What are managed futures and how they can be an alternative asset class to add value to an investor’s portfolio.

During certain periods of time, managed futures can capture upward and downward trends in traditional markets; this has made this asset class a popular ‘alternative’ investment for financial advisers looking for assets that are uncorrelated with the traditional equities, bonds and property.

Grant Samuel Funds Management (GSFM) has recently partnered with Man Group to offer its managed futures fund to advisers and their clients. In this article, GSFM examines this alternative asset class and how it can add value to an investor’s portfolio.

The one predictable element about capital markets is that they are generally not predictable. Instead, they are often driven by human emotion and unforeseen events; even those who correctly predicted the global financial crisis (GFC) failed to anticipate the extent of its impact. Its ongoing effects have destabilised economies and markets, pushed interest rates to record lows and ushered in a raft of regulatory change world-wide. It was a period characterised by underperformance of all traditional, and many alternative, asset classes. The expected relationships between different asset classes broke down as each seemed to compete in the race to the bottom.

What are managed futures funds?

Sometimes known as Commodity Trading Advisors (CTAs), managed futures managers employ systematic trading programs to exploit persistence in the direction of price changes – or trends – in capital markets.

Managed futures funds invest in global futures markets and seek to profit from the pursuit of trends and movements in a range of assets that include currencies, interest rates, equities, metals, energy and agricultural produce.

