Louise Biti

The Government handed down the 2018 Federal Budget on 8 May. With an ageing population and baby boomers starting to head towards care years there was a major focus on aged care and helping retirees to improve access to income. Personal tax changes also featured, but with a long lead-in time.[1]

Impacts for aged care Several aged care reviews have been conducted over the last 12 months, focussing on all aspects of aged care from financial viability of the sector to consumer protections and client contributions. The main review was the Legislated Review of Aged Care (Tune Report).

Clients will be relieved to learn that changes were not proposed to the consumer contributions. Most of the proposed changes focussed on increasing the number of care places and helping clients with additional income to fund income needs, including access to care.

———

Client conversations

The Government recognises the increasing cost burden and difficulty of funding aged care solutions in the home particularly given long waiting times for home care packages. Advisers need to start the aged care conversation early with clients including during pre-retirement and early-retirement planning. Retirement planning conversations should factor in the costs of aged care and anticipate home care needs with pre-retirees who are saving for retirement as well as retirees who are looking at income drawdown strategies.

Conversations with clients should include:

- How clients expect to fund their aged care costs – highlighting that legislation has been shifting towards a greater user-pays basis

- The role of the home in meeting aged care costs – including the client’s willingness to access the equity in their home

- Ability to rely on family and friends to provide care and financial support

- If they move to residential care, what options they may have for funding the accommodation deposit and ongoing costs.

———-

Home care packages

Demand for government-funded home care packages is increasing, with around 105,000 people currently waiting in the National Queue for a suitable package to be allocated. As an interim measure, some clients may be receiving a lower level package than approved.

In December an additional 6,000 packages were allocated, and this Budget announced an additional 14,000 packages over four years from 1 July 2018.

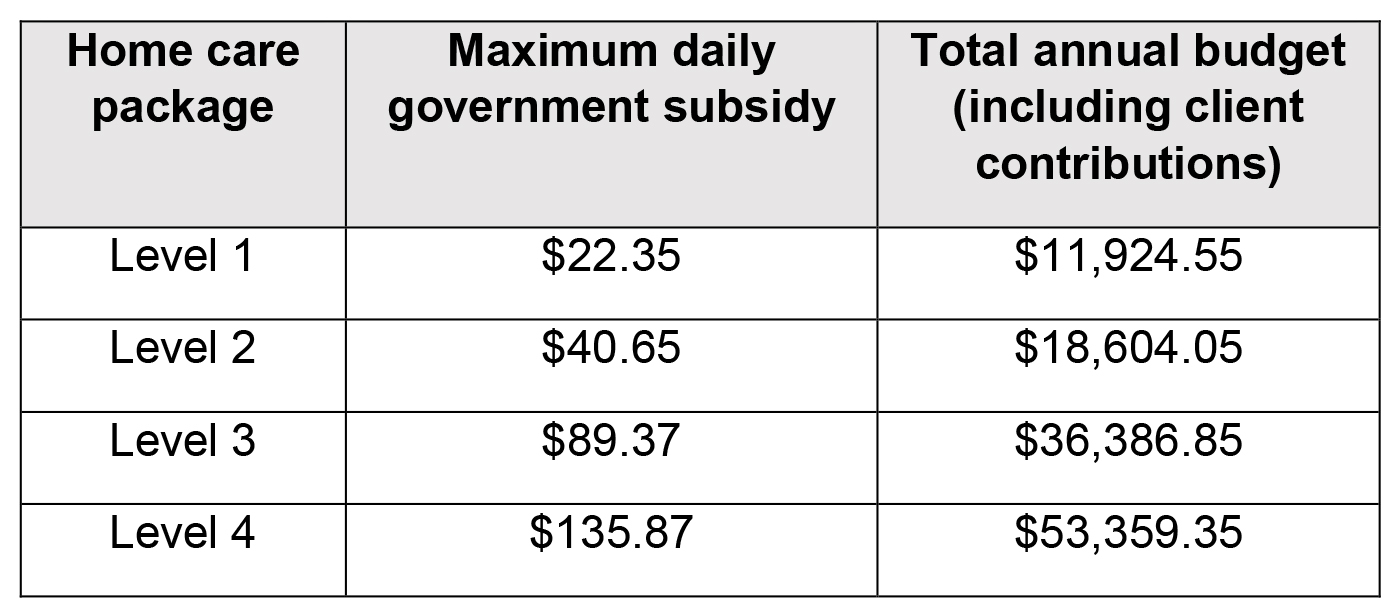

Home care packages are approved at four levels of care, with varying levels of available budget. The package budget includes contributions paid by clients as well as the subsidies paid by government.

