Multi-asset investing involves blending the active management of directional risk across a range of asset classes…

One approach towards multi-asset investing involves blending the active management of directional risk across a range of asset classes with less directional sources of return.

Introduction

When looking at a distribution of returns from global equity markets over a full market cycle, the majority of returns in each period have been largely favourable.

However, most long-term investors understand that part of equity investing also includes dealing with volatility and less favourable returns, which can be driven by anything from macroeconomic factors to financial shocks and political events. While less frequent, it is these negative returns which cause discomfort to investors, especially the extreme ‘left-hand tail’ events (Chart 1).

Extreme negative return events can lead to severe drawdowns in an investor’s portfolio, which can change the retirement plans of investors by delaying their planned date of retirement or reducing the amount of capital to cover expected living expenses. For example, in the calendar year of 2008, following the equity market collapse resulting from the global financial crisis, private pension fund investments lost 23% of their real value on aggregate in the OECD countries. This is equivalent to $5.4trn, which means many people lost a substantial amount of their retirement savings. In Australia alone during that year, losses amounted to 27%[2].

The significant impact is not only felt in investors’ portfolios, but it can also impact investors’ saving and investing behaviours in the short to medium term. For example, investors may sell at an inopportune time following such events, reducing the long-term return potential from their portfolios and in turn putting at risk their longer term financial objectives. Additionally, when investors suffer large financial losses, they tend to become more risk averse and save more, rather than invest. These factors can create a number of challenges for advisers when developing and implementing a long-term financial plan for clients.

Given the effect of the ‘left-hand tail’, we share our dynamic approach to mitigating this risk within a multi-asset investment strategy. In doing so, we acknowledge two important factors.

Firstly, there are no guaranteed strategies to completely remove ‘left-hand tail’ risk. Instead, we are simply seeking to reduce the probability of it occurring and the extent of any drawdown at the total-portfolio level. Secondly, there is no single method to address this issue – it requires a multi-layered approach.

Multiple dimensions of risk

When we think about building an investment portfolio we sometimes think in terms of likely sources of return and about how we manage the risks around them. Potential sources of return can be split into broad categories. For example, they could vary between the following categories:

- Fixed income: alpha and beta

- Equity: mainly beta

- Real assets: alpha and beta

- Total return strategies: mainly alpha

Over the long term, we might expect around half of a portfolio’s returns might be derived from asset allocation and the remainder from investment selection, although these proportions could vary over time. When conditions are conducive for beta to perform, one might expect a strategy to run more directional risk and beta would be likely to contribute more than half of portfolio returns. Conversely, when conditions are more challenging (and beta is less attractive), there may be more opportunities for the portfolio to generate returns from alpha.

Managing investment risk across such a portfolio requires thinking in multiple dimensions:

- At a portfolio level to ensure appropriate levels of diversification.

- At an asset class level, specifically, being mindful of drawdown risk when running directional exposure.

- At an individual position or strategy level to ensure that risk is not overly concentrated and that downside in the event of extreme moves is within tolerance levels.

When managing directional risk, some form of downside protection is sensible for assets with material downside potential. When it comes to managing individual positions and strategies, less directional sources of return can help deliver a better distribution of returns.

Managing directional risk

The most volatile elements within a multi-asset portfolio dominate the portfolio’s risk/return characteristics. It is reasonable to anticipate that asset class exposures will be an important

contributor to aggregate portfolio risk, and the most volatile assets (equities and commodities) are likely to be at the top of that list.

Biases towards these asset classes can be driven by a fundamental understanding of how they are influenced by macroeconomic factors, such as monetary policy, fiscal policy, growth and inflation. Looking at a range of valuation indicators in the context of an assessment of the macroeconomic environment, alongside proprietary indicators of market positioning, is one way of forming a view on their likely performance. But how much exposure is finally incorporated into a portfolio should also be guided by risk considerations.

A specific asset class approach could be deployed to limit downside. This can be illustrated with regard to equity exposure in chart 1. As Chart 1 shows that, equity returns can be attractive – but the ‘left-hand tail’ (the risk of an extreme negative outcome) is large. The same is true of a number of other risk assets.

Improving the distribution of those returns, reducing the ‘fat tail’ at the left is obviously attractive.

