Shared co-working spaces: an alternative property opportunity to investors

From affordable housing to agriculture, student accommodation to co-working space, Australia is slowly following the lead of other markets and offering an increasing number of alternative property opportunities to investors. In this article, DomaCom explores the world of alternative property and examines a range of investment opportunities that lie in diversified property assets, assets that are usually off the radar for most.

The alternative property sector is thriving in overseas markets. According to JLL[1] , the United Kingdom (UK) has seen a surge in alternative property assets; it has jumped from just 10% of the property market in 2010, to become 29% of the market in 2016. The reason? Positive fundamental drivers, with many sectors having a significant supply and demand imbalance due to demographic and structural changes.

Demand for alternative property stems from the emergence and subsequent maturing of new property sub-classes, current high valuations in residential and commercial property, the uncertainty surrounding retail, and high valuations of both the equity and bond markets. Changing demographics and an evolution in the way we use our cities contributes to demand, along with changing lifestyle patterns, technology and increased global mobility.

Although focused on the UK, JLL’s Alternatives Predictions 2017 contains analysis arising from interviewing a range of institutional investors, private equity, property companies and developers, with combined assets under management of more than £207 billion. There were several interesting findings:

- Investor attitudes toward alternative property assets are overwhelmingly positive

- Over 70% of respondents either plan to increase their allocation by 2020 or are fully exposed to their respective alternative sectors

- The benefits of diversification and ability to access long term income from alternative property assets are well established.

The report also found that demand for alternative property outstrips supply, a result of factors including population growth, increasing life expectancy, changing demographic profiles, the greater use of digital appliances, and the impact of technology in the work place.

Likewise, alternative property assets have become mainstream in Europe; according to analysis from Savills[2], alternative sub-sectors represented 25% of total European real estate investment activity in 2015. In fact, allocations to alternative property assets have increased approximately 25% year on year, as investors look beyond traditional property assets for higher returns, stable income and assets that are less correlated with economic cycles.

Student housing

The student housing market in the UK is well established, experiencing sales of £3.2 billion in 2016, a result of the UK being the key European market for international students. Similarly, Australia is entrenched as a key destination for international students, primarily from south-east Asia.

International student growth is strong, with student visas growing by 11% from 2015 to 2016. China (28%), India (11%), Republic of Korea (4%), Thailand (4%) and Vietnam (4%) are the top five countries of origin for international students studying in Australia[3].

Unlike the UK however, Australia’s student housing market as an alternative property asset class is relatively undeveloped, with fewer transactions, fewer beds – and fewer investment opportunities. The Savills report suggests there is a reasonable pipeline of development in the student accommodation sector, particularly in Sydney and Melbourne where there is a significant supply and demand imbalance.

Currently, most development is in private or institutional hands; it remains to be seen whether Australia will follow the UK’s lead and translate development in the student accommodation sector into an accessible investment opportunity for retail investors.

According to Austrade’s Economic Analysis, Education is Australia’s third largest export industry after iron ore and coal.

