What is driving the exuberant confidence in China?

Tracey Chen

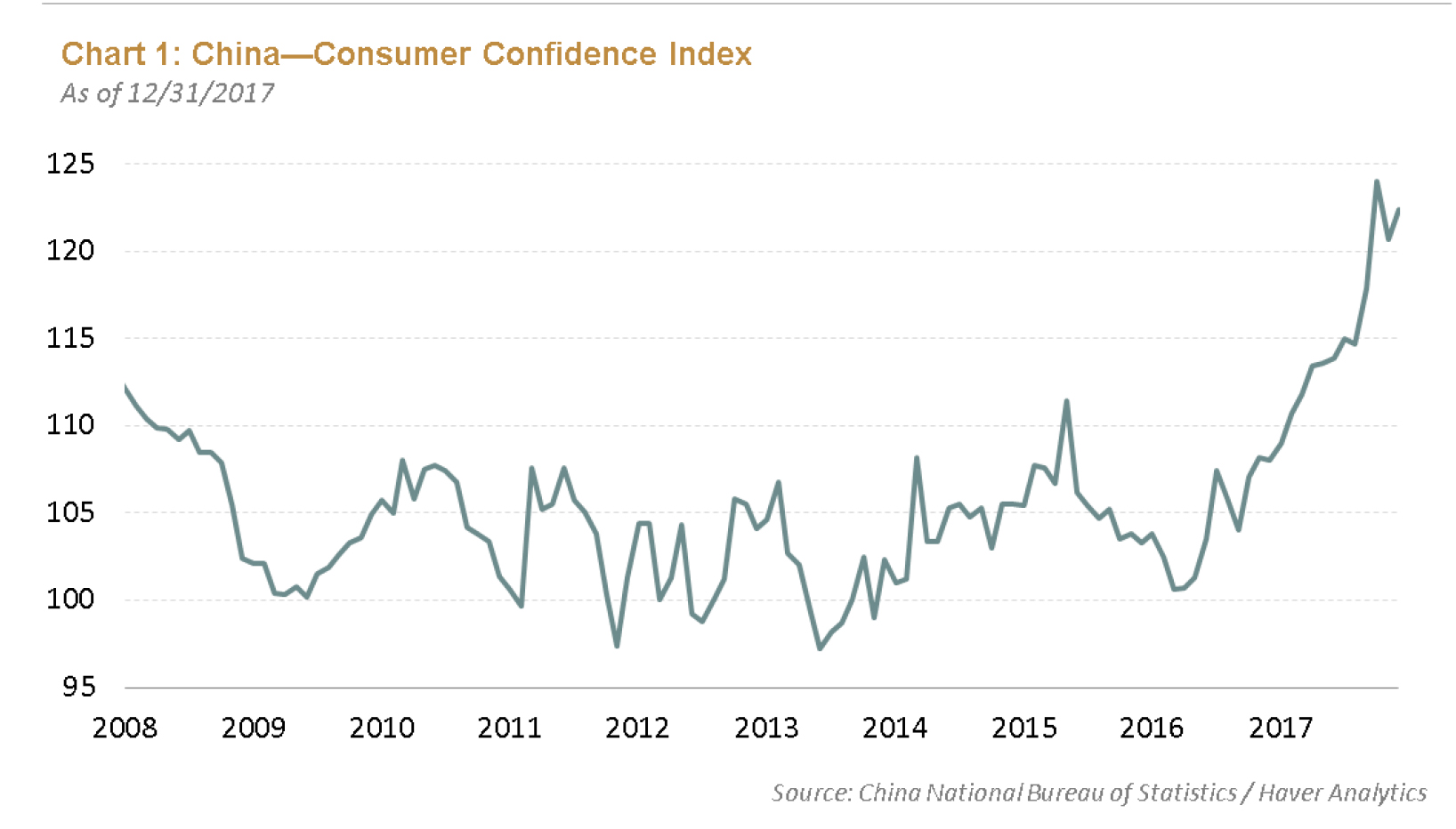

Tracy Chen, Portfolio Manager and Head of Structured Credit, at Brandywine Global, an affiliate manager of Legg Mason notes that Chinese consumers are suddenly feeling quite positive about the economy and their prospects according to recent confidence data (see Chart 1).

Ms Chen reports: This surge in optimism is particularly evident among the wealthy. A recent survey conducted by Hurun Report of individuals with net worth more than 10 million yuan (USD 1.57 million) found that roughly 94% of respondents are optimistic about the Chinese economy’s prospects in the next two years, up 3% over last year. Nearly half of this group expressed strong optimism on the Chinese economy, compared with just 28% in 2017—a jump that represents the biggest uptick in sentiment in 14 years. The bullish consumer confidence data can be attributed largely to several factors: the wealth effect of the property boom cycle in 2016 and 2017, a reduction in pollution due to environmental cleanup efforts, the robust gross domestic product (GDP) rebalancing stemming from President Xi Jinping’s national rejuvenation dream, and the emergence of a new economy.

