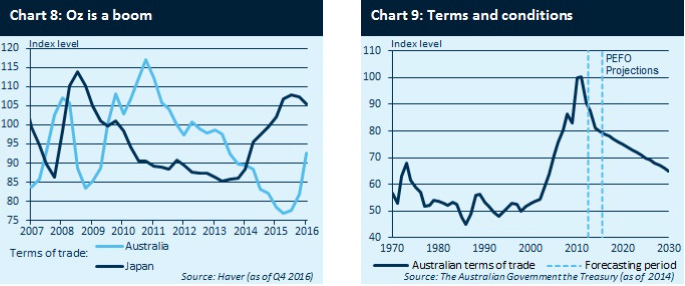

Given a diversity of factor endowment and a relatively high openness to trade, the rebound in commodity prices over the last 12 months has had contrasting effects on economies within Developed Asia. The easiest way to quantify these effects is to look at changes in the terms of trade.

This concept focuses on the relative price of exports to imports and seeks to quantify the domestic purchasing power of an economy and its competitiveness abroad. Using this metric, it is no surprise that Australia emerges as the biggest beneficiary of higher commodity prices (see Chart 8).

The nation’s trade balance has soared, with total exports up 29.7% y/y in February driven by iron ore, coal and natural gas exports. Furthermore, one would expect improving national income to translate into better spending and investment. Looking at the hard data though, the evidence that terms of trade effects are spilling over to domestic activity remains somewhat scant. Retail sales remain sluggish, falling 0.1% m/m in February, while the latest labour report offered little encouragement with unemployment ticking up to 5.9%, while wage growth remains stagnant. Elsewhere, the improvement in corporate cash flow has also been slow to translate to higher wages or capital investment.

On the latter, the Australian Bureau of Statistics’ private capex survey pointed to plans to reduce capex in 2016-2017 and 2017-2018, with mining investment expected to fall by -20% in FY2018. Despite the tepid response from the domestic economy so far, we continue to see Australia as a beneficiary of the global cycle.

Elsewhere in Asia, the repercussions of improving commodity price trends are less clear. As a major commodities importer, Japan proved a key beneficiary of the collapse in commodity prices, with the terms of trade turning positive in September 2015.

However, rising oil prices and a weaker yen meant that the terms of trade narrowed in Q4 last year and turned negative in January. Higher import prices have been associated with weaker consumption and downward pressure on corporate earnings in the manufacturing sector.

However, recent episodes have been triggered by significant currency weakness, rather than commodity price changes. With the currency having stabilised at a level close to the estimated breakeven rate for Japan’s manufacturing sector of ¥110, the impact on corporate profit margins may be limited. If the yen was to see another rapid decline, one suspects the translation effects might be more severe.

Given the importance of the terms of trade to economic activity, can investors avoid being blindsided by volatile commodity price movements? The typical method of forecasting a country’s terms of trade is to identify which goods or services are the most powerful determinant on the terms of trade in the past.

In Australia’s case, non-rural bulk commodities such as iron ore and coal tend to have the biggest impact on the terms of trade. The next task is calculating some form of future demand and supply curve based on mining activity and producer’s cost structures and structural and cyclical estimates of future commodity demand. Using these techniques, the government’s latest estimate is for a fall of around 16% to 2017-2018 (see Chart 9). Caution is probably still wise, but if the global cycle continues to improve we may expect Australian activity to surprise on the upside.