In April 2015, Business Insider ran a story ‘A crowdfunding revolution is coming to Australia’[1]. That revolution has not only arrived, it is well established and growing exponentially. In this article, DomaCom looks at crowdfunding – what it is, how it works, and how it will change the investment landscape.

Crowdfunding is the practice of raising funds through the use of internet platforms, subscriptions, events, and other methods to find supporters and raise funds for a project, person, cause or enterprise.

While today’s crowdfunding burst onto our computer screens earlier this decade, it has been a widely-used method of fund raising for many years. In 1885, the Statue of Liberty was lying prone, and no one in government wanted to fund the building of a monumental base for what is now arguably the nation’s most significant landmark. In stepped publisher Joseph Pulitzer. He launched a fundraising campaign in his newspaper, The New York World and raised more than the $100,000 required from 160,000 donors in five months[2].

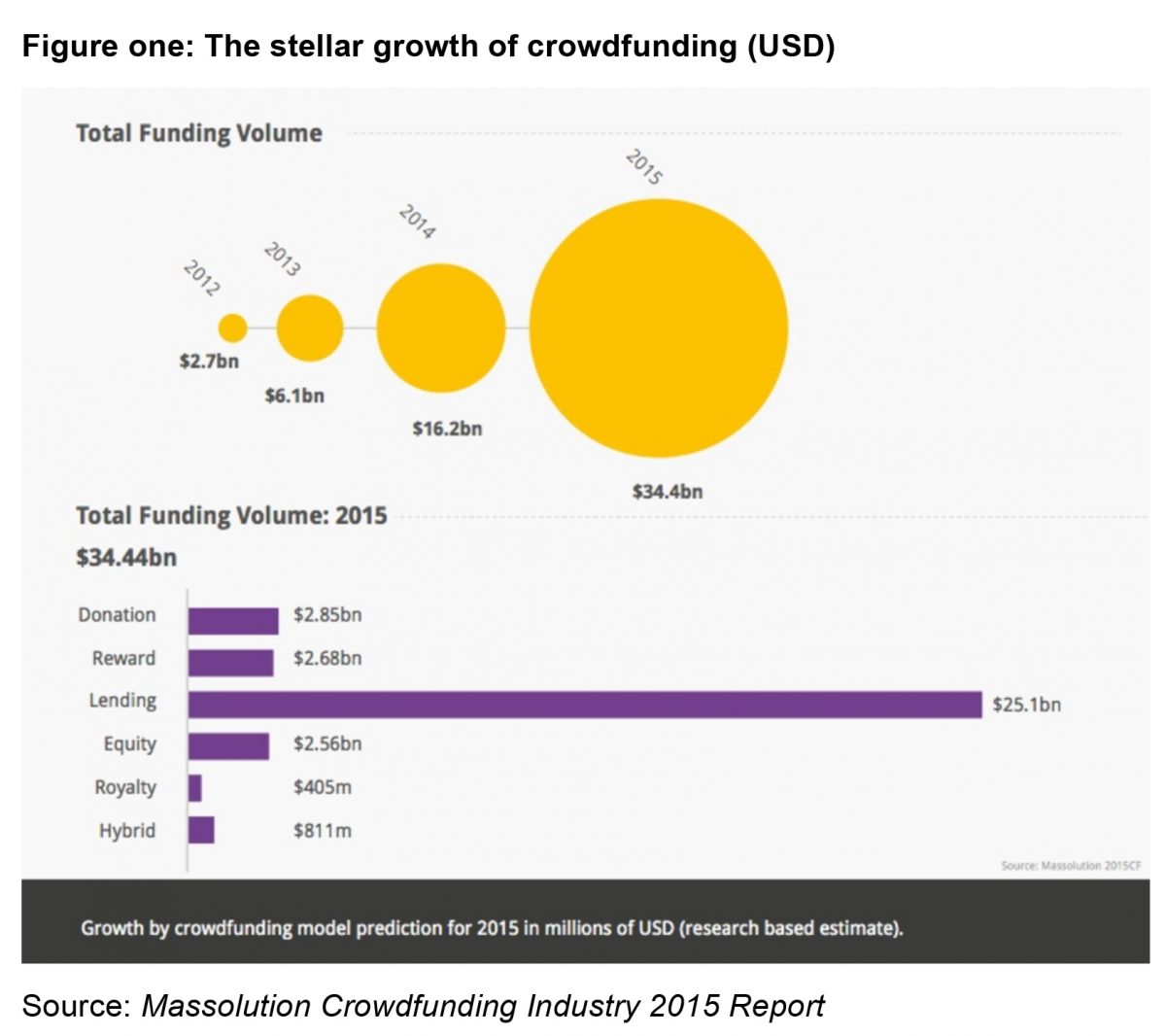

The advent of technology and the burgeoning fintech industry has simplified crowdfunding and turned it into a growth industry. According to the Massolution Crowdfunding Industry 2015 Report, total funds raised through crowdfunding in that year were estimated to surpass US$34 billion. In another report, Global Crowdfunding Market 2016-2020, analysts forecast the global crowdfunding market to grow at a compound annual growth rate of 26.87% from 2016-2020.

Figure one illustrates the incredible growth trajectory of crowdfunding. From approximately 700 crowdfunding platforms and $US2.7 billion in 2012, through to 2,000+ platforms and $US34.4 billion in 2015.

Crowdfunding – who, what and why!

There are usually three participants in a crowdfunding arrangement:

- The initiator of the project, usually referred to as the promoter

- The organisation providing the platform, generally known as the intermediary

- The individuals that contribute money, often referred to as contributors.

There are several categories of crowdfunding; in Australia, it falls into four broad categories:

Donation-based crowdfunding is the philanthropic end of the spectrum, where a contributor makes a payment, or donation, to a project, person or venture. Nothing is generally received in return – except of course the good feeling that comes with supporting a worthy cause.