1. The Wealth Effect of the Property Boom

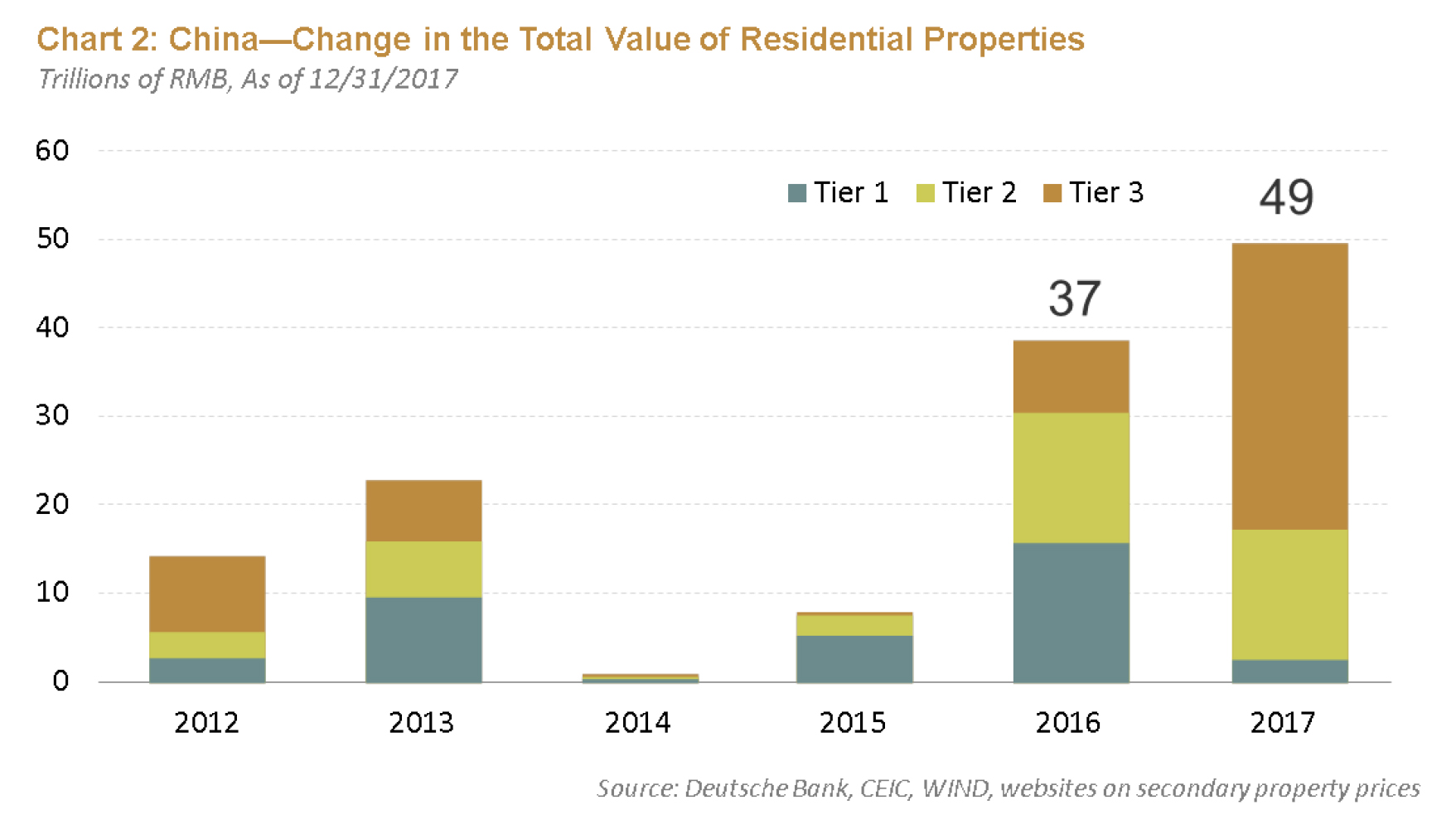

The importance of the property market in China cannot be overstated. The Hurun Report survey confirmed that real estate remains the preferred investment among the rich in China. However, the Chinese property market’s prominence is a double-edged sword. While inflating consumer wealth, it also makes the Chinese economy extremely vulnerable to a property market downturn. The old administrative measures to cool down the property market have not been very effective. Policymakers have started using long-term mechanisms to stabilize the property market, calling for property taxes and housing provisions across multiple sources and channels, including commodity housing, affordable housing, and rental options.