Clients pay a basic daily fee of $10.32 towards the home care package and this may increase up to $39.95 per day based on assessable income. These contributions are included in the annual package budgets shown in the table above.

On average, the government pays around 90% of the package budget with client contributions only accounting for around 10%.

No changes were proposed to government subsidies or client contributions.

———-

Client conversations

Many clients are afraid to ask for help as they think this will trigger a move into residential aged care.

The increased focus on home care provides an opportunity for advisers to start conversations with older clients about accessing services that can help them remain independently in the home for longer, with a better quality of life. This might also be a conversation to have with younger clients who are worried about ageing parents.

The proposed changes to the Pension Loan Scheme (discussed later in this paper) may provide an option for clients to use equity in their home to provide a safe place to live by funding private home care to fill in the gap while waiting for a package to be allocated or to top-up an existing package with additional services.

———-

Residential care

Additional funding has been proposed to introduce 13,500 new residential care places and 775 short-term restorative aged care services in 2018/19.

To encourage providers to build new aged care services, $60 million will be allocated towards capital investment for new places. Another $40 million will be allocated to providers in regional, rural and remote areas for construction and improvement, plus $105 million for aged care services in remote indigenous communities.

Additional funding will be allocated for palliative care services in residential care (subject to matched funding from the states and territories) as well as innovations in managing dementia and mental health programs for older Australians.

Home care packages are allocated to the consumers (under consumer directed care) rather than the providers, but residential care packages are still allocated to the provider. An impact analysis will be conducted to determine the impact of allocating residential care packages to the consumer.

An important consumer protection in residential care is the government guarantee of refundable accommodation deposits (RADs) and refundable accommodation contributions (RACs). This guarantee is proposed to continue but a levy on care providers will be introduced to recover costs from care providers.

Supervision of aged care

As the government recently announced, a new Aged Care Quality and Safety Commission will be formed to combine the functions of the Australian Aged Care Quality Agency, the Aged Care Complaints Commissioner and the regulatory functions of the Department of Health.

This will provide a single point for clients to make complaints about poor levels of care.

Proposed commencement: 1 January 2019

Funding will be allocated over the next few years to improve the quality of residential aged care and enhance regulation of aged care provider quality so that risks are identified and acted upon more quickly.

Simplifying the application process

Dealing with the paperwork and application processes can be difficult for older Australians and their families. Proposals were announced to further improve MyAgedCare and simplify the application forms.

A trial project of navigator services to assist people with choosing appropriate care services will receive funding of $7.4 million over two years from 1 July 2018.

The Government proposes to combine the residential care and home care programs from 1 July 2018 to allow greater flexibility in funding various packages according to client demands.

Further information on these measures is not yet available.

Protecting against elder abuse

Elder abuse (both physical and financial) is increasing in concern in many sectors of the community.

The majority of financial abuse cases arise from actions by children, including those acting under an Enduring Power of Attorney. This abuse is sometimes deliberate and malicious but is often a misunderstanding of what actions they can take using an Enduring Power of Attorney and arise from “inheritance impatience.”

The government announced the following proposals to increase protections for older Australians:

- Funding trials of specialist elder abuse support services

- An elder abuse knowledge hub

- A national plan to address elder abuse and working with the states and territories to develop a nationally consistent legal framework, and

- Establish a National Register of Enduring Powers of Attorney.

Support for carers

Carers carry a large part of the care for older and disabled Australians with around 2.8 million people acting as carers. Many of them need greater support.

The Government has proposed to provide $113.3 million of funding over five years for a new Integrated Carer Support Services model to provide early intervention and preventative services for carers to support the well-being of carers.

This model will combine several existing services into one national model with the Carer Gateway as the entry point for accessing services from October 2018.

Carers may currently receive a non-means tested Carer Allowance to help with the costs of caring for someone. This is proposed to be subject to a $250,000 family income test threshold. If family income exceeds this threshold, the carer would no longer qualify for the Allowance. This is not expected to impact most carers.

Impacts for retirees & Centrelink

The proposed changes to Social Security and Veterans’ Affairs rules are mostly good news and aim to help retirees use their available resources to access higher levels of income.