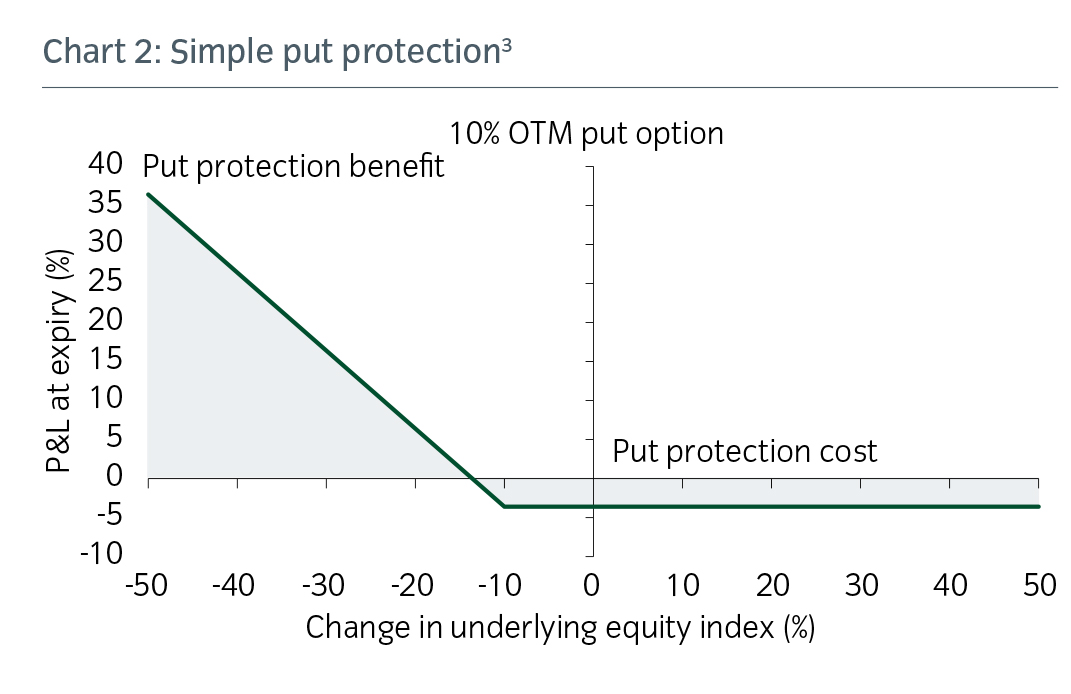

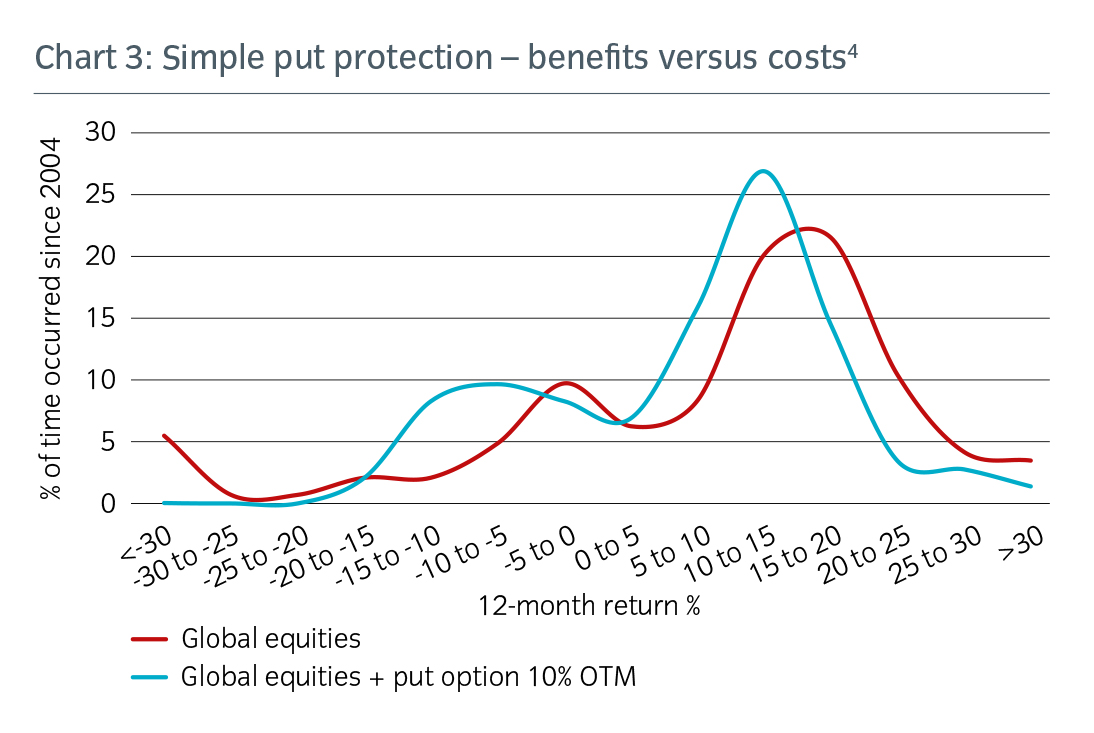

There are many ways of potentially providing downside protection. One simple approach, shown in Chart 2, is to use a put protection strategy that seeks to limit downside beyond a pre-determined level. Chart 3 illustrates the impact of employing this strategy. It is effective, but comes with a cost in terms of return generation.

