Brad Potter

Reflection on 2017

In early 2017, I suggested a total return of 12-15% was a reasonable expectation given the rotation from defensive, secular growth and bond-sensitive stocks towards the cyclical and value end still had some way to go. Well, the forecast was a little high as total return for the ASX 200 accumulation index was 11.8%.

Surprisingly, interest rates stayed pretty stable across the curve in both Australia and USA, with 10-year bonds ending the year largely unchanged. The bond sensitive stocks recovered all the underperformance and more from the 2H 2016.

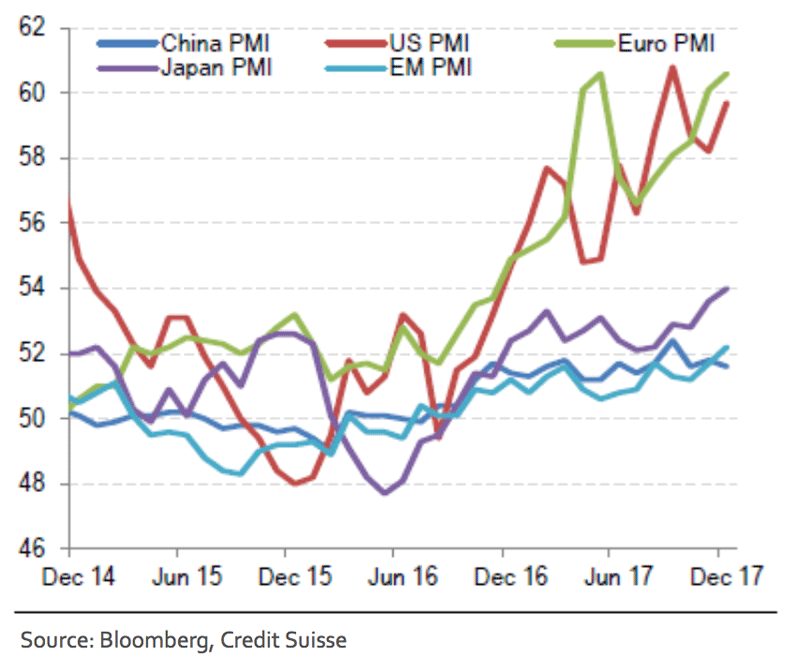

The years of slack monetary policy exacerbated by quantitative easing appear to have finally lit the fire under the global economy. We are in the middle of a synchronised global recovery with Purchasing Managers’ Index (PMI). The net result of the strong economic growth has been corporate profitability growing strongly, which is reflected in strong earnings growth revisions.

The bulk commodities surprised on the upside as a number of policies implemented by the Chinese government kept prices high.

The Domestic Economy

The domestic economy confounded the naysayers during 2017. Business conditions have rarely been better and unemployment levels are at very low levels.

The mining states that suffered during 2016 have recovered somewhat. Many mining companies have started to re-employ considering, in hindsight, that they probably cut too deeply initially given the combination of high export volumes post the expansion phase and reasonable prices. The non-mining states have been building momentum for some time on the back of a broad-based construction boom.

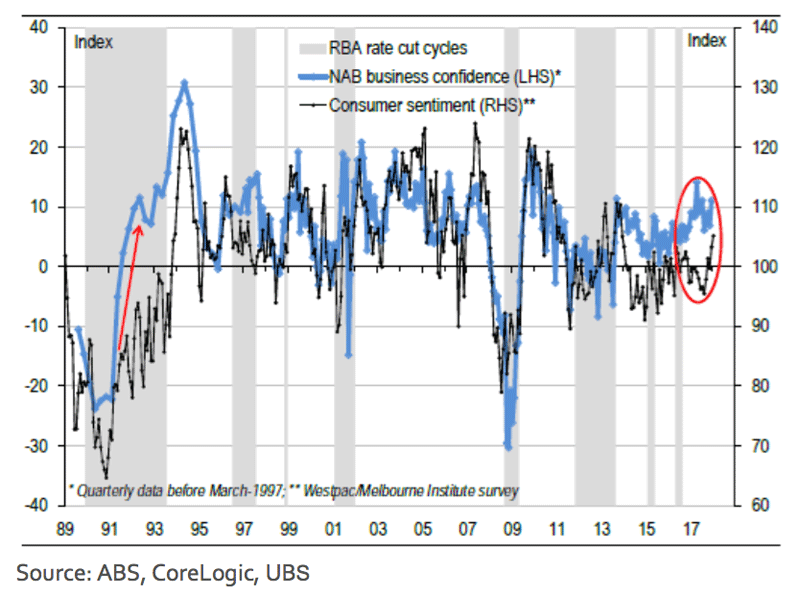

Chart 1: Divergence between consumer sentiment and business confidence narrowing on employment boom

Consumer confidence has been largely uninspiring compared to business sentiment, which isn’t helped by low wages growth and inflation in utility bills, insurance and council rates. Despite this, consumers appear to be spending. However, the latest consumer sentiment reading rose 1.8% month-on-month (~8% over the year) and is the highest since late 2013.