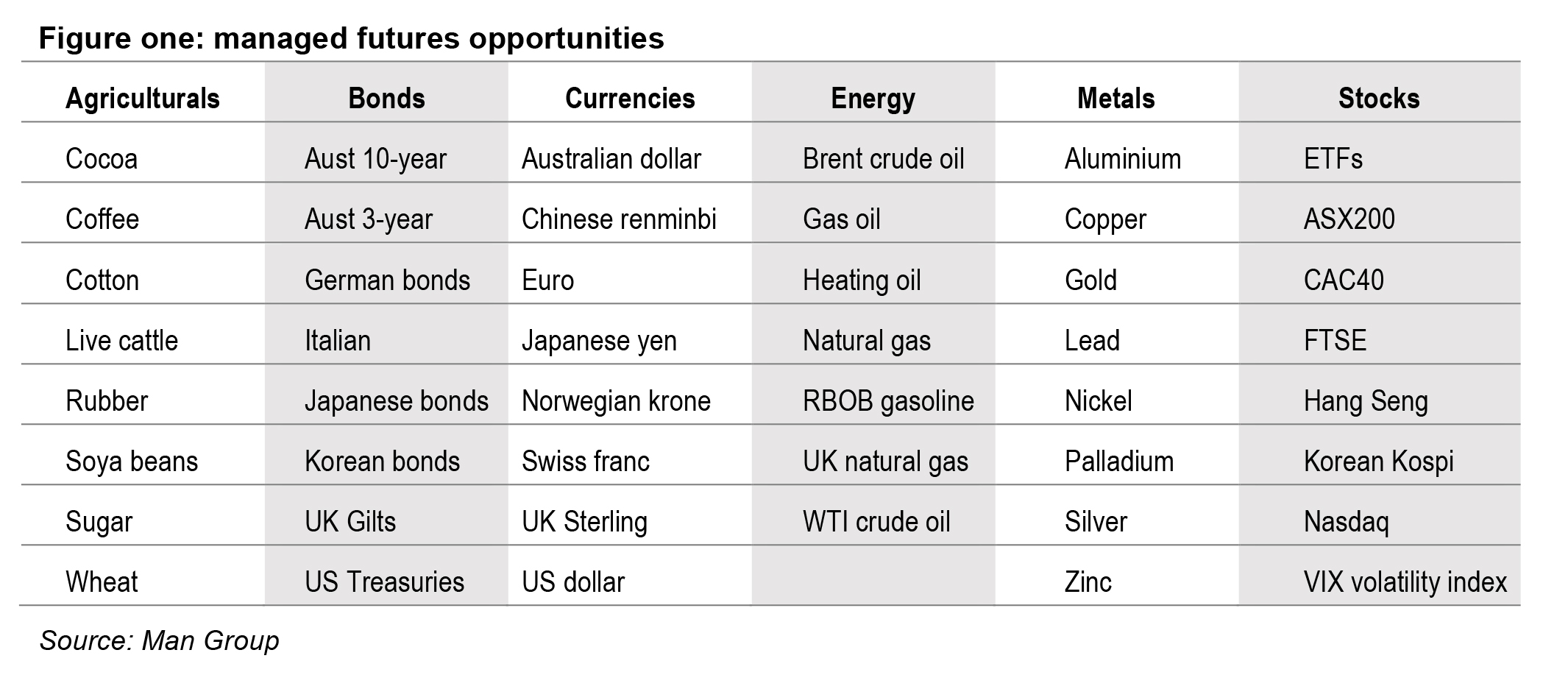

The standout feature of managed futures funds is the sheer range of opportunities that can be accessed through a constantly-evolving universe of futures contracts, each component of which can be traded both long and short. Figure one provides a snapshot of some of the many investment opportunities available to managed futures funds.

Variances in opportunities traded are one of the key differentiators between managed futures funds; some funds invest only in exchange traded futures contracts, while others include an exposure to over the counter contracts, which in turn opens a myriad of trading opportunities.

Futures: exchange traded vs over the counter

Exchange-traded futures contracts are transacted on an organised futures exchange, such as the Sydney Futures Exchange. They are standardised contracts and require a deposit or margin settled through a clearing house.

Over the counter – or OTC – futures are trades that take place between a buyer and a seller outside of a formal exchange

Why futures?

Futures trading takes place in very liquid markets; as a result, it’s relatively simple to calculate net asset values from market prices throughout the day and consequently, the pricing of managed futures is transparent and the funds themselves are liquid.

The use of futures contracts allows a fund manager to take many more different investment exposures for any given amount of capital than would be possible from investing solely in the underlying assets. Although each position is not individually ‘hedged’ in the true sense of the term, the blending of many different themes within one portfolio provides investors with a form of structural hedging.

A further advantage that managed futures funds can lay claim to in the most severe market environments is that there is always a sense of functionality in the trading arena. For every long contract that exists, there must, by definition, be an equivalent ‘short’, and vice versa. This natural balance means that futures exchanges seldom experience the disequilibrium and illiquidity that has plagued capital markets during the peaks of the GFC.

Following the trend

Managed futures funds can harness profits through following trends that arise as a result of a variety of unrelated phenomena, including slow macro cycles, carry, behavioural biases and the uneven dissemination of, and reaction to, market-relevant information.

1. Slow macro cycles

Some of the strongest trends in futures markets coincide with phases of macroeconomic cycles. The business-cycle itself is characterised by momentum; individuals smooth their consumption expenditures, firms make long-term decisions to commit to investment projects, wages and employment are sticky and the government sector explicitly tries to smooth fluctuations. Likewise, emerging markets take time to emerge, and do so with predictable rises in consumption and demands on industrial commodities. Such macro trends manifest themselves in the prices of many financial instruments, and trending behaviour can arise if the underlying economic factors are not fully discounted by the market.

2. Dissemination of and reaction to information

Economic and other news disseminates unevenly; different market participants react only when such news reaches them, each potentially having their own reaction rate. For example, high-frequency traders typically react to events almost immediately, whereas large institutional investors may require a lengthy decision-making process, and retail investors may take longer again. Periods of sustained buying or selling develop as news spreads and participants react in similar ways but over different time-horizons. This effect leads to persistent trends.

3. Behavioural biases

Market participants often exhibit consistent but seemingly non-rational behaviours. Some of the more well-known behavioural biases include:

- holding losing trades too long in the hope they will come good

- closing winning trades too soon

- under-reaction, leading to sequences of incremental actions

- crowding/herding – in other words, buying because everyone else is buying.

Behavioural biases which lead to individuals losing money or foregoing profits, such as the first two examples above, are effects where a systematic trader, uninfluenced by emotion, can profit either by taking the other side of the trade or holding onto a winning trade when others have closed out. The second two examples lead to explicit trends as partial reactions and herd behaviour can induce sustained price momentum.

4.Carry

Carry represents the return earned for holding a financial asset or portfolio if the ‘world stays the same’ and is a key driver of momentum returns. It is greatest for systems targeting longer-term trends (six months or more) in markets which themselves have strong carry returns.

