The global economy is on a ‘hot streak’, with a string of positive data surprises feeding expectations for further strengthening. But is momentum really as strong as it first appears?

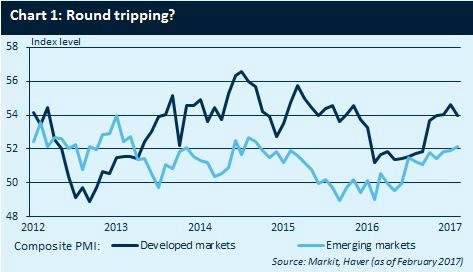

When we break down PMIs by region, it is clear that despite nine months of consecutive gains in the advanced economies – a time in which the composite PMI jumped from 51.4 to 54.6, sentiment is still only marginally above the level 12 months ago.

Indeed, what the pattern in the data mostly reflects is a rebound following the collapse in sentiment in early 2016 (see Chart 1).

For EM, the rebound has been more persistent, if somewhat bumpier, but still only pushes sentiment back to the levels of late 2014. So are the benefits of an easing of distress in the commodities complex and inventory restocking being misconstrued as cyclical recovery?

While it would be remiss not to recognise the low starting base, there are a number of distinctive improvements in the economic data that suggests the global upswing is the ‘real deal’.

First, the disconnect between buoyant PMI readings and more pedestrian industrial activity has started to fade.

Advanced economies’ production surged towards the end of last year, and core manufacturing components have remained strong, even as the latest headline prints in the US and Germany saw a mild correction. Second, there are signs the corporate capex drought is coming to an end.

This partly reflects the improving earnings environment, but also signals that private sector deleveraging has bottomed.

The jump in equipment investment in Japan and the US in the Q4 national accounts data corroborates the trend.

Looking forward, the indicators for the technology and manufacturing investment cycle bode well, even if gas and oil investment were to plateau.

Finally, trade dynamics point to a meaningful acceleration in global demand. Here too, we should be cautious about the impact that rising commodity prices can have on inflating trade values.

A better indication comes from trade volumes, but they too have turned a corner, jumping 3.5% in H2.

The omens for Q1 are also encouraging with carried over growth expected to push global volumes up 1.2% on the quarter, while our favoured trade bellwether, Korean exports, saw a 11.2% y/y volume jump on a seasonally adjusted sequential basis.