Pension Loan Scheme

Many retirees are asset-rich and income-poor, particularly with rises in house values.

Proposals to expand the Government’s Pension Loan Scheme may help retirees to turn equity in their home into a regular income stream. This income could be used to meet living expenses or pay for services such as private home care.

The Pension Loan Scheme is administered by the Department of Human Services.

The current scheme allows part-pensioners and some self-funded retirees to top-up the amount of age pension they receive to the maximum available pension. For example, a single person who receives a part-age pension of $400 per fortnight could borrow up to $507.60 per fortnight ($13,197.60 per year) to bring their payments up to the maximum single age pension.

Eligibility criteria for the scheme includes:

- Clients need to own a property to use the scheme as the government will take a mortgage on the property

- Self-funded retirees cannot have age pension entitlements reduced to nil under both the income and assets tests

- Normal pension residency requirements must be met.

The scheme is proposed to be expanded to allow eligible retirees to borrow regular income payments up to 150% of the maximum pension entitlement (less the pension amounts they receive). This opens the scheme to full age pensioners.

Amounts borrowed are paid as fortnightly income and interest compounds on the amount owing at 5.25%. Establishment fees are not charged, but the client may pay legal fees. The amounts borrowed are neither assessable nor taxable income. Age-based limits apply to the amounts that can be borrowed so clients will not owe more to the government than their house is worth.

———-

Example

Tony and Laura are full age pensioners living in a home they own. Tony has been approved by ACAT to receive a home care package and is on the waiting list for allocation of a package. He has been told to expect at least a nine-month wait.

They only have a small bank account and cannot afford to pay for private care services while they are waiting for a government-subsidised package.

However, with the expansion of the Pension Loan Scheme, Tony and Laura may be eligible to borrow up to $17,787 per year of income from the Government (taking total payments including age pension up to 150% of the full couple rate of age pension). Interest at the rate of 5.25% will compound on the debt and repayments are not required until they sell the home or both pass away.

When Tony receives his home care package, they can choose to stop or reduce the pension loan amounts if his home package provides sufficient support to help him remain safely in the home.

———-

Client conversations

This measure creates opportunities for advisers to have conversations with clients on strategies for funding options to pay for private care while they wait for home care packages.

The Pension Loan Scheme (PLS) offers retirees who need extra income an alternative to reverse mortgages with an interest rate lower than the current rates on reverse mortgages.

This may help clients to afford care services while waiting for government funding and minimise putting their health and independence at risk.

The PLS is not suitable for clients who wish to borrow higher income amounts or lump sums.

———-

Proposed commencement: 1 July 2019

Pension Work Bonus

For clients who are age pension age, the first $250 per fortnight of employment income is excluded under the income test. This is proposed to increase to $300 per fortnight to allow pensioners an opportunity to increase overall income.

It is also proposed to be extended to include age pensioners who are self-employed. Any unused threshold in a fortnight can be rolled over to offset against higher amounts in future fortnights. This “income bank” is limited to $6,500.

———-

Example

Patrick receives the age pension and does occasional work. In the first fortnight in July 2019 he earns $250. This is exempt income and he can carry forward an amount of $50 to his income bank. In the next fortnight he earns $350. He uses the $50 in his income bank so that the whole amount is exempt income.

———-

Proposed commencement: 1 July 2019

Pooled lifetime income streams

The pension means test rules will be amended to encourage the development and take-up of pooled lifetime retirement income streams. These have sometimes been referred to as deferred or longevity income streams.

It is proposed to assess 60% of all pooled lifetime income stream payments as assessable income and 60% of the purchase price as an assessable asset until the client reaches age 84, or for a minimum of five years. The assessable ratios will then be reduced to 30% for the remainder of the client’s life.

These changes may encourage new product development and only apply to pooled income streams purchased from the commencement date. Any existing products will retain their current assessment.

Proposed commencement: 1 July 2019

Centrelink call centre

Anyone who has dealt with Centrelink will know the frustration of long call waiting times and computer system errors. The government aims to implement improvements through:

- An allocation of $50 million over 2018/19 to reduce call wait times

- Increased funding to improve computer systems.

Impacts for superannuation

There were no nasty surprises or tax increases for superannuation funds. Instead some measures aim to increase flexibility and help to reduce running costs.

More flexibility to contribute over age 65

Once a client reaches age 65 they need to meet a work test to continue making personal contributions into superannuation. This