Rising confidence in the outlook for future economic conditions and a strengthening labour market helped drive the improvement. It is interesting that the increase in confidence was more pronounced for mortgagors compared to renters — perhaps suggesting fewer concerns on higher rates for the former.

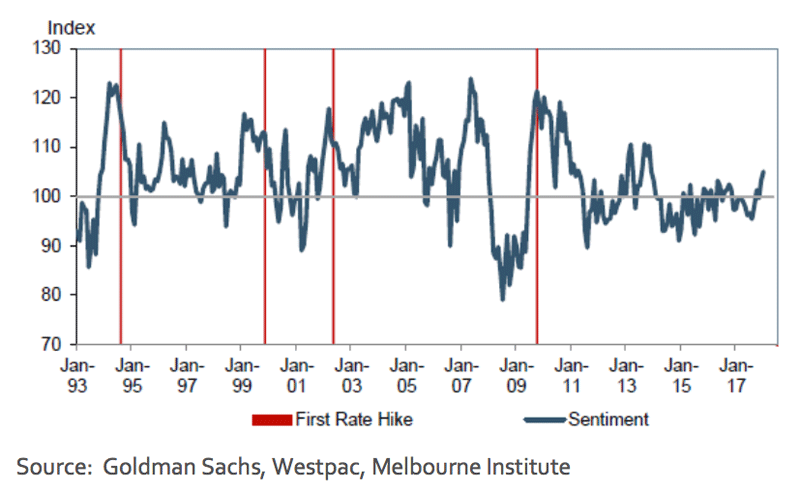

Chart 2 Consumer Sentiment and First Rate Hike

Government spending on infrastructure both at state and federal levels continues to surprise as new projects get unveiled. The economy will be supported over the next few years with the work on current and forecast projects.

Deloitte Access Economics is forecasting the $4b trough in rail and road projects that occurred in 2015 will peak to around $16b in 2020. Macromonitor, an Industry research group, is more bullish suggesting a $35b peak in 2019/20. The stress on infrastructure has become acute and governments are finally recognising that real solutions are required.

Housing

It is difficult to envisage a national housing collapse without coincident rising interest rates and much higher unemployment, with the latter being key. We have witnessed micro housing collapses in the mining states as job losses resulted in forced sales with little buy side demand. Banks saw impairment and stress levels rise but from extraordinary low levels, and most banks are now saying the bottom has been reached and they are seeing good recovery.

Unlike other countries, the Australian regulators have been acting together and thus have put forward a number of macro prudential policy decisions to reduce the excesses. For example, limits have been put on interest only loans resulting in banks increasing mortgage rates and thus incentivising principle and interest products. Foreign property buyers are paying increased taxes and duties, and banks are becoming even more diligent with lending practices.

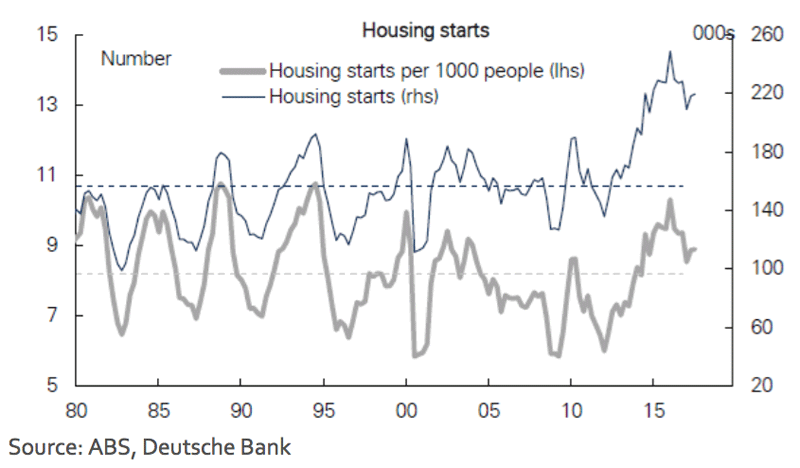

It is interesting to reflect that although housing stats have peaked at absolute levels well above previous peaks, when adjusted for the population growth, the peak is much more modest. It is difficult to envisage a severe house price fall without an economic shock, and a more modest house price correction is unlikely to be materially disruptive.