Affordable housing

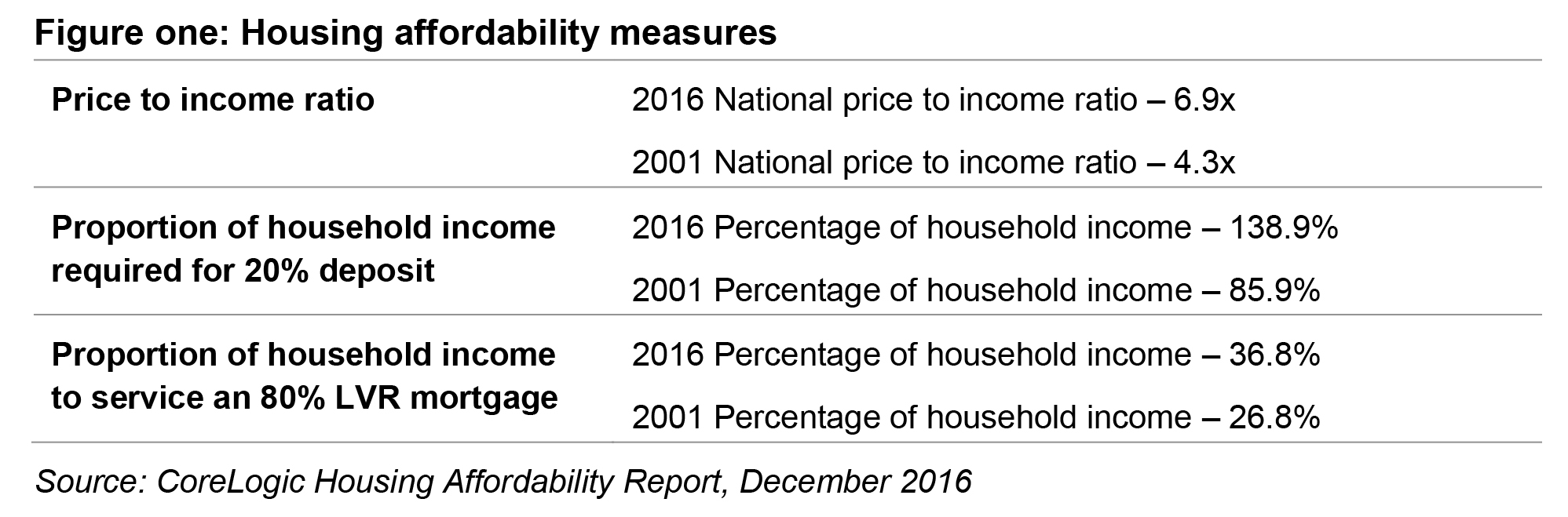

Australia’s housing affordability crisis is not new, but there seem to be few signs that it’s abating. This has real and potentially long-reaching implications many, particularly for those not currently in the property market.

The extent of the issue is illustrated by figure one, from CoreLogic’s 2016 report into housing affordability[4], which considered three measures of affordability and compared the current data to that collated 15 years earlier (data at September 2016 and 2001).

The significance of housing affordability – or lack of – is underscored by the measures introduced by the 2017 federal budget, in which retail and institutional investors have been incentivised to invest in the social housing sector.

Managed investment trusts (MITs) can now invest in affordable housing, and investors who purchase into these trusts will see an increase in the capital gains tax discount they receive (from 50% to 60%).

Affordable housing case study: Akuna Lifestyle Estates

There’s been a significant amount of negative press of late about aged care facilities – poor care and conditions, excessive costs to buy in, fees along the way, and high exit fees to get out. Despite this, many Australians still need cost effective solutions for retirement living.

DomaCom has signed an Agreement with Akuna Lifestyle Estates to launch the first crowdfunded resort-style residential community land development in regional Victoria.

The project is planned to be developed and sold in eight stages over three to four years, commencing in 2017, and will be follow a Residential Land Lease Community (RLLC) model; a more affordable and transparent option than the conventional retirement village model. Residents will purchase their homes for a modest price, and rent the land it sits on.

With this scheme, there are no exit fees, with any future house sale only subject to the normal residential sales commission fee of 2.5%; there are no refurbishment fees or other costs imposed on the residents. In fact, residents receive all proceeds from the sale of their house.

The target market comprises those aged over 55, with a focus on those retirees with low superannuation balances and who qualify for Government Rental Assistance on the land lease. This market is growing at 30 per cent per year, with a third of Australians estimated to be over 55 within a generation. Akuna will develop the land and then sell the homes with 49- year land leases at an average price of $265,000 per house.

DomaCom will use its fractional property investment platform to offer an attractive yield to investors for the acquisition and development of the land and common facilities, including a clubhouse, sports centre, pool and bowling green; it is targeting a 15% annualised return on the completed project with an estimated ongoing rental income of 8% pa.