More dynamic approaches to downside protection can improve meaningfully on simple put protection. One example is synthetic option replication, a variant discussed here that helps to increase the probability of a portfolio achieving an outcome and reduces the probability of significant drawdowns, even in deep bear markets. The principles which guide the process are:

- Scale initial investment in individual positions in accordance with conviction and tolerance for downside performance (by reference to historic and expected volatility).

- Dynamically manage the position size in accordance with changes in conviction and the performance of the investment. If the investment loses money, then the dynamic asset allocation framework will guide towards reducing the exposure, which seeks to contain the risk of further downside. If the position makes money, the portfolio manager has scope to increase the position size because it has moved further away from the tolerated loss level set when the position was initiated. (This approach should also incorporate some anti-momentum elements.)

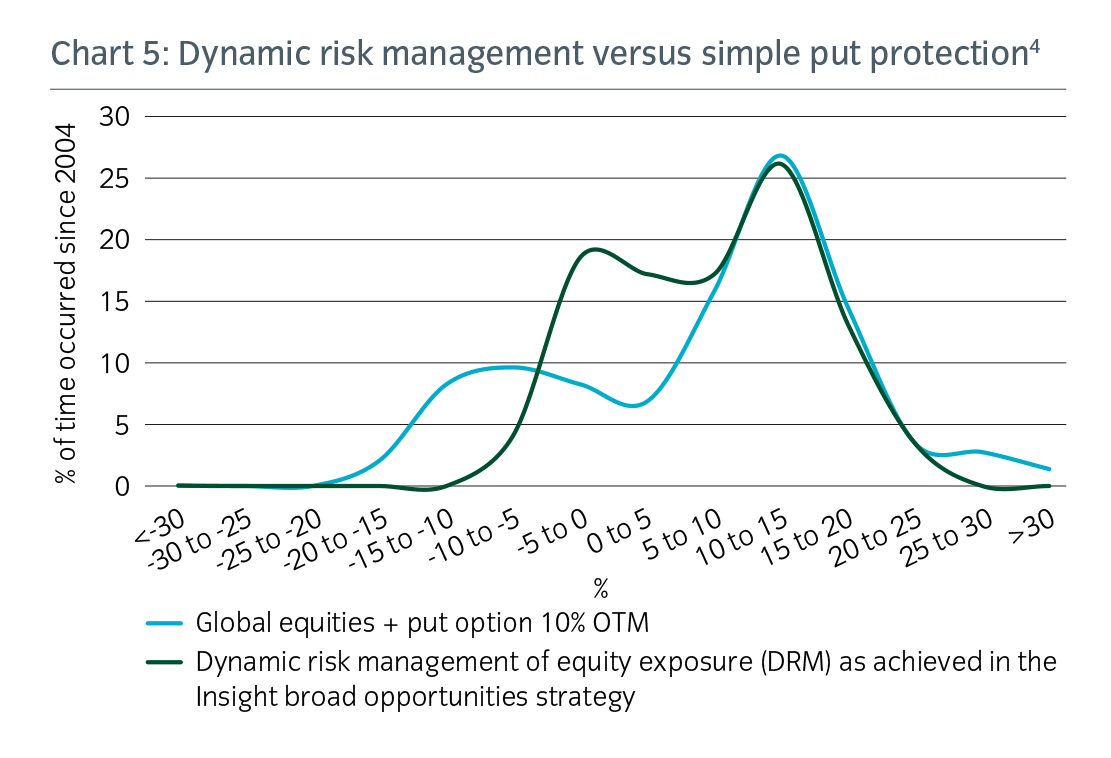

The charts below show how this dynamic approach can improve on the more simplistic option-based strategy. Chart 4 illustrates the principle behind this approach to dynamic risk management. Chart 5 shows that the resulting distribution, as generated in Insight’s broad opportunities strategy, has historically offered better downside protection and greater upside participation than the simple put protection strategy described earlier.

Managing individual positions and strategies

This dynamic approach to risk management can work for some investible assets, but not all. There are asset classes without a ‘fat left-hand tail’ or ones which exhibit mean-reverting characteristics. Alternative approaches to risk management are more appropriate for assets that fall within these categories and also for strategies that are designed to generate returns through alpha and have a limited requirement for beta management.