The massive wealth effect from the property boom in 2016 and 2017 is unique. The majority of wealth gains in 2017 were in Tier 3 cities as opposed to the dominance of Tier 1 and Tier 2 cities in the past. As a large economy with uneven regional development, China typically sees changes occur in two or three waves, led by the rich coastal area before spreading to less-developed inner regions. In 2017, the total value of residential properties jumped to RMB 49 trillion (see Chart 2) with a significant wealth effect from property boom gains seen in Tier 2 and Tier 3 cities. Since Tier 2 and Tier 3 cities make up the majority of China’s population and GDP, the impact of the spread of disposable income growth due to property gains from Tier 1 to Tiers 2 and 3 is significant. This wealth effect has spurred a boom in household consumption which helps purchases of luxury goods and Chinese imports. As a result, China’s current account surplus should continue to shrink.

2. The Improving Environment

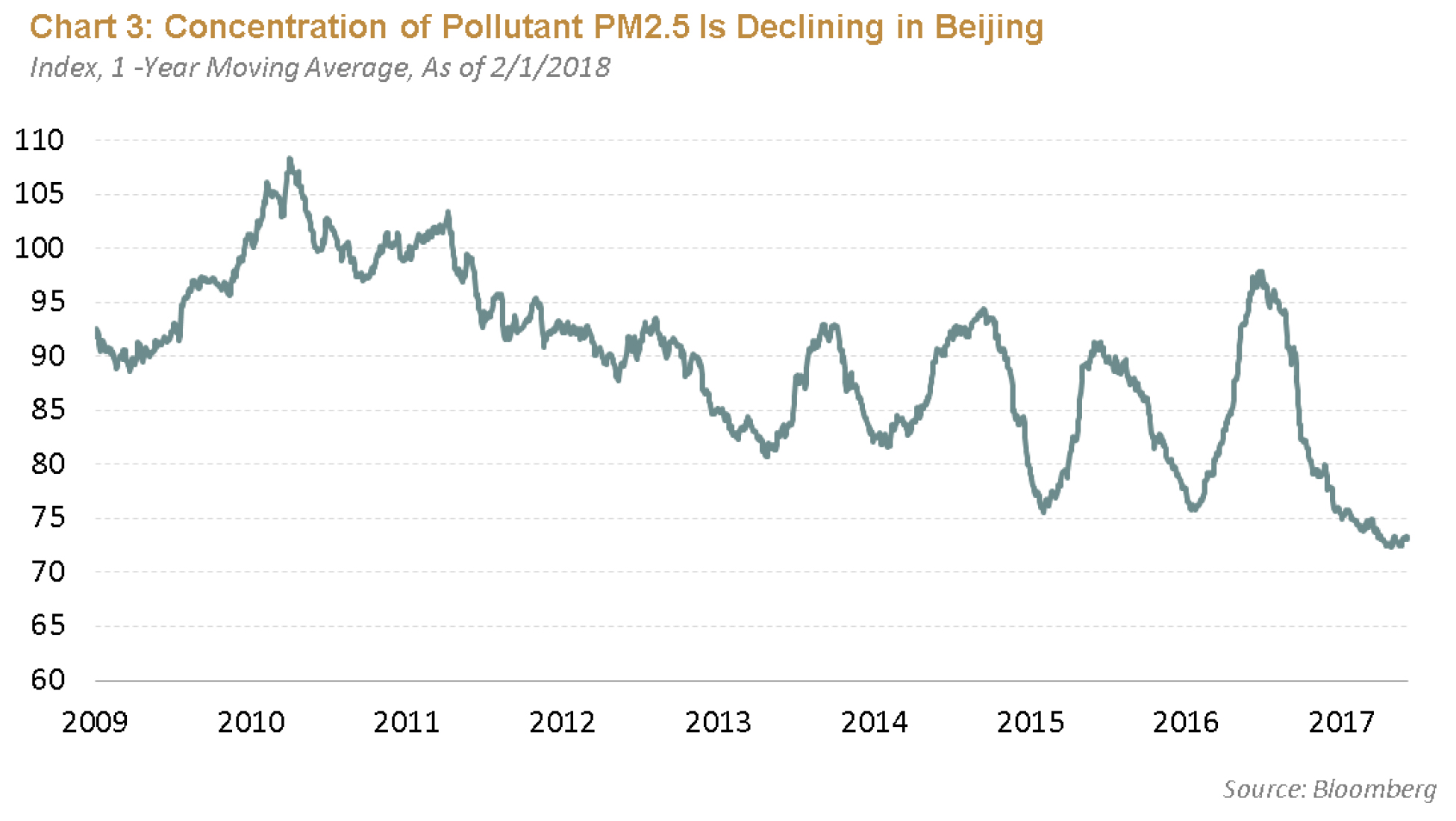

Due to the government’s anti-pollution campaign for the past several years, which has included a variety of measures such as converting coal heat to gas, pollution in Beijing and in 27 other cities in northeastern China has fallen sharply. The harmful pollutant indicator PM2.5 that measures air quality in terms of particulate matter dropped precipitously in Beijing (see Chart 3). Greenpeace estimated that lower pollution levels resulted in 160,000 fewer premature deaths across China in 2017.