Reward-based crowdfunding, where the promoter provides a reward to contributors in return for their payment, rather than receiving equity in the business or project. For example, a contributor supporting a musician may receive free music downloads, or a tech company might provide free or discount software.

Equity-based crowdfunding is where the contributor makes a payment in return for equity in the underlying asset, project or venture. Until recently, Australia was lagging its overseas counterparts in this area. However, in March this year, equity crowdfunding legislation was approved by the federal Parliament, after more than two years of industry consultation and debate.

This year’s Federal Budget took it one step further and extended equity crowdsourcing to proprietary companies; private companies will be able to raise up to $10,000 from retail investors who may benefit in many of the same ways as those investing in ASX-listed companies – in other words, the rights to participate in future profits, to vote and to returns of capital should the company be wound up.

Debt-based crowdfunding, where the contributor lends money to the promoter who, in return, agrees to pay interest and repay the principal at the end of an agreed period of time. This is also called peer to peer (or P2P) lending.

Where’s the money coming from?

According to a 2015 study by Goldman Sachs[3] millennials are more likely to participate in crowdfunding. A survey conducted by the investment bank in the US found that:

- 47% of Millennial respondents have backed or are likely to back a crowdfunding campaign, compared to

- 30% of Gen-Xers

- 13% of Baby Boomers

- 4% of Matures.

Whether it’s helping millennials get a toe-hold into the residential property market or taking an equity stake in a start-up, crowdfunding presents opportunities for financial advisers to engage with millennials.

Crowdfunding opens the door to investment opportunities

Agriculture

Globally, a number of crowdfunding platforms have been launched to enable contributors to donate to, or invest in, agriculture-related opportunities.

San Francisco-based AgFunder is an equity crowdfunding platform, founded in 2013, to connect investors with high growth agriculture technology and food technology companies. Investors receive equity in return for their investment.