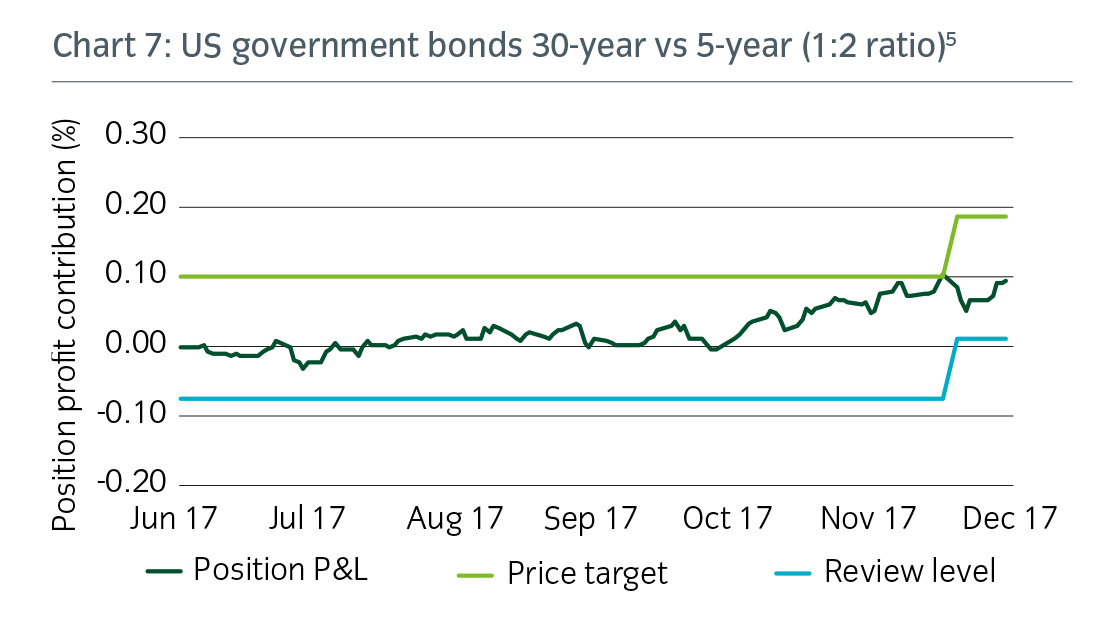

One example is ‘relative value’ positions that aim to capture the difference between two similar assets, where a long position is held in the investment believed to offer a better relative return and an offsetting short position in the one which is expected to underperform. The volatility (historic and expected) of the relative position must be taken into consideration when identifying the potential profit target, as well as the acceptable tolerance for loss.

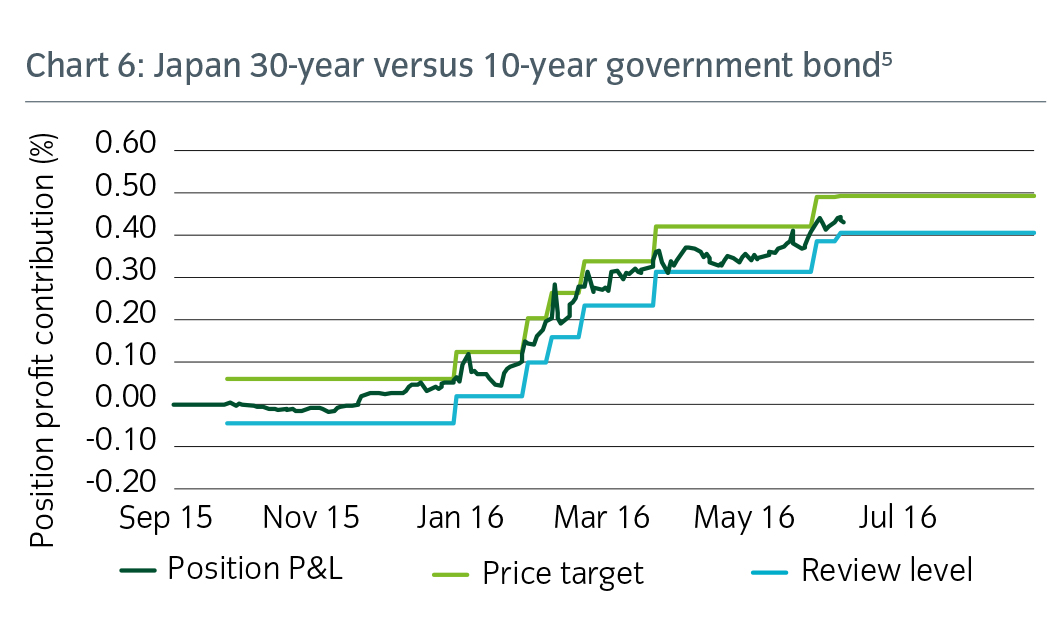

This approach ensures the monitoring of position performance against pre-determined expectations. The simplicity and rigor of this approach applies once a profit target has been reached – if the fundamental rationale remains valid, one could continue running positions while also ‘locking in’ profits and re-setting higher stop-review levels to account for this, as can be seen in Charts 6 and 7 below.

