Australian brands close the gap between digital experience and customer expectation

SAP Australia yesterday launched its 2017 Australian Digital Experience Report, revealing that Australian businesses have significantly improved the digital experience they provide, closing the gap to what consumers expect. However, while performance has improved, consumers are still more likely to be unsatisfied with digital experiences than delighted by them.

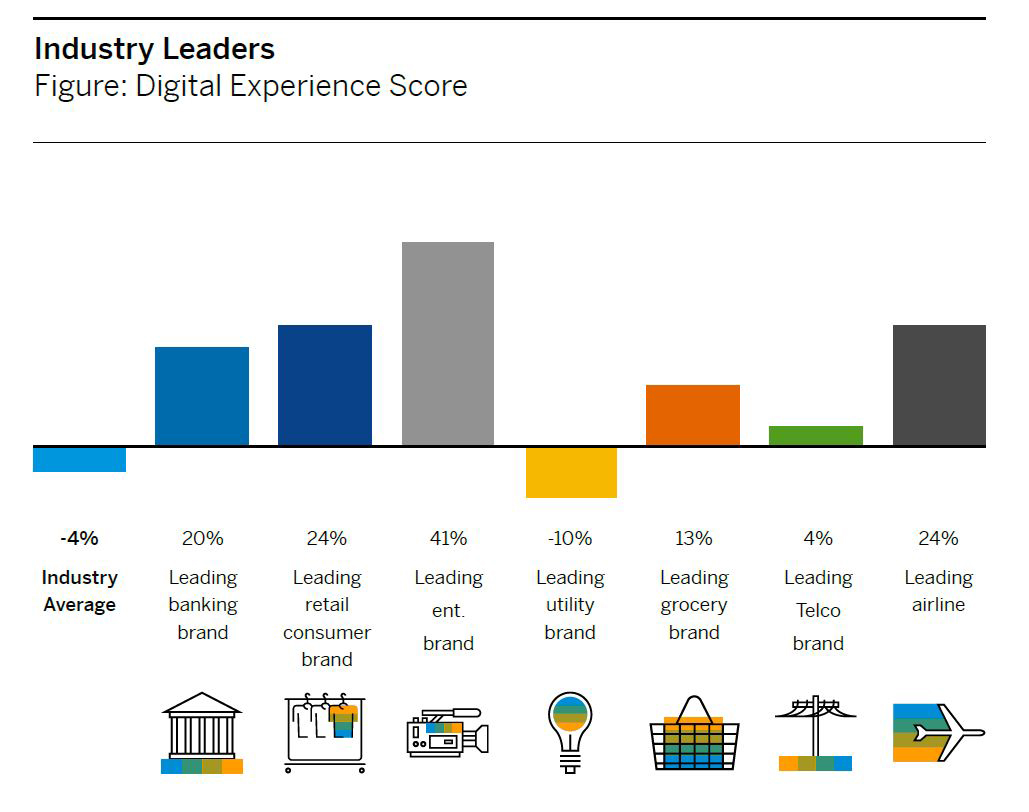

The report, based on results from more than 4,000 Australians who rated more than 11,000 interactions against 14 attributes, found overall digital experience has improved from last year. For the first time since the survey was conducted in 2015, five industries posted positive results. Retail grocery brands led the way, improving their combined digital experience score[1] from -4 to 10 over the past 12 months. Banking (7), media and entertainment (6) and retail consumer (4) also returned positive digital experience scores.

Air travel achieved an overall score of 1, which means it has an almost even split of delighted and unsatisfied customers. Insurance (-5), telecommunications (-11) and utilities (-15) all have more unsatisfied customers when it comes to digital experience.

Overall, the proportion of consumers unsatisfied with their digital experiences has dropped from 40 per cent to 35 per cent, while the number who are delighted has increased from 26 per cent to 31 per cent. This highlights that brands have actively improved the digital experiences they provide, but there’s still much room for improvement.