Closer to home, DomaCom attracted more than 5,000 backers for its crowdfunding bid for the Kidman pastoral business. Investors and farmers rallied behind DomaCom, and pledged more than $80 million for the iconic property. Whilst the Kidman campaign was not successful, DomaCom recently crowdfunded a beef cattle property in western Victoria with 92 investors contributing to the acquisition. They will share in the 4% gross rental yield and ongoing capital growth in the property.

The interest generated by the Kidman opportunity has presented other agricultural investment opportunities. The world’s population is growing and so too is the need for agricultural production. Sourcing capital is one of the most critical areas for Australian farmers to drive efficiency gains to increase scale and productivity. However, debt levels are already high and farmers have had difficulty accessing the alternative sources of funding required to fill the capital gap.

Through crowd funding, Australian farmers can apportion part of their farm to investors and lease it back; that way they have the capital to introduce innovation and increase the farm’s value, which in turn adds value for investors.

Philanthropy and civic projects

A variety of crowdfunding platforms have emerged to allow contributors to support a range of specific projects, without needing to spend large amounts of money. Many of these projects tend to be donations – an individual raising money to cover medical costs, or a charitable platform supporting microbusinesses in developing nations. There are, however, investment opportunities in this sector.

There is a proposed solar farm project in country NSW that may seek investors via crowdfunding to acquire a property. Such a project could enable entire towns to become solar powered with surplus energy sold back into the grid.

There are other proposed civic projects in regional centres such as crowdfunding to build entertainment venues, sporting or other facilities that local governments can’t fund.

Real estate

Australians have long had a love affair with property – a home of one’s own forms the backbone of the ‘great Australian dream’; although for younger Australians, it seems that dream is slipping away. It’s because of this affinity with property ownership that Australians understand the value of direct property as an asset.

Crowdfunding in this asset class has democratised property investment and enables many more people to invest, with as little as $2,500. Benefits of this model include:

- Scaled entry into property market, which is particularly important for Gen Y and Millennial clients, who may otherwise have limited opportunities to buy residential property

- Crowdfunding allows a limited amount of funds to be spread across multiple property assets, providing diversification from different geographic locations and property types

- It offers advisers the potential for enhanced fees by including direct property investment in your offering to clients.

There are several options available to Australian investors in this space; importantly, there are two quite distinct models:

Fractionalised property – a property is ‘broken down’ into affordable segments or fractions, which enables investors to buy a portion of a property. Fractionalisation provides financial advisers with an opportunity to easily invest a portion of their clients’ investment portfolio in direct property and the client owns equity in the property. Fractionalisation in this way enables advisers to control the asset allocation to high value assets. DomaCom are looking to add corporate bonds to their stable of fractionalised assets.

Peer to peer (P2P) – in this model, the investor is making a loan to the property investor, in return for interest payments and return of capital at an agreed time.

When reviewing crowdfunded property investment options, it is important to ensure:

- The crowdfunding platform has a robust legal structure and the property is an asset of a registered managed investment scheme, with the property title held by a registered custodian; this provides security to buyers

- Each property asset is segregated into a sub-fund, so returns and costs pertinent to each property are kept separate and applicable to investors in that property only

- The platform has a liquidity facility available, whereby investors can sell all or part of their property unit holdings if necessary.

Crowdfunding opens the door for investors to access a variety of investment opportunities outside of the more traditional listed investments or managed funds. Importantly, investment opportunities that arise through crowdfunding provide financial advisers with a medium that is of interest to clients from the younger generations.

Whether they are looking for an entry to property investment, or wish to invest in something a little more left field, the children of Baby Boomers and the upper end of Gen X are the next generation of accumulators. Any measures you can take to help them build an investment portfolio that includes direct property and other crowdfunded investment opportunities will auger well for the future of your business.

[1] http://www.businessinsider.com.au/a-crowdfunding-revolution-is-coming-to-australia-heres-what-you-need-to-know-2015-4

[2] http://www.bbc.com/news/magazine-21932675

[3] Goldman Sachs Future of Finance Study 2015

———-