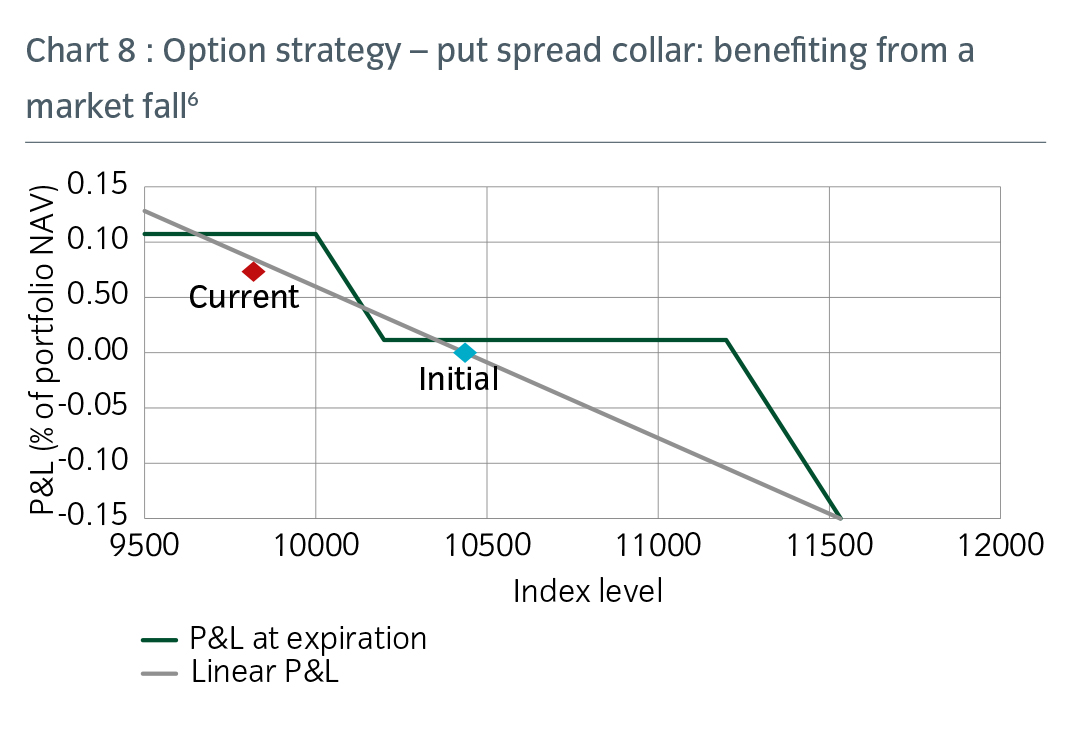

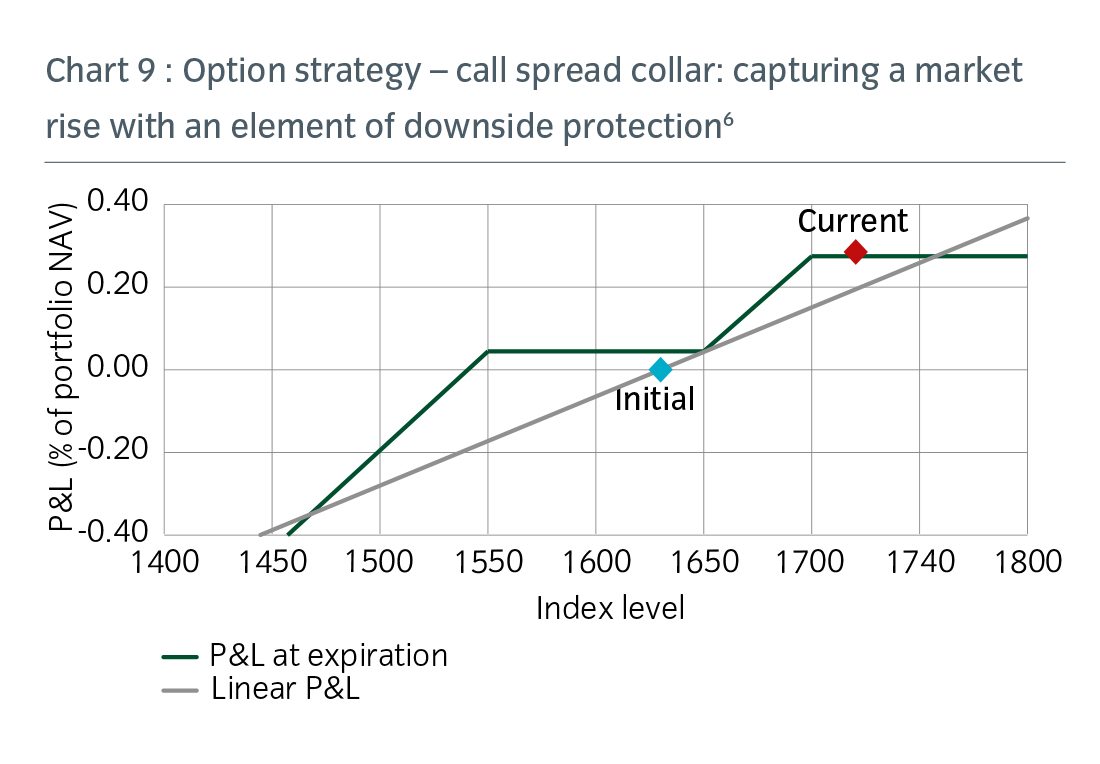

Other strategies require alternative approaches to risk management, for example, derivative strategies where economic exposures can move in a non-linear fashion.

By combining put and call options, one can be precise about the trading ranges viewed as likely across a variety of asset classes (see, for example, Charts 8 and 9). Different strategies can also isolate the particular characteristics viewed as desirable: directional views, volatility, carry, time value decay and skew can all be expressed using combinations of strikes and expiries.

When structuring an options trade, the position can be sized for a profit target, while also setting a stop-review level that reflects an acceptable level of downside risk.

Managing overall portfolio risk

Multi-asset portfolios aim to deliver returns by investing across a range of asset classes and strategies. This enables them to generate returns in different market conditions. Some investments work best (or, indeed, worst) in different environments; a strategy that has a broad mandate and the flexibility to take advantage of such opportunities can enhance its return potential.

A multi-asset opportunity set can also be used to diversify risk. When managing a multi-asset portfolio, it is crucial to understand the risks that are embedded within that portfolio and to ensure that it is sufficiently diversified. This sometimes involves thinking beyond historic statistical relationships: inter-relationships and correlations can change over time.

It is important to have not only an accurate picture of overall portfolio risk (measured by volatility, value-at-risk (VaR) and other appropriate risk metrics), but also to appreciate the decomposition of risk among portfolio positions. If risk were inappropriately skewed, portfolio adjustments would need to be made to secure more balanced risk distribution. This could then ensure that the portfolio had sufficient diversification from a fundamental perspective.