Australia’s Digital Experience Gap, 2017

Top performing brands and industries

For the second year running, Netflix was singled out by Australians as having the best digital experience among all brands. Other leaders include online retailer Kogan, Vodafone and Suncorp Bank.

“The digital performance of brands in Australia has significantly improved since we first launched the study in 2015. When we look at industry-specific scores, retailers are clearly equipping themselves with innovative digital capabilities to prepare themselves for future disruption, such as the impending local launch of Amazon. Banks also face intense competition and are looking to improve customer experience, increasing engagement and responsiveness as a result.” said Colin Brookes, President and Managing Director, SAP Australia and New Zealand.

“While brands have improved overall, this is still very much grounded on getting the basics right along with a greater focus on the emotional attributes that consumers demand. In order to become a digital experience leader, brands should look to new technologies such as artificial intelligence and machine learning to help integrate and deliver personalised experiences across channels, which delight customers.”

AUSDXR Brand leaders, 2017.

Meeting omni-channel expectations

New to this year’s research, the report highlights how brands can improve their digital experience scores by enabling customers to interact across multiple channels. Brands delivering an omni-channel[2] experience saw a lift in Net Promotor Score[3] (8 per cent versus -1 per cent) and customer loyalty (43 per cent would remain loyal versus 38 per cent), versus those that offer a single channel.

Close to half (43 per cent) of consumers use at least five channels to engage with brands. This includes physical stores, contact centres, mail, websites, live chat, social media and mobile apps. With more consumers now expecting omni-channel interactions, brands need to ensure integrated and cohesive consumer experiences or risk losing customers.

While 33 per cent of consumers are delighted with the digital experience in multi-channel environments, compared to 22 per cent in single-channel engagements, the number of unsatisfied consumers demonstrates the complexity brands face managing experiences across multiple channels. Omni-channel experiences disappointed 29 per cent of consumers compared to just 16 per cent in single channel.

Head of SAP Hybris Australia and New Zealand, Stuart O’Neill, said: “Consumers no longer view each brand interaction in isolation – they want a consistent experience at every touch-point. The best performing brands across industries are looking outside the box and ensuring each consumer interaction is optimised, personalised and, above all, delightful.

“A great example of brands looking critically at the experience they provide and making a change can be seen in the grocery sector, where these brands are under a lot of pressure from digital native competitors looking to take market share. This report is proof that the changes the industry has made over the last year are having a big impact on customer loyalty and NPS.”

Digital channels drive satisfaction

Consumers have grown to expect digital interaction. Websites (41 per cent) scored the highest satisfaction rating followed by email (33 per cent) and mobile apps (25 per cent). These provided a better customer experience than shopfront/in-store/branch (24 per cent), telephone/contact centres (20 per cent) or mail (19 per cent). Newer technologies such as social media (eight per cent) and live chat (five per cent) offered the lowest levels of satisfaction for digital channels.

Consumers in the 18-34 age group are more likely to use five or more channels to engage with brands (57 per cent) compared to those aged 35-49 (46 per cent) and 50+ (30 per cent). Similarly, younger consumers reported feeling more satisfied with their experience in social media and live chat channels compared to older consumers.

“We need to remember consumers are individuals with preferred methods of engagement. Providing an optimised experience across all channels ensures that, no matter where they choose to reach you, they have an experience that meets their expectations,” said O’Neill.

“This is increasingly important with the number of international brands launching in Australia, many of which are defined by robust omni-channel experiences.”

About the Survey

To better understand the digital experiences being delivered by Australia’s leading brands, and how these compare to consumer expectations, SAP commissioned AMR to poll more than 4,000 Australian consumers. This year’s survey covered eight industries: retail consumer, retail grocery, telecommunications/internet service providers, insurance, banking, utilities, media and entertainment and air travel.

Performance was based on consumers scoring each attribute on a scale of 0 (not important) to 10 (most important), with the most important attributes defined by a score of 9 or 10.

———