Family trusts – a growing force in the Australian economy

Brian Hor

Family trusts have always been an important structure for business planning, tax planning and estate planning, mainly due to their tax efficiency, asset protection, flexibility and succession possibilities.

Increasingly, they are being used for retirement-planning purposes following the Government’s introduction of more measures limiting the ability to make both concessional (up to $25,000 per year) and non-concessional (up to $100,000 per year or $300,000 for three years) contributions to superannuation funds.

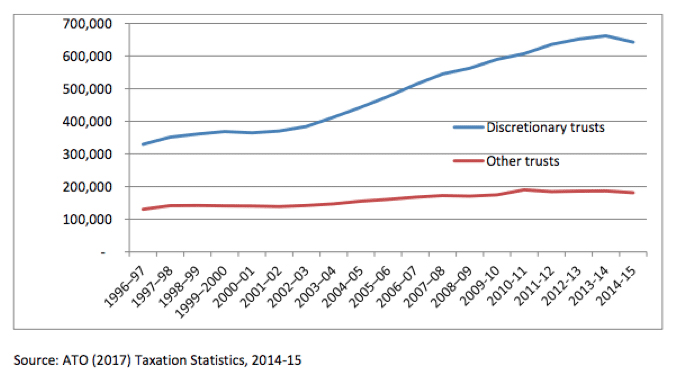

ATO figures show discretionary trusts grew around 95 per cent from 1996-97 to 2014-15.

“While it’s still too early to know what effect the July 1 changes to super will have on the use of trusts, I have seen a significant increase in the use of trusts over the past five years,” said Brian Hor, Special Counsel, Superannuation & Estate Planning at SuperCentral.

Additionally, tax-free pension amounts are now capped; transition-to-retirement income streams are no longer tax-free; and there are constraints on the ability to use limited recourse borrowing arrangements (LRBAs) to circumvent the caps and/or contribution limits.

By comparison, family trusts are not subject to stringent legislative restrictions on issues such as:

- requiring a sole purpose test

- limits on trust membership (i.e. who can be beneficiaries)

- to whom distributions can be made

- conditions of release

- what you can invest in

- trust borrowings

- transactions with related parties.

Trust, Super – or both?

All of this doesn’t spell the end for SMSFs – they are still the most tax-effective vehicle for members in pension phase; they still attract very low tax on earnings in accumulation phase; they can still access a CGT discount of one-third if the relevant asset was owned for at least 12 months; and they are still great as tax-effective vehicles for holding business real property.

However, what it does mean is that, post-1 July 2017, the ideal retirement strategy is now a dual structure: an SMSF for tax free income up to your Transfer Balance Cap, and a Family Trust for excess monies where you are unable to contribute more to super, or if you can do better than the 15% tax flat rate on your super accumulation account.

Scenario

For example, a non-working spouse and 2 kids at university with the Low Income Tax Offset can receive around $60,000 per year tax free on $1.2m invested at 5% in a family trust – a saving of $9,000 per annum as compared with paying 15% on those earnings in a super accumulation account.

A family trust is also useful if you need greater flexibility in terms of access to your funds, and the ability to gift or lend funds as compared to super.

Check your trust deeds regularly

Importantly, family trusts still do need to be regularly updated for changes in the laws and in the family’s circumstances. At the very least an existing trust deed needs to be reviewed for reasons such as: the trust deed may be too inflexible (especially as regards the power of appointment of the trustee, or power to amend the trust deed); the trust deed may be incorrectly drafted (e.g. it may contain the wrong parties – or it may even be invalid from the start!); the trust may be close to vesting (or may even have already vested); or the trust deed may simply not say what you think it does – especially regarding who are the beneficiaries, or the exclusion of so called “notional settlors”.

By Brian Hor, Special Counsel, Superannuation & Estate Planning