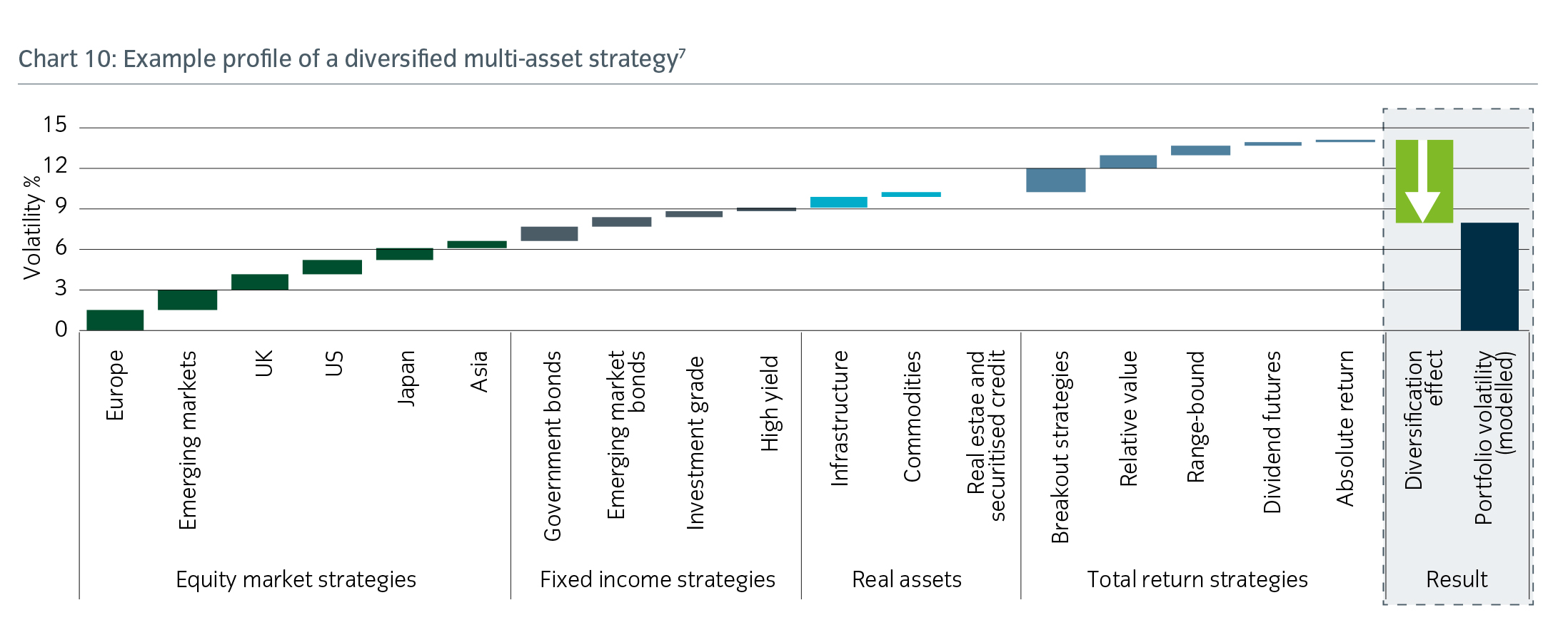

In Chart 10, the benefits of diversification are illustrated by showing the contribution to risk of the various strategies deployed within a diversified multi-asset portfolio and then comparing the aggregation of these individual positions with the expected volatility of the overall portfolio. The difference between the two gives a sense of the benefits that can be derived from a diversified multi-asset approach to return generation.