To understand how carry finds its way into momentum returns, consider an asset with an upward sloping forward curve. If the curve retains its shape, the futures price will naturally slide down the curve, creating a negative drift (trend) over time. Conversely a downward sloping curve can create a positive trend. Thus, carry can generate momentum in futures prices even without trending behaviour in the underlying spot price.

Five benefits managed futures can offer

1. Diversification

Managed futures provide diverse investment opportunities across geography, asset class and sector. As illustrated in figure one, exposure may include agricultural commodities, energy products, metals, interest rates, equities and foreign and domestic currencies. The use of futures contracts also allows the manager a much more diverse exposure for a given amount of capital than would be possible from investing solely in the underlying assets.

2. Reduced portfolio volatility

An appealing characteristic of trend-following managed futures funds is that they are uncorrelated with equities; managed futures funds generally exhibit a negative correlation when equity markets trend lower. This means that they can actually counter, rather than merely cushion, the impact of a sharp downturn on an investment portfolio.

3. Transparency and liquidity

Tight regulations result in maximum transparency for investors and the very liquid investment arena means it is simple to calculate net asset values throughout the day. Consequently, the pricing of managed futures is transparent and the funds themselves are liquid, an unusual attribute for a ‘low correlation’ investment.

4. Returns in all market conditions

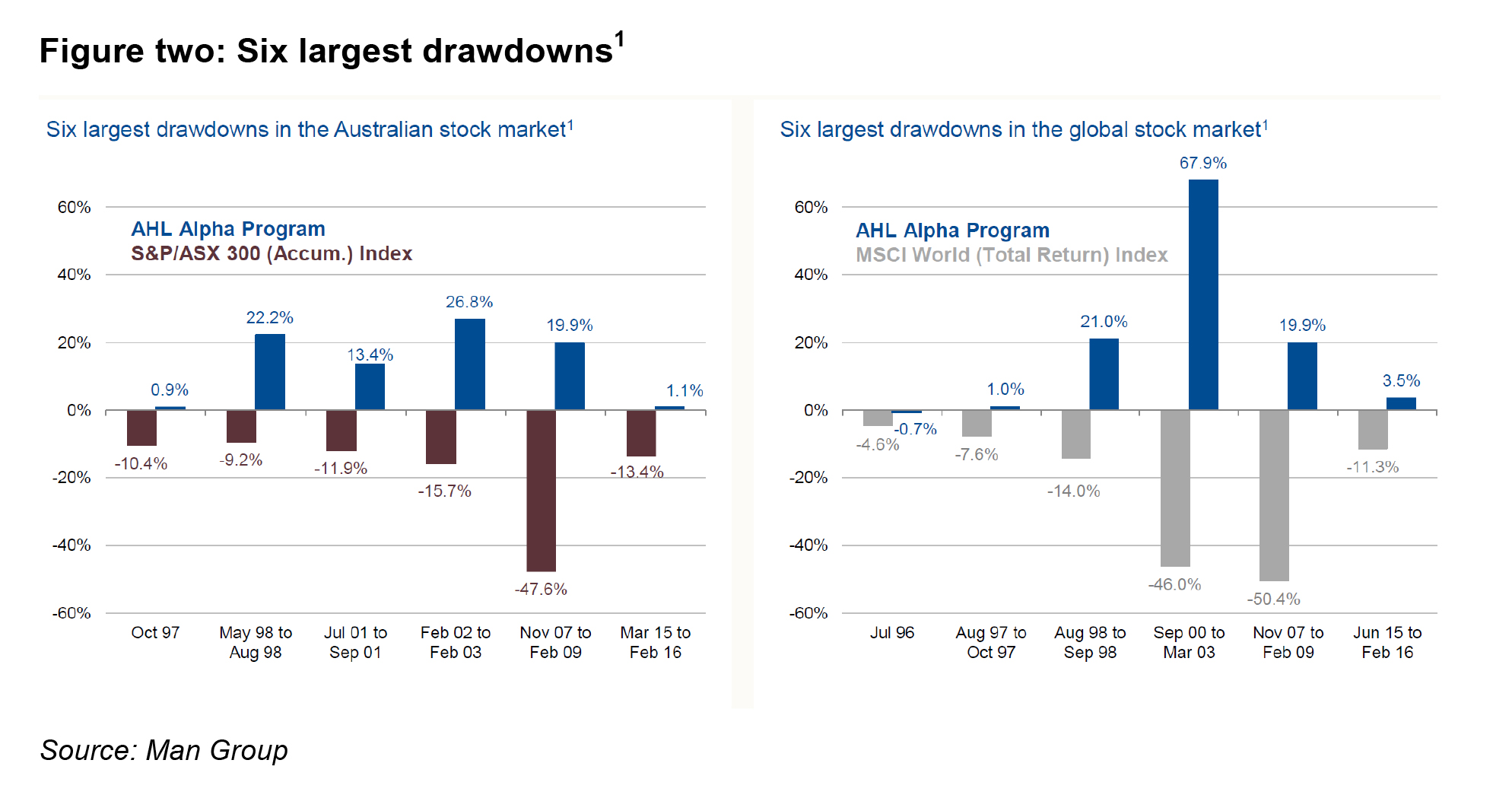

Managed futures can generate positive returns in almost all market conditions; they can profit from rising markets by taking long positions, or take advantage of the expectation of falling price trends by going short. As illustrated in figure two, using the Man AHL Alpha strategy as an example, the managed futures program has performed well during those periods when both Australian and global equities have experienced their worst drawdowns.

While managed futures have historically performed well in market conditions that have been unkind to traditional asset classes, as with any investment, past performance is not indicative of future returns.

5. Benefit from human behaviour and unforeseen events

Each year, US-based Dalbar undertakes a Quantitative Analysis of Investor Behaviour. Its 2017 study, as with previous reports, found that it is investor behaviour, rather than investment performance, that hurts investors the most. Among the report’s key findings were two important findings:

“For the 12 months ended 30 December 2016, the S&P 500 index returned 11.96%, while the average equity mutual fund investor earned only 7.26%, a gap of 4.70%.”[2]

This underperformance was primarily attributable to the “Trump rally” in November (1.13%) and December (1.34%). Investors who sold out on the expectation that markets would fall were hurt; managed futures funds following market trends, or momentum, are able to benefit.

“In 5 out of 12 months, investors guessed right about the market direction the following month. While “guessing right” 42% of the time in 2016, the average mutual fund investor was not able to keep pace with the market, based on the actual volume and timing of fund flows.”[3]

The research demonstrates that investors struggle to constrain their emotion and tend to buy and sell investments at the worst times. Trend following funds strip out the emotion, the greed and the fear.

While investors may be preoccupied with downside protection and risk aversion, the events of the GFC and the years that followed have shown that sentiment can shift abruptly and spawn sharp rebounds that many investors miss out on. Consequently, one of the most attractive attributes of managed futures funds is that they can capture strong trends in both rising and falling markets and may add value to your clients’ portfolios irrespective of the prevailing market conditions.

———–

[1] The periods selected are exceptional and the results do not reflect typical performance. The start and end dates of such events are subjective and different sources may suggest different date ranges, leading to different performance figures. The Australian stock market corrections and global stock market corrections are measured by the six largest drawdowns in the S&P/ASX 300 Accumulation Index and MSCI World Net Total Return Index hedged to USD, respectively, between October 1995 and June 2017. To illustrate Man’s longest running AHL Alpha Program, the past performance of AHL Alpha plc from October 1995 to September 2012, AHL Strategies PCC Limited: Class Y AHL Alpha USD Shares from September 2012 to August 2014 and AHL Alpha (Cayman) Limited from August 2014 to June 2017 are used in this chart and are measured as the rise or fall in price during the periods of drawdown set out in the charts above. All of these entities invest in the same way as the AHL Alpha Program. This chart is not a chart showing the performance of Man AHL Alpha (AUD). The periods selected are exceptional and these results do not reflect typical performance. As a consequence, they give no indication of likely performance. Performance figures are calculated net of all fees as at 30 June 2017. Past performance is not a reliable indicator of future performance.

[2] Dalbar Quantitative Analysis of Investor Behaviour, 2017

[3] Dalbar Quantitative Analysis of Investor Behaviour, 2017

———-