Co-working spaces

Technology has driven changes in the way we work and, as a result, there’s been significant growth in flexible and collaborative workspaces. The incredible success of New York-based WeWork illustrates this growth potential; launched in 2010 to offer serviced office spaces to travelling entrepreneurs, WeWork is now worth over US$20 billion.

With a global presence, including Melbourne and Sydney, WeWork has tapped into a changing jobs market and the sharing economy. Individuals or small business don’t want the overheads of an office, but want a space where they can work without having to worry about a printer that’s out of toner, a blown fuse or sales calls.

Many co-working spaces offer a mix of private and communal work areas, often a café and importantly, exposure to like-minded entrepreneurs to share ideas, network and potentially generate business.

As with the student accommodation sector, it’s a burgeoning sector with significant growth potential. A CBRE report published in January 2016 said that co-working spaces in the US are estimated to be experiencing a five-year compound average annual growth rate of 21 percent.

A recent report by The University of Sydney[5] found that:

- approximately 75% of co-working spaces in Australia are owned and run as private businesses

- 21% are run as ancillary to an operator’s regular small-business activities

- 8% are not-for-profit co-working spaces, usually established to pursue social causes

- 6% are funded by state or local government, generally to support economic development in a specific region.

Despite the potential, co-working spaces are yet to be harnessed as an accessible investment opportunity for retail investors.

