Millennials – otherwise known as Generation Y – comprise the fastest growing segment of the Australian workforce. Although there are more than five million millennials in Australia, approximately 20% of the population, they are less likely to seek financial advice or own their own home than preceding generations.

In this article, DomaCom examines the factors that make millennials so different from their parents, the baby boomers, and outlines strategies that advisers can use to engage with this generation.

Meet the millennials

Millennials get a bad rap – they’re entitled, opinionated and expect to be rewarded for doing little. In the workplace, they’re lazy and disengaged, while expecting regular promotions and financial rewards.

Who are the true millennials and what makes them so…well, millennial?

Millennials were born between 1982 and 1999, children of baby-boomers, or older Gen X. They’re generally highly educated, very tech savvy and happy to share their lives and opinions on social media. They’re the generation where everyone got an award and everyone was ‘special’. They are not used to hearing ‘no, you can’t do that’ because for years, they’ve been told they can do anything. When aspirations and the real world collide, the reality check isn’t always pleasant.

Despite their earning capacity – household income is growing faster than any other demographic – our millennials are not optimistic. The 2017 Deloitte Millennial Survey[1] found that millennials in emerging markets are more upbeat and generally expect to be materially better off than their parents. This contrasts with mature markets where many millennials feel theirs is the generation where things stopped getting better.

In fact, just 8% of Australia’s millennials believed they would be better off financially than their parents – and only 4% believed they would be happier. From a global perspective, 26% believed they would be wealthier than their parents and 23% said they’d be happier.

What’s the cause and effect of such beliefs? According to the survey:

“Young Australians were also found to be more pessimistic about their financial and emotional wellbeing than their global counterparts, due to their uncertainty of ever owning a home and having little faith in the country’s political future.”

The property conundrum

In general, millennials have shown a preference for property over shares – they understand property, perceive it as less risky, and importantly, they have seen their baby boomer parents benefit from the massive capital appreciation of their homes – growth that has resulted in Australian property being amongst the most unaffordable in the world[2].

According to Demographia’s global study, three national markets are rated as ‘severely unaffordable’ – China (including Hong Kong), New Zealand and Australia.

Despite millennials earning a good income, getting on the property ladder is next to impossible. The cost of living has risen enormously during their lifetime and many start work with a significant HECs debt. Add to that the ease of credit that has perpetuated the ‘have now, pay later’ mentality, buying into the great Australian dream has never been harder. And in the meantime, the price of housing keeps rising.