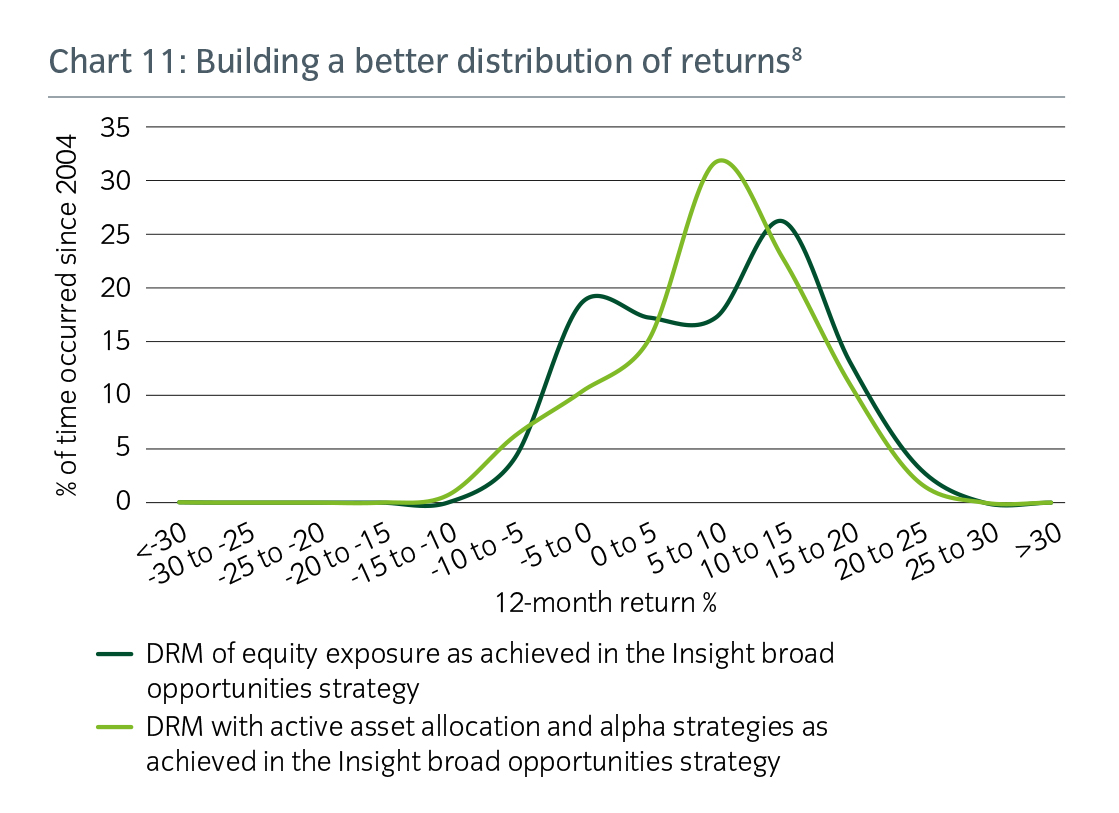

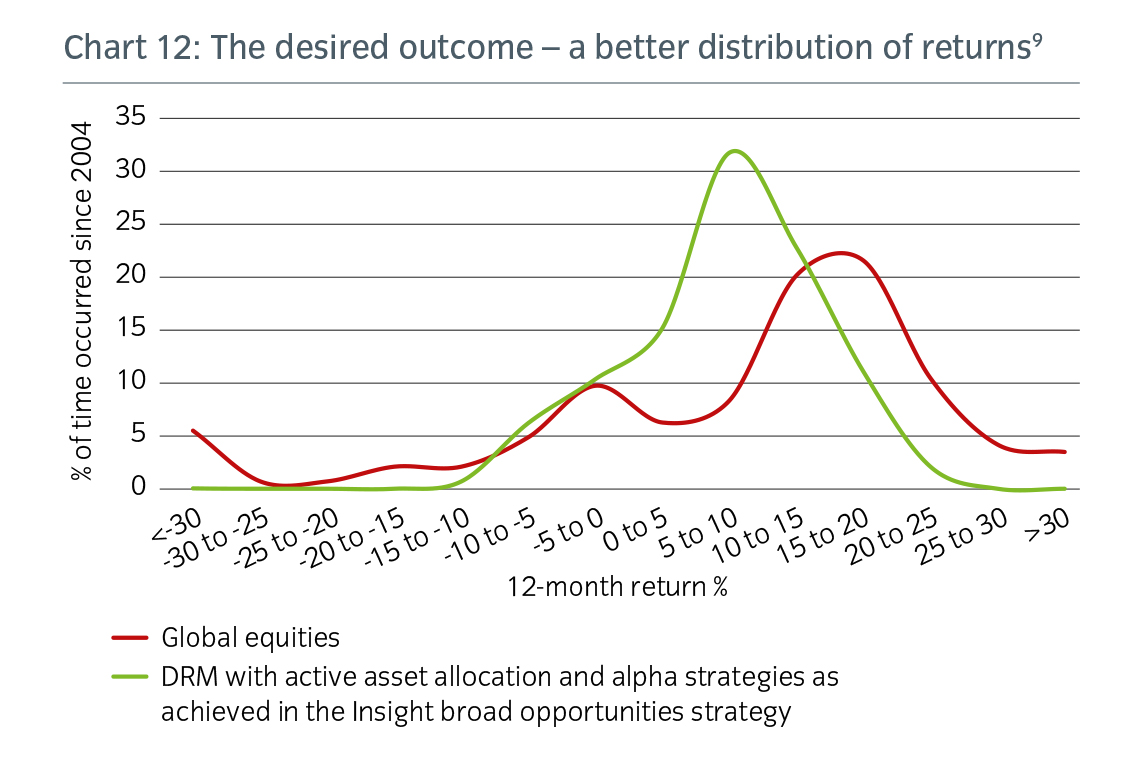

This kind of multi-faceted approach to risk management provides confidence that a broad opportunity set can be used to further improve the distribution of portfolio returns. Chart 11 shows the return profile of a 100% equity portfolio adjusted to incorporate the dynamic risk management strategy described above. The distribution achieved by an actively managed multi-asset portfolio is then overlaid on this return profile. Chart 12 illustrates the same distribution, but compared with global equities. It shows precisely how combining a wider opportunity set (including less directional strategies), with an active asset allocation overlay can improve on the distribution of returns.

Conclusion

While market swings are an expected part of long-term equity investing, it is the ‘left-hand tail’ risk that concerns investors. Since this risk is so difficult to predict and is large in size, it can have a devastating impact on portfolio returns and hinder investors’ ability to achieve their financial objectives for retirement.

At Insight, we take a dynamic approach to manage this risk within a long-term, multi-asset investment strategy, while at the same time aiming to deliver a growth strategy to increase investors’ real returns. We acknowledge that there are no guaranteed strategies to completely remove ‘left-hand tail’ risk, but rather to seek to mitigate the probability of it occurring and its impact when it does. We also acknowledge that there is no single method to address this issue – it requires a multi-layered approach and the expertise of a team of investment specialists, ready to respond to evolving market conditions.

———-