Chart 3 Housing Starts and relative to population

China – Beautiful China – Transforming From Fast Growth to High Quality Growth

Pollution reduction, state-owned enterprise (SOE) reforms, supply-side structural reforms, combined with controlling property prices were the main tasks outlined post the 19th National Congress of the Communist Party of China. There is no doubt that President Xi Jinping is putting his stamp on the Communist Party; essentially having as much power as any other over the past few decades. The anti-corruption effort will remain front and centre of President Xi Jinping’s goal of de- risking the financial sector, reducing excess capacity and pollution, and alleviating poverty.

Recent data clearly shows the Government is slowing the economy, with a primary objective to transition from fast growth to high quality growth. The Government will achieve this higher quality growth by evaluating local governments on the basis of efficiency (or ‘total factor productivity’ TFP) rather than the traditional GDP.

In our view, the economy will slow and transition to a more balanced and environmentally-friendly country. Fixed asset investment is destined to slow substantially over the next decade and consumption will rise. The growth in the middle class will continue to drive the incredible transformation that is occurring in China. In the short term, a property slowdown is a potential risk in 2018 as the Government tries to reign in speculation, but also effectively accommodate the low income workers.

The political aspiration of the Chinese government is to reduce annual emissions by 50–70%. This target is likely to take 10+ years and will result in profound changes to the industrial China we know and understand today. The net result of the supply- side reforms and crackdown on the environment is that high quality inputs (materials) will likely remain priced above long- term averages for some time.

In our view, industries and SOEs will consolidate and be encouraged both economically and legislatively to use inputs that are less polluting and enhance profitability. Demand for high-grade iron ore, coal and liquefied natural gas from Australia will remain high.

Iron Ore – A Tale of Two Grades

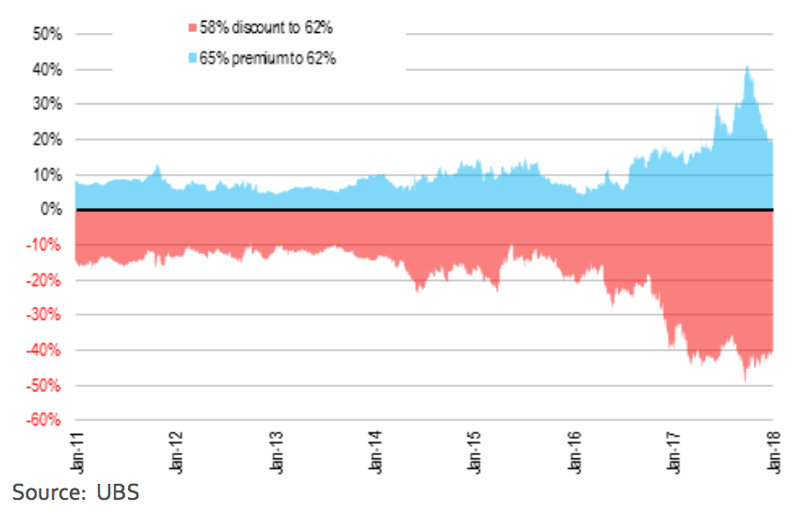

The pricing bifurcation of the iron ore market into high grade and low grade has materially changed iron ore market dynamics. Steel mills have been preferentially buying high quality iron ore versus low quality to maximise volume growth and offset the high coal prices.

Mitigating the high metallurgical coal prices were the initial reason, but this was overtaken by maximising steel volume given the high steel prices and concerns around reducing environmental emissions. Prior to 2017, 58% of iron ore typically traded at a 20% discount to the 62% benchmark price – this has now blown out to 41%.

Chart 4 Discount and premium of high and low quality iron ore over the 62% benchmark price

The consensus view was that iron ore would be in surplus in 2017 and so prices would fall. However, steel mills were motivated to purchase high grade iron ore and scrap metal to fill the blast furnaces and so a shortage of high grade ore was created. The large stockpiles in China are the currently undesired low grade ore.

It is noteworthy that Fortescue is now taking the view that the huge blow out in margin between high and low quality ore is structural—not cyclical—and is taking action to high grade their mined product. Given the obvious move to a cleaner, more environmentally friendly China, it appears this may be a structural issue. We will see when steel prices fall, but note that the recent decline in margins in China’s steel mills is restoring interest for lower grade iron ore at the ports.