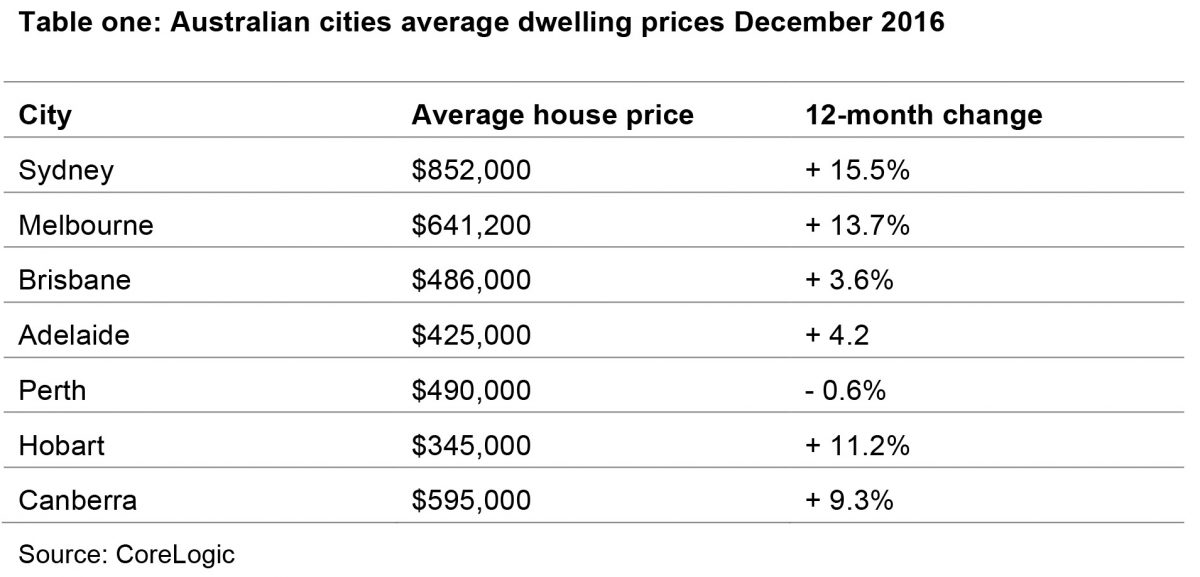

According to CoreLogic, prices in Sydney have jumped by 97.5% since January 2009; Melbourne was close behind, with an increase of 83.5%. In other words, in less than 10 years, the average house price in Australia’s two major cities has nearly doubled.

Over a similar time period, salaries have not kept pace. While a house in Sydney increased by an average of $10,000 per month last year, the average weekly wage increased by a modest $15 between January and December.

Then there’s the deposit. Most banks pay less than 3% on savings (less after tax), they require at least a 20% deposit (plus costs such as stamp duty) for a mortgage…it’s no wonder that most millennials despair about home ownership.

Where do millennials invest?

Millennials aren’t all spendthrifts and a number have embraced investment. The overseas experience suggests this demographic is largely driving the take up of robo advice, and, in Australia, the stellar growth of the round up app Acorns is largely down to millennials. This style of investment seems to appeal.

Using Acorns as an example, this app allows users to hook up debit and credit cards and it then ‘rounds up’ each purchase to the nearest dollar. The proceeds are invested in a basket of ETFs in $5 increments, based on the risk profile of the investor. Additional amounts can be invested regularly or on an ad-hoc basis. Acorns recently added ‘found money’ whereby users can shop online with select merchants and receive a bonus in their Acorns account.

It’s simple, it doesn’t require years of saving to get invested, and it harnesses a medium familiar to millennials – technology.

How can financial advisers work with millennials?

As their parents continue to retire and draw down on their savings, millennials will become the next generation of accumulators. They won’t have the benefit of significant capital gains in their home (if they own one at all), nor will they have bought today’s blue chip stocks at IPO. However, they will earn a solid income and need to accumulate wealth for their future.

There are ways that savvy financial advisers can attract this demographic. In the same way that Acorns is fractionalised investment – it breaks a basket of ETFs into small pieces, so it can be purchased in increments – so too can residential property.

Fractional property investment breaks property down into affordable segments, and enables investors to buy a portion of a property…thereby enabling millennials to get a foot onto the property ladder. Millennials understand property and want to invest in it – this is a simple means to that end.

Benefits of fractional property investment

The fractional model democratises property investment and enables many more people to invest in this asset class, with as little as $2,500. Other benefits of fractional property investment include:

- Scaled entry into the property market, particularly important for millennial clients, who may otherwise have limited opportunities to buy residential property

- Fractional investment allows a limited amount of funds to be spread across multiple property assets, providing diversification from different geographic locations and property types

- Fractionalised property is an asset of a registered managed investment scheme and the property title is held by a registered custodian; this provides security to buyers

- Each property asset is segregated into a sub-fund, so returns and costs pertinent to each property are kept separate and applicable to investors in that property only

- Savings can be transferred to fractional investment where it tracks the property market, rather than sitting in the bank earning low rates of interest.

Fractionalised property investment provides an opportunity for financial advisers to groom future clients from the younger generations looking for an entry level to property investment. The children of the retiring baby boomers are the next generation of accumulators; any measures you can take to help them build an investment portfolio that includes direct property will help position your business for the future.

[1] http://www2.deloitte.com/global/en/pages/about-deloitte/articles/millennialsurvey.html

[2] Demographia Housing Affordability 2017

——-