3. The Great Rebalancing

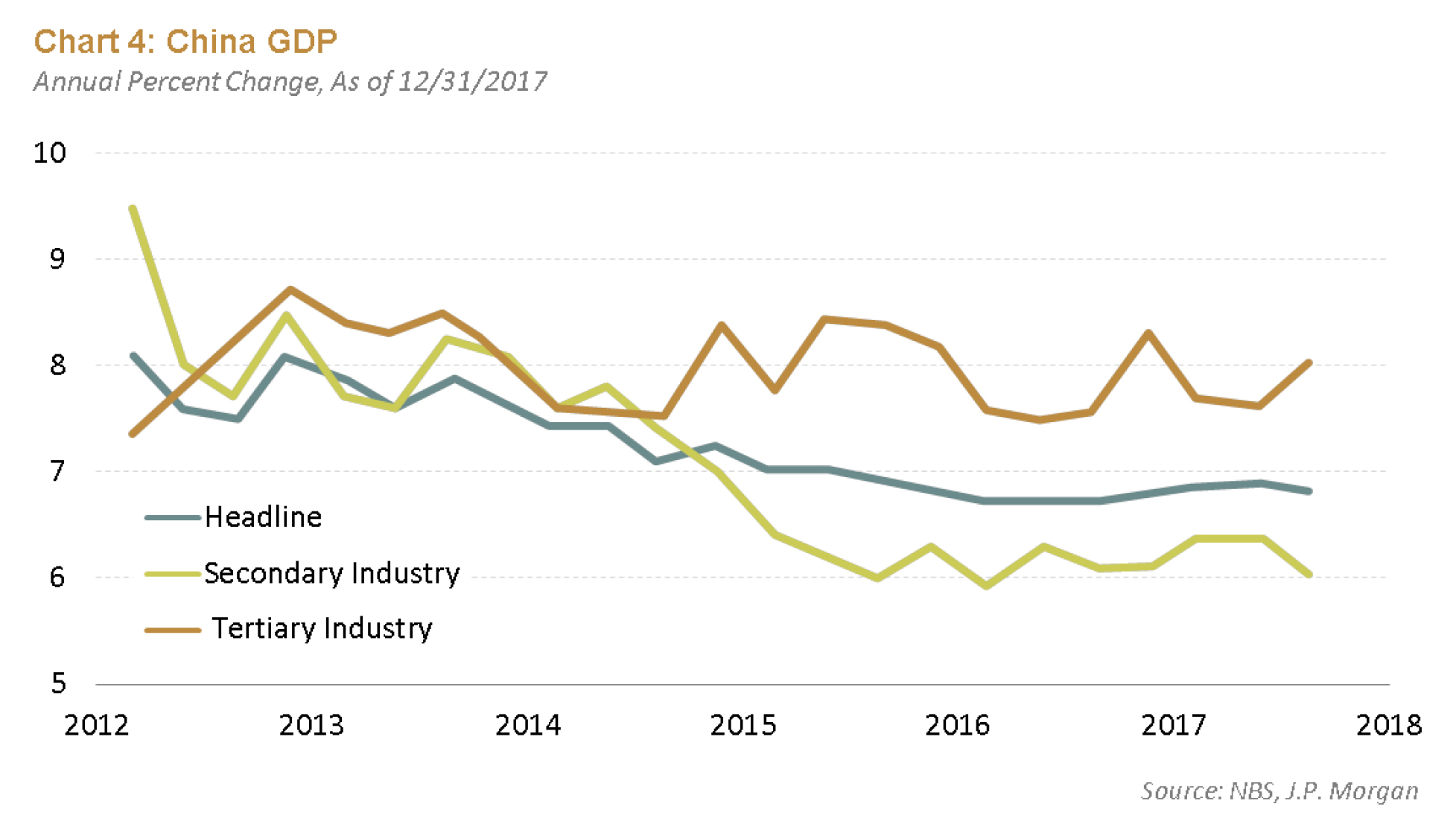

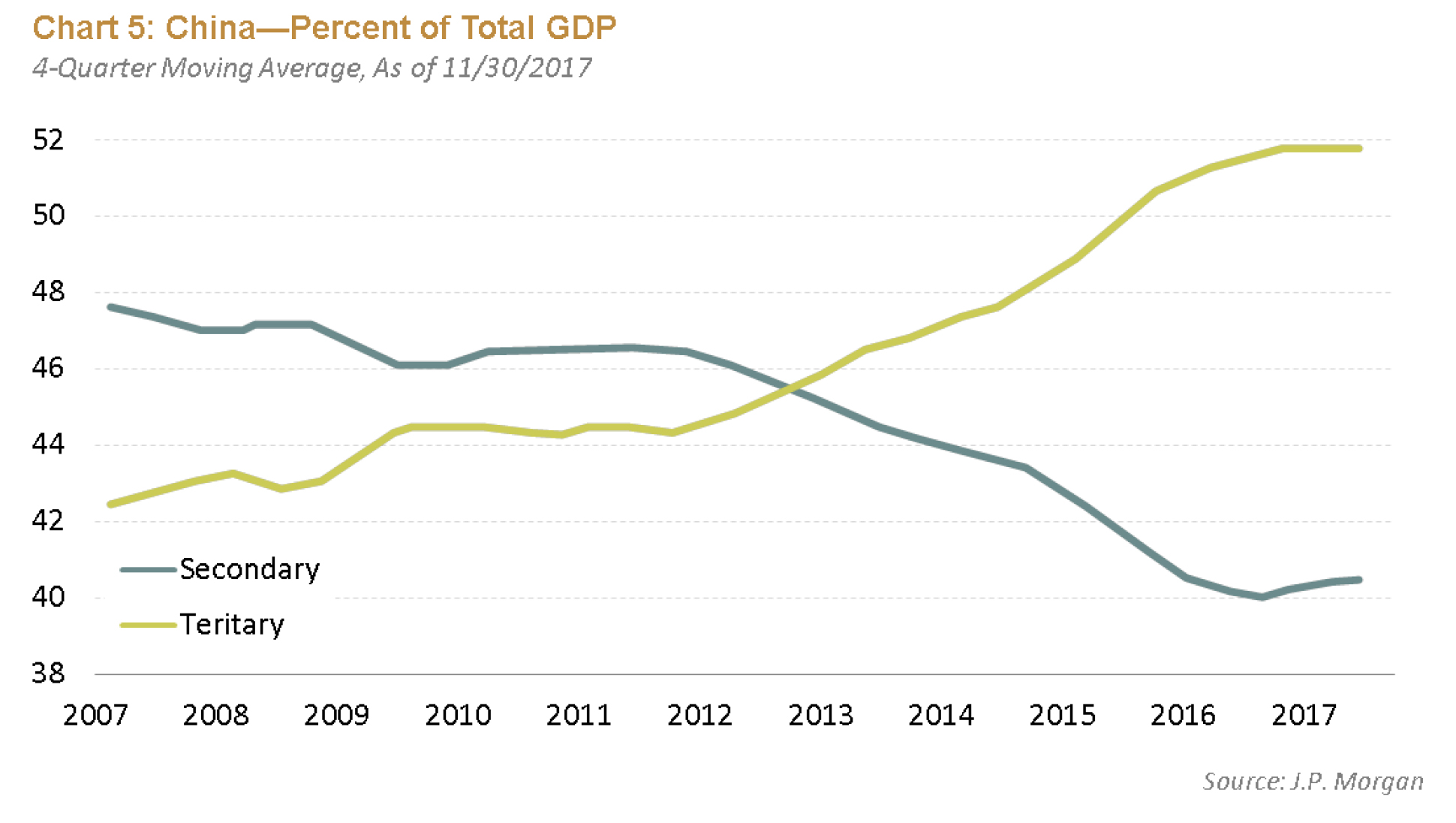

While investors mostly focus on China’s debt and overcapacity issues, the rebalancing of GDP is quietly happening at “China speed.” The expansion of tertiary, or service, industry has been impressive at 8% nominal growth, a much faster rate than secondary industry (see Chart 4). As a percent of GDP, tertiary industry already dominates with a 52% share (see Chart 5).