The Banks

A long anticipated royal commission, Commonwealth Bank of Australia (CBA) tripping over multiple banana skins and Australia and New Zealand Banking Group (ANZ) shrinking to greatness are all areas of interest in banks starting the year.

The issues around capital have now passed with banks selling non-core assets and low returning business to move core equity Tier 1 (CET1) to levels that are within Australian Prudential Regulation Authority’s (APRA) guidance. In the case of ANZ, they arguably have +$6b in excess capital that will be returned to shareholders via on market buybacks.

The Royal Commission into misconduct in the financial system services sector appears to have a much more limited scope than many feared and includes the entire financial sector. The investigation into misconduct, and any conduct that falls below community standards, will be disruptive for the banks and certainly a distraction for management.

Compensation schemes for impacted consumers and recommended remedies for the causes of the misconduct are likely. It is, however, difficult to determine the ultimate ramifications to the banks both from a penalty and operational perspective.

ANZ and National Australia Bank (NAB) are moving down the cost out path that should result in real costs coming out of the banks rather than some esoteric lowering of the cost to income ratio due to revenue growth. This will be the first time in over a decade that real costs reductions will hit the bottom line. Westpac and Commonwealth Bank are taking the road ‘well- travelled’ and managing costs via the cost to income line. The profit prize for banks to right size their businesses to the current top line growth outlook and technology advances is large.

Asset quality remains benign and impairment charges are at 30- year lows. There has been no systemic poor lending practices that will drive a meaningful bad debt cycle over the short to medium term. Nikko AM Australia valuations assume reversion back to more normal mid-cycle loss rates despite the indications that this seems some time away.

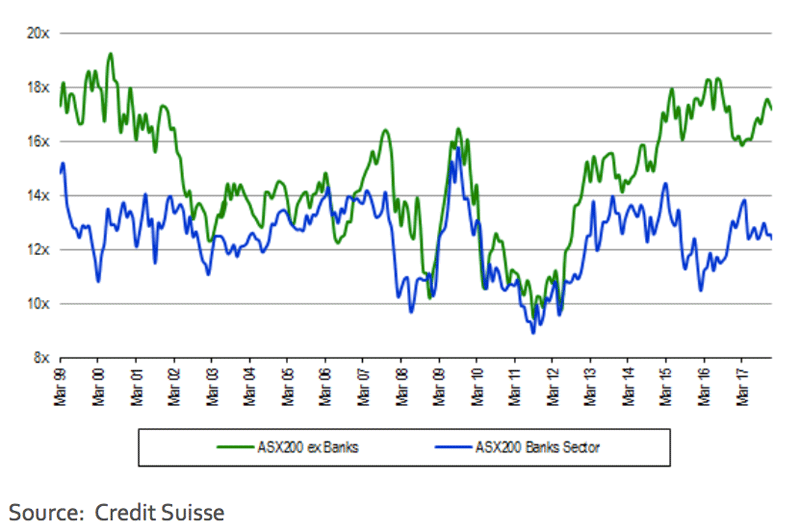

Recent research from Merrill Lynch is music to a value manager’s ears. Their work highlighted that valuation is the one common factor in periods of sustained bank outperformance since 1999. Headline grabbing issues such as earnings per share (EPS) growth, return on equity (ROE) and other political/event risk headlines are much less reliable return signals.

The valuation metrics currently suggest that the banks are oversold and certainly look attractive compared with history. The banks, ex CBA, are all trading +1 standard deviation cheap versus the market; have a benign bad debt outlook but their capital positioning is fine and, in the case of ANZ is in excess. Dividend yields remain high at around 6% fully franked and are sustainable. Nikko AM Australia’s long term sustainable earnings valuation suggests the banks look great value versus the market – albeit with little growth.