Agricultural investment

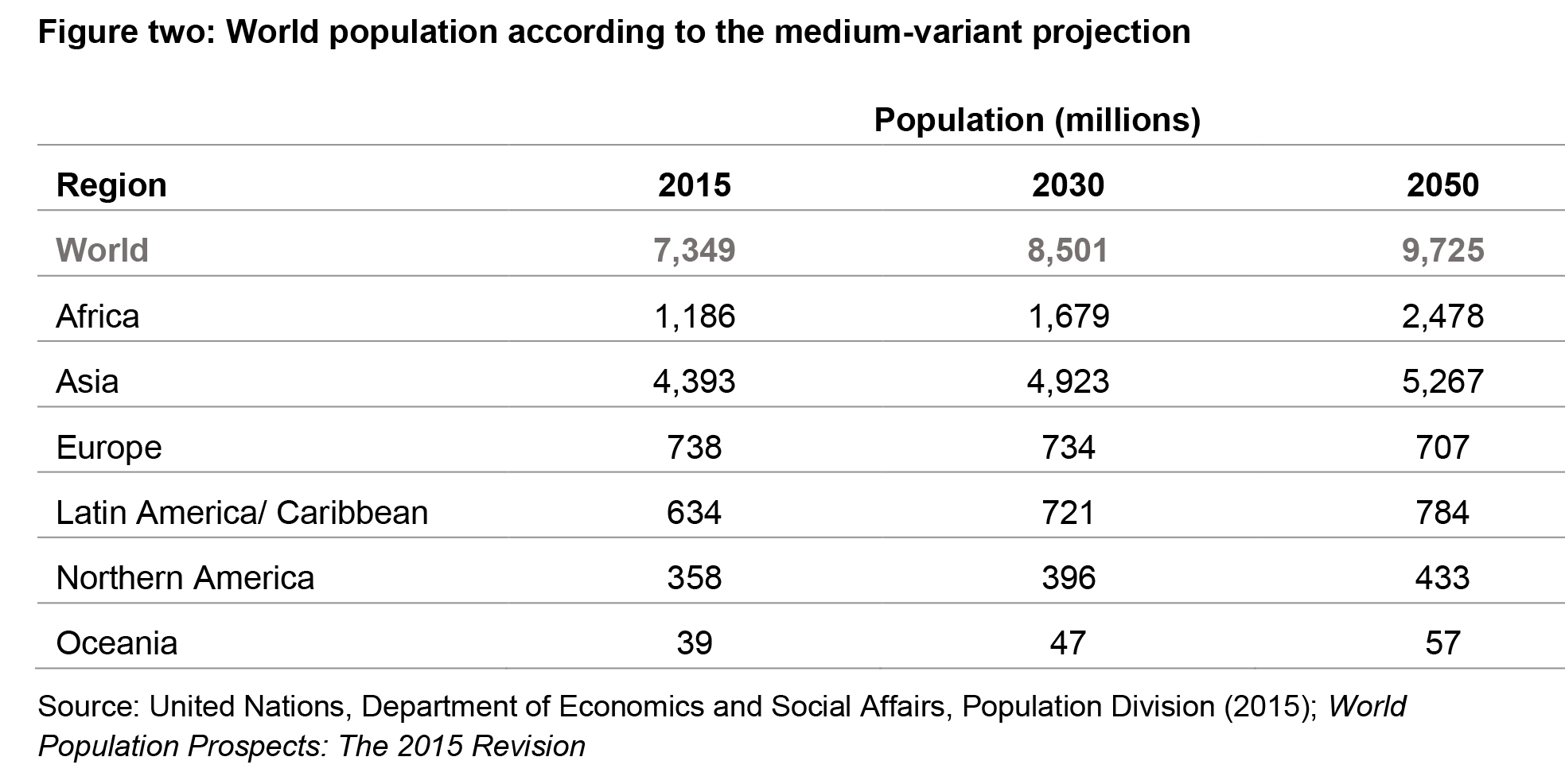

As the world’s population continues to grow, so too does the demand for agricultural production. As illustrated in figure two, it’s estimated that the world’s population will increase by 2,376 million by 2050, from 2015 figures. Asia and Africa will account for most of that growth. These regions are experiencing significant urbanisation and economic growth, which in turn fuels a growing middle class.

Food demand worldwide is likely to surge in the years ahead. Australia’s perception as a clean and green source of food has seen increased demand for dairy, meat, fish and grains. There is a solid investment case for rural property. Research by the Rural Bank of Australia[6] found that in all states, the median price of agricultural land has trended higher; the national median farmland price increased by 9.3% in 2016, following a 5.3% increase in 2015 and a 6.8% increase in 2014.

Agricultural case study: Cultivate Farms

Launched in April 2017, Cultivate Farms connects aspiring farmers with retiring farmers, a connection that provides a transitional succession process for retiring farmers. This model benefits farmers because when they partner with Cultivate Farms, the farmer retains partial ownership of their property and has the opportunity to mentor the incoming family. Its sold as an opportunity to rejuvenate communities that have been impacted by the proliferation of corporate or overseas farm ownership.

Because the farmer remains a partial investor, they still receive income and can have as much, or as little, involvement in the day-to-day running of the farm as they want. Aspiring farmers have often been locked out of opportunities because of high funding barriers. With Cultivated Farms, young would-be farmers are matched with opportunities that suit their needs; each is an equity owner (with as little as 1%), and receive a wage and annual incentives. They also have the ongoing support of farming experts and access to relevant education.

Equity is available to investors, with the opportunity to be involved with the farm if wanted. The model requires investors to take an equity stake of up to 20 per cent in the farm for a minimum of five years, during which time the farmers are paid a wage to operate the farm.

The DomaCom model

For investors who want the benefits of diversifying into rural property but have no interest in the farm, DomaCom can use its fractional investment platform to acquire farming properties in which investors and farmers can take a position by buying units in the sub-funds linked to the specific properties they are interested in.

Fractional investment provides a sound funding model for a range of alternative property investments. As a defensive investment, uncorrelated with traditional markets and the economic cycle, Australia is likely to follow the lead of the UK, Europe and US to offer an increasing number of alternative property assets becoming available for investment. DomaCom will assess the opportunities as they become available to make alternative property assets accessible to your clients.

——–

[1] JLL, Alternatives Predictions 2017 – UK

[2] http://www.savills.com.au/_news/article/109975/200105-1/3/2016/investment-in-alternative-real-estate-assetsbecomes-the-norm-in-europe

[3] Savills Australian Student Accommodation Market Report

[4] CoreLogic, Housing Affordability Report, December 2016

[5] The Australian Co-Working Industry, The University of Sydney

[6] Australian Farmland Values Report 2016 – Rural Bank of Australia

———