assessment leading to an increase in their Age Pension entitlements.

The result is a cumulative increase in their Age Pension entitlements of approximately $95,886 over a 10 year period when compared to retaining their current investment structure.

The investment bond provides liquidity should funds be required for a new car, aged care needs or to fund a specific life event.

The estate planning benefits of the investment bond ensure beneficiaries receive proceeds tax free on death of the life insured.

Strategy 4. Investment Bonds joint names with 1 child – $270,000 in an investment bond and $100,000 Annuity for Bob

This strategy provides a blend of liquidity with the investment bond and the security of a lifetime income stream from the annuity whilst allowing the client to benefit from both the short term asset test benefits of the annuity and the long term asset test benefits of the investment bond strategy which are a by-product of forward thinking intergenerational planning.

In this scenario, Bob and Margaret would effectively remove over $135,000 of assessable assets after 5 years from both the Investment Bond structure and annuities combined.

Over a 10 year period this would result in a cumulative increase in their Age Pension entitlements of approximately $91.152 when compared to retaining their current investment structure.

Overall there are a number of opportunities to maximise age pension entitlements post 1 January 2017, a jointly owned investment bond may provide an asset test benefit after 5 years as well as provide certainty for estate planning purposes.

Important note: Projections are based on pension rates based on current legislation as at 1st January 2017, an investment bond yield of 3% after fees and taxes, an annuity payment of 5% of purchase price for Margaret and 6% for Bob, lifestyle expenditure of $40,000 p.a. and inflation at 3%. These assumptions have been selected for illustrative purposes only and no representation is made by Centuria Life Limited as to whether these returns are achievable within the product classes. Different returns will alter the outcomes. It is recommended that financial advisers determine and run their own assumptions for the the strategies presented.

———–