Chart 5 12 Month Forward Rolling PE – Bank Sector vs ASX200 ex Banks

Earnings

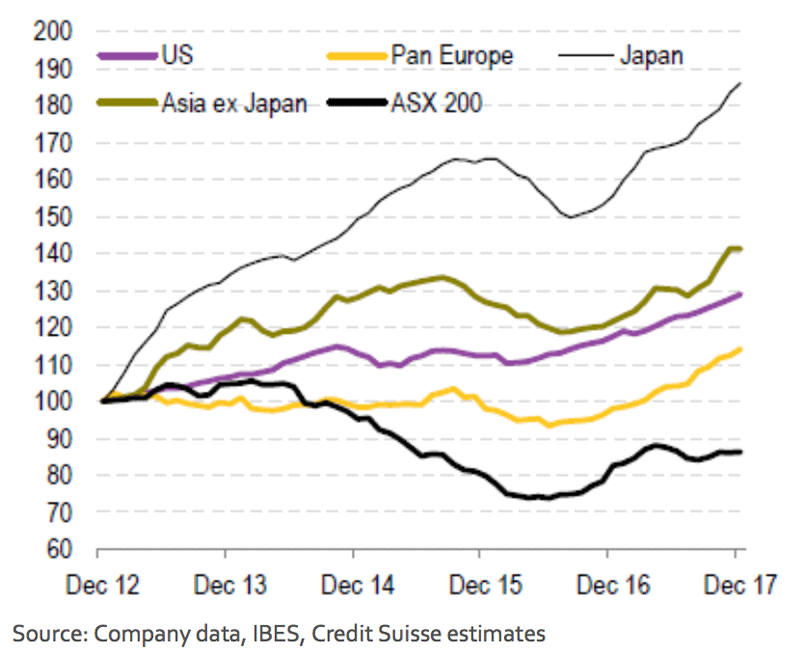

Global earnings continue the trend that started in mid-2016 with revisions improving both in geographical and sector breath. Cyclical sectors dominate the positive trend in earning revisions as one would expect in a global reflation trade. Secular growth stocks, bond sensitive and defensive stocks are all likely to de-rate during such a reflation trade.

Profit growth within Australia has not been as strong over the past few years but it also didn’t fall as far either. Economically sensitive sectors such as cyclical, commodity and other financial companies have provided the growth, with defensives and banks the weakest. The big four banks have had the headwind of macro prudential regulation that is now abating. The top line growth for the banks should remain modest, but it is arguably all in the price. Looking forward into 2018, the market appears to have a more balanced view of where the growth emerges.

Chart 6 EPS for Major Equity Markets (Local Currency – 12 Month Forward)

Chart 7 Synchronised Global Expansion

Oil

Three core questions are paramount when determining the price of oil:

- Will the OPEC supply discipline remain?

- Is US shale oil/gas able to make sustainable profits/cash

flows and thus grow production? - What is the demand outlook vis-à-vis the synchronised

global growth.

Further, longer term questions are worthy of discussion – such as the electronic vehicle revolution. However, in our view the impact of this is much further out and unlikely to materially impact for a number of years despite Elon Musk’s bold predictions.

The Nikko AM Australia view for some time is that Saudi, in particular, is strongly incentivised for the supply discipline to remain and thus prices to remain high. The market is also underestimating the fragility of many Organization of the Petroleum Exporting Countries (OPEC) members and thus very little political risk premium is currently in the oil price.

The oil shale producers have consistently been unable to generate free cash flow – even at much higher oil prices, and now investors, both credit and equity, are asking for returns. Costs are rising, labour is a problem with fracking crews in short supply, key inputs such as fracking sand is scarce, and the best reservoirs may have been already drilled. There is an argument that the oil shale model is broken and can’t fill the supply gap. The distinct lack of deep water exploration and development over the past few years implies a long lead time for this potential production to come into play.

Therefore, the combination of global synchronised growth and lower production provides confidence on the outlook for oil price.

Mergers and Acquisitions

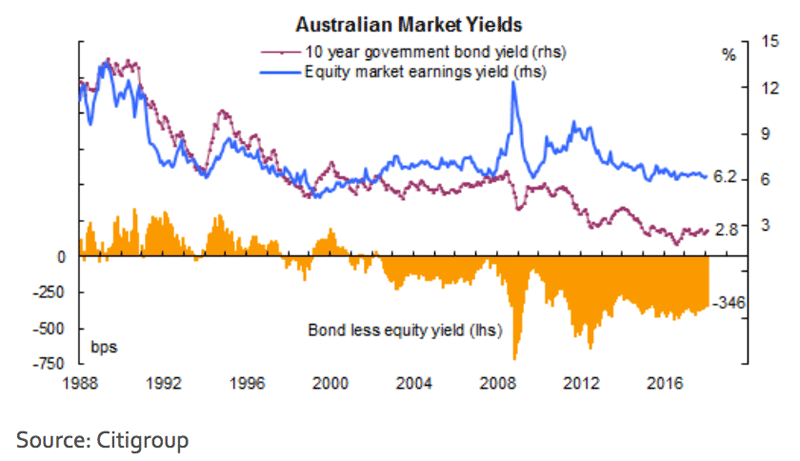

Mergers and Acquisitions are likely to remain at elevated levels in 2018 both globally and within Australia. Interest rates remain at extremely low levels despite the world in a synchronous economic growth phase.

