Josh Callaghan

Canstar has released 2018 Superannuation Star Ratings research, identifying 7 super funds for offering outstanding value to Australians.

Australia’s biggest financial comparison website*, Canstar has released its 2018 Superannuation Star Ratings research, highlighting the super funds offering Aussies outstanding value and investigating the impact that default life insurance cover could make to Aussies’ retirement balances.

Insurance in super can act as a safety net for many Australians, offering a level of protection in the instance they or their loved ones need to draw upon it. However, insurance held through super can represent a significant cost over a lifetime and can reduce a person’s overall retirement benefits.

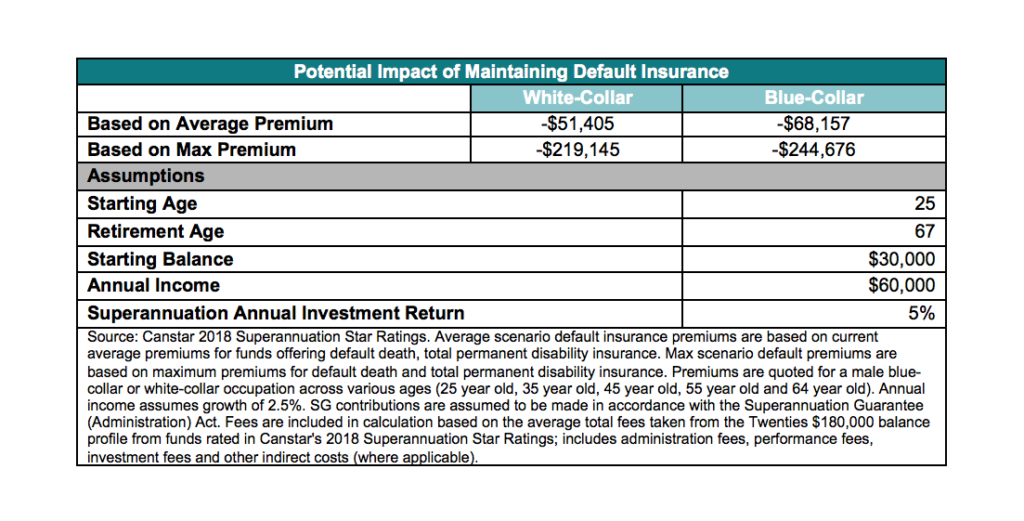

Canstar has calculated the impact to your nest egg of opting out of default life insurance, finding that forgoing life insurance could potentially increase your super balance by over $200,000 at retirement.

However, Canstar’s superannuation expert warns of the importance to carefully weigh up the savings of opting out of default life insurance against the peace of mind offered by the insurance, particularly at different life stages.

Canstar’s superannuation expert, Josh Callaghan explains, “Many Australians with default life insurance cover in their super may not even realise they are paying for the privilege, how much they are paying for it or what is included in the cover. If their circumstances don’t warrant such cover, it could be needlessly eating away at their retirement nest egg.”

Canstar’s investigation shows a 25-year-old blue-collar non-smoking male starting with a $30,000 superannuation balance and an annual income of $60,000 could retire with up to $244,676 more at age 67 if he opted out of the default insurance within his super compared with if he kept it.

This balance was deduced using the maximum annual default death and total permanent disability insurance premiums charged by those considered in Canstar’s 2018 Superannuation Star Ratings.

“Sacrificing life insurance to retire with an extra $200,000 sounds very tempting, especially when you’re young with fewer responsibilities. However, finding yourself underinsured later in life when you have significant financial commitments can be a serious concern and shouldn’t be overlooked,” explained Callaghan.

“Sacrificing life insurance to retire with an extra $200,000 sounds very tempting, especially when you’re young with fewer responsibilities. However, finding yourself underinsured later in life when you have significant financial commitments can be a serious concern and shouldn’t be overlooked,” explained Callaghan.

Consider the profiled white-collar non-smoking male who decides to opt out of default insurance at age 21 to save money and boost his retirement balance. If he then decides to take up insurance when he had a mortgage and family to contend with at say age 35 those insurance free years could mean an extra $25,000 in his retirement nest egg. This isn’t as significant as the possible $244,676 savings if he opted out for life, however it will mean from age 35 onwards he’s got cover to protect him and his family.

“Keep in mind that if you do opt out of the default insurance, it’s unlikely you will be able to opt back in with your current super fund. You will instead need to apply for tailored insurance or if you specifically want default insurance, you would be required to switch super providers,” noted Callaghan.

“It is important to remember there are many factors to consider when choosing a super fund in addition to the insurances on offer, such as past performance, ongoing fees and the advice on offer.”

If you’re unsure of whether you are paying for a default life insurance policy through your super fund, check your super statement or ask your fund directly to understand what you may be covered for.

To give you an insight into the likelihood of you already having default insurance through your super, out of the 63 superannuation accounts rated in Canstar’s 2018 Superannuation Star Ratings (for a 25-year-old), 35 funds offer default death cover, 33 offer default total permanent disability and only 11 offer default income protection.

Who offers outstanding value when it comes to superannuation?

After researching and rating 63 superannuation accounts, Canstar has revealed seven 5-Star Rated recipients for Outstanding Value in its 2018 Superannuation Star Ratings.

Canstar’s 2018 Superannuation Star Ratings are calculated using a sophisticated and unique ratings methodology that considers performance, fees and product features across superannuation products. Ratings range from one to five stars, with five star-rated products being assessed by Canstar as offering outstanding value to consumers.

Following are the seven 5-Star Rated recipients as rated by Canstar, sorted alphabetically by fund name.

- AustralianSuper

- CareSuper Personal Plan

- Energy Super

- HOSTPLUS Personal Super

- StatewideSuper Personal Plan

- Sunsuper for Life

- VicSuper FutureSaver

These 5-Star Rated recipients have demonstrated robust net investment returns across the previous five years, as well as competitive product offerings, specifically when it comes to financial advice, tools and education, member access, contribution methods and beneficiary options.

Learn more about Canstar’s 2018 Superannuation Star Ratings and methodology.