4. The New Economy

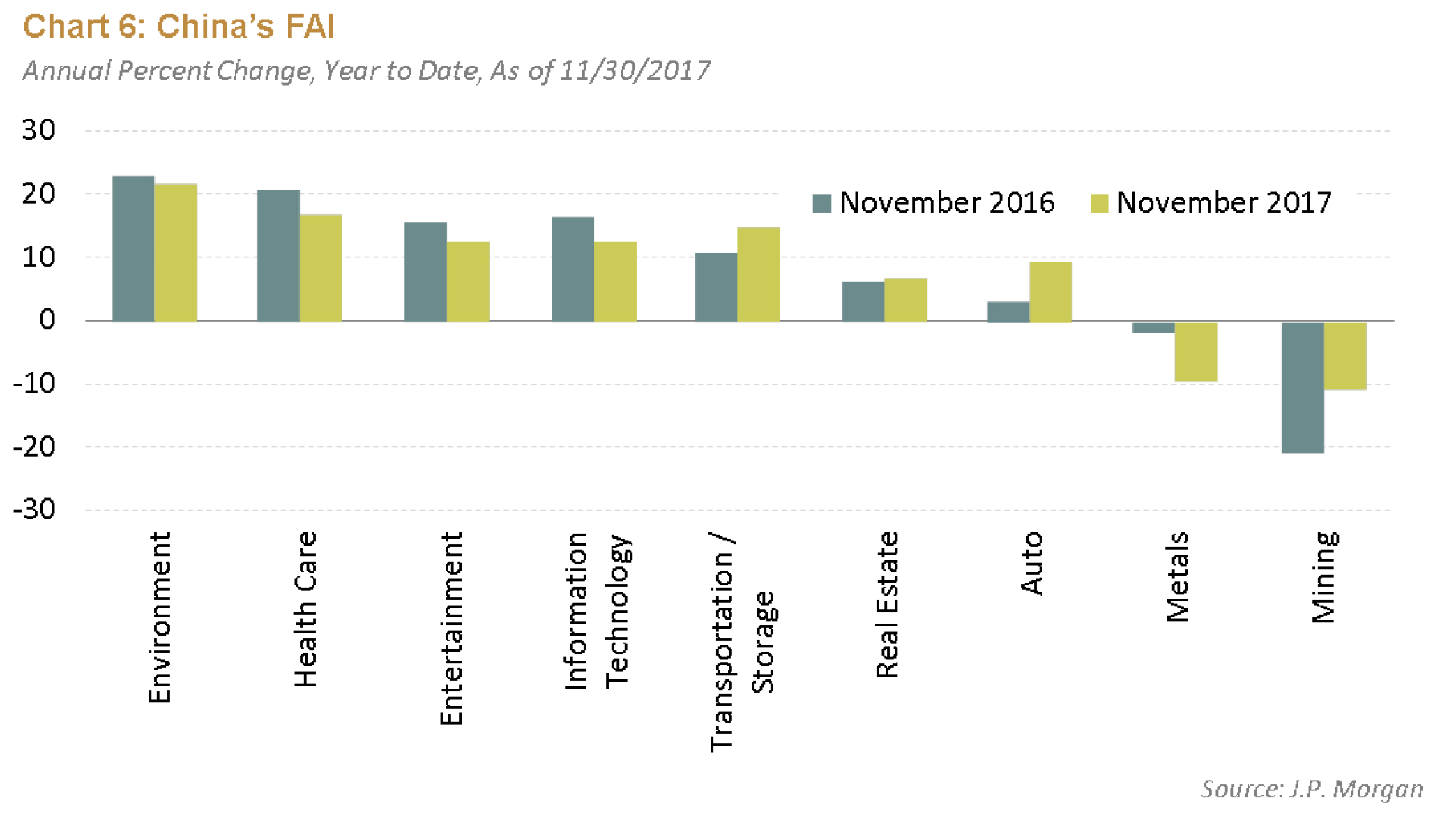

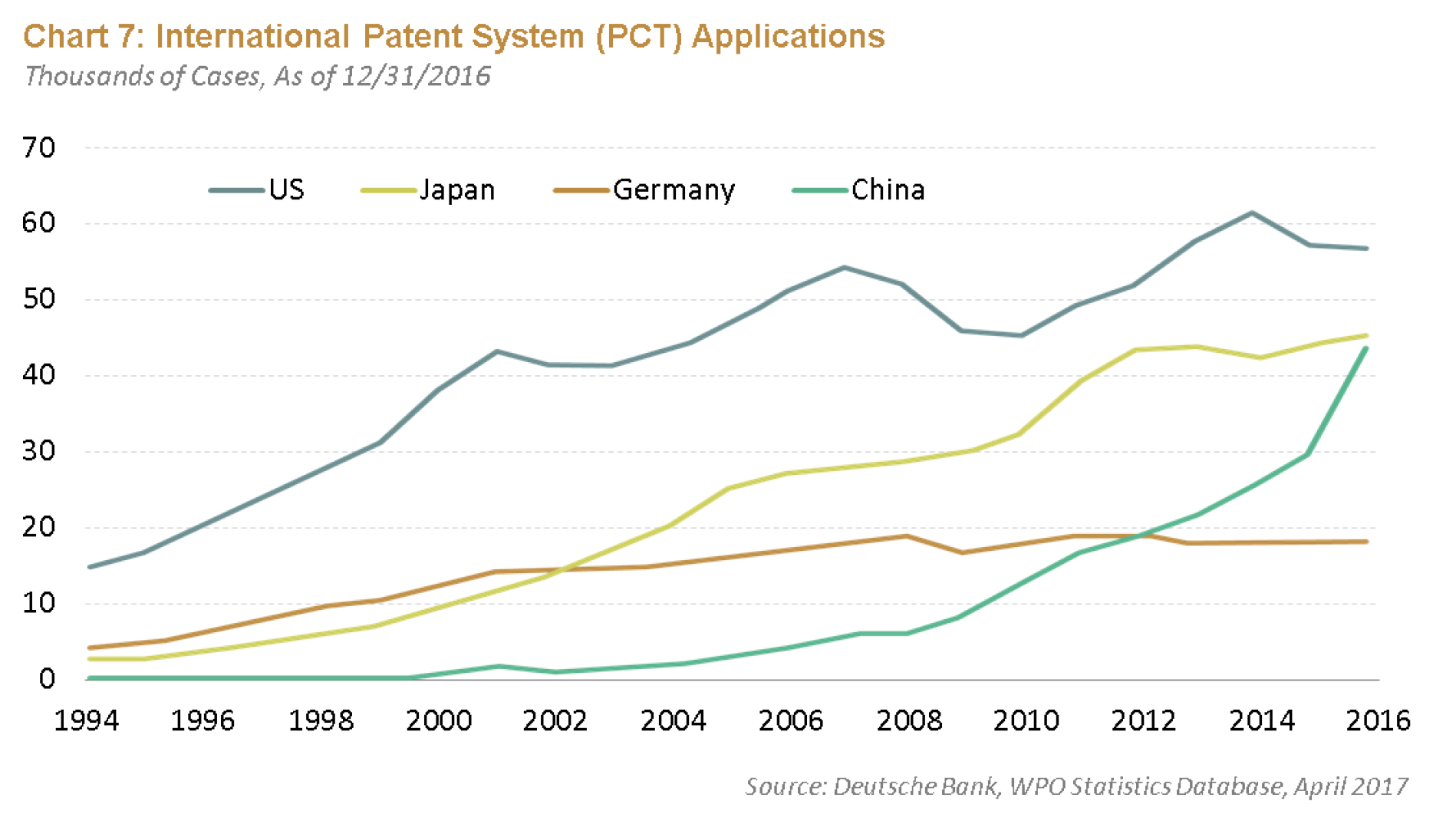

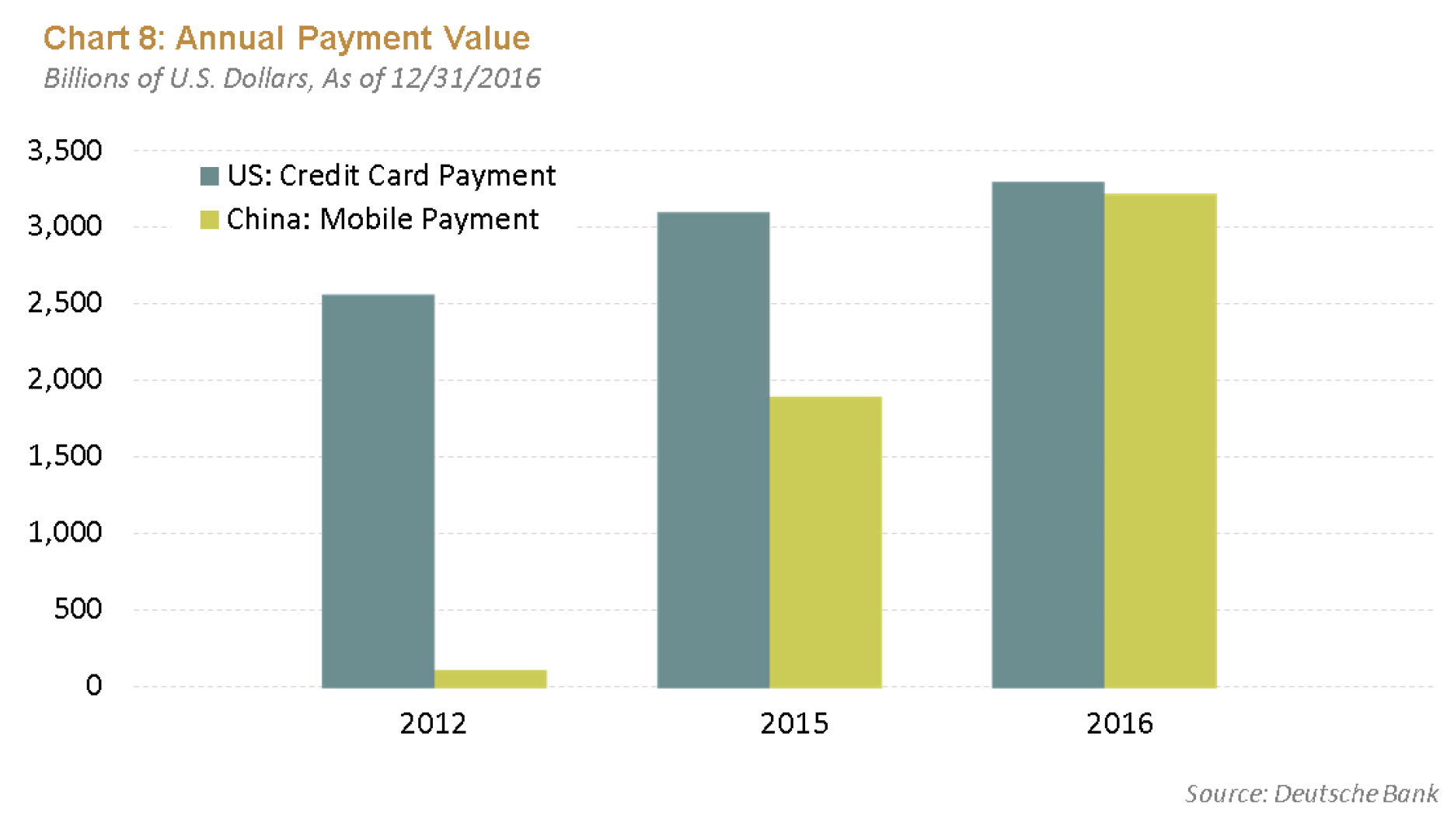

It is also interesting to look at China’s fixed asset investment (FAI) growth as the country shifts from an old economy focused on low value-added manufacturing to the new economy characterized by high value-added manufacturing, services, clean energy, and technology. In this new economy, China has seen FAI in the environment, healthcare, entertainment, technology, and transportation all grow above 10%, whereas FAI in metals and mining has experienced negative growth (see Chart 6). The Chinese government focuses on promoting innovation as evidenced by increasing patent applications (see Chart 7). China, which has been surpassing developed countries in its move toward a cashless society, has seen its mobile payments grow to about the same size as the U.S. credit card market in terms of annual payment value (see Chart 8). Thanks to government subsidies, abundant data, and a large talent pool, China is leapfrogging the U.S. in the digital economy, or at least shrinking the gap, in terms of mobile payments, ecommerce transaction volume, and computing power.

5. The New Connectivity

Investors also have been cautioning against China’s wasteful infrastructure investment, like “bridges to nowhere.” Undoubtedly, there are some wasteful projects, but the immense connectivity network of China’s infrastructure will surely have long-term benefits, such as boosting productivity or supporting the rise of more mega-cities. By the end of 2017, the total high-speed railway operating length reached 25,000 km, connecting over 180 cities and 370 townships. This expanded reach shrinks the concept of time and distance and supports the concept of “China speed” by providing better connectivity among cities and regions, transporting people, goods, and capital. Resources will be reallocated to promote closer economic connectivity inside and across China. The new way of life and commuting, supported by transportation and infrastructure improvements, also increases the mobility of the labor force.

Conclusion

As a leading economic indicator, exuberant consumer confidence usually is a harbinger of stronger economic growth and even higher asset prices. Will the above five confidence drivers—wealth effect from the property boom, improving environment, great rebalancing, new economy, and new connectivity—be able to sustain this confidence at such a high level in 2018? I would not hang my hat on that yet.

Liu He, the prominent advisor to President Xi, elaborated on China’s “One Goal, One Theme, and Three Battles” at the Davos World Economic Forum. The one goal is to transition Chinese economic growth from a focus on quantity to a focus on quality. The one theme is to continue pushing forward the supply-side structural reform. The three battles are dissolving and preventing systemic risk, reducing poverty, and cleaning up environmental pollution. With those missions in mind, policymakers will carry on with financial deleveraging, supply-sidedecapacity, and pollution control. We expect both monetary policy and fiscal policy will stay neutral and prudent with a tightening bias. In all likelihood, financing costs will move higher along with more coordinated financial regulation while the property market will continue its cooling process. Therefore, those short-term pains will moderate China’s economic growth in 2018 in exchange for a longer-term gain. Due to the high leverage of property developers and certain local governments, we likely will see the pressure from financial tightening on both, reflected in higher defaults and more consolidations. Government’s implicit guarantees will be tested. As a result, consumer confidence will be tested as well. However, robust and synchronized global growth, exports, consumption, and the new economy should provide some offsets to the moderate slowdown.