Business confidence and conditions are high – management and boards can purchase growth at low funding costs, making the metrics of takeover deals attractive with the view that funding costs are unlikely to be any better. The earnings yield to debt yield spread remains at wide levels compared to history and thus a debt-funded acquisition can be accretive virtually from day one.

Chart 8 Australian Market Yields

The Snap Back To Value – Part Deux

Nikko AM Australia previously highlighted the huge differential in pricing between the ‘value’ stocks and the ‘quality’ low volatility stocks. The defensive bull market that saw the safe companies and secular growth stocks rally to unsustainable highs ended in August 2016. However, 2017 saw many of the defensive and bond sensitive companies retrace most of the correction as bond yields remained stubbornly low and the market seemed unconvinced on the reflation trade.

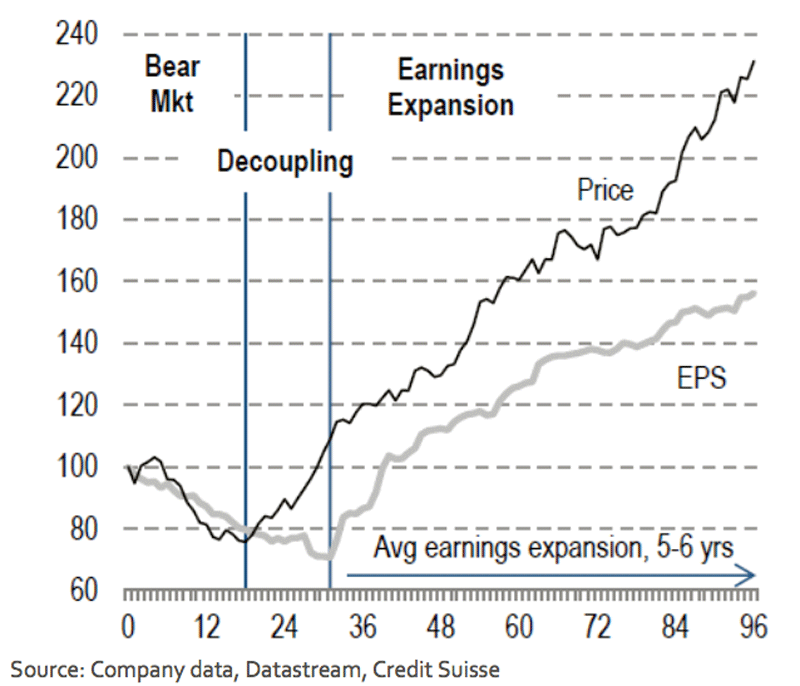

The initial rerating of the economically sensitive stocks, such as industrial cyclical, financials and material stocks, has passed and we are in the earnings expansion phase that can last 5–6 years. The aggregate market PE is a meaningless number under this scenario as it will likely fall or remain stable as earnings and price move together.

The rerating of the economically sensitive stocks and commensurate derating of defensives, secular growth and low volatility stocks will generate substantial alpha for a well- positioned active value manager such as Nikko AM Australia.

Chart 9 The Australian equity market cycle – average of previous four cycles

Conclusion

The combination of global synchronous growth, together with the ongoing accommodative monetary policy, should see strong earnings growth globally continue and Australia will be pulled up with it.

The Nikko AM Australian Share Wholesale Strategy is well positioned to take advantage of the economic upturn as we are overweight attractively valued cyclical and financial companies that are leveraged to the upswing. The stocks in the portfolio have been selected via our detailed, disciplined and extensive research that value them on long-term sustainable earnings and a balance sheet that is appropriate.

The aggregate market PE appears slightly expensive based on the average of the past 20 years of low inflation. However, it provides no insights into the market trajectory and given our belief that we are at the start of a long profit cycle, the earnings growth will drive stock prices higher. The expectation, like other profit cycles, is the market PE will remain flat at best but likely fall as earnings growth is greater than stock price appreciation.

Given the market dividend yield is around 4.5% and earnings growth of high-single digits is a reasonable assumption, a total return in the market of between 11–14% for 2018 is envisaged. Given the starting point for the market PE no PE rerating is likely. The risks to this, as always, is geopolitical volatility.

By Brad Potter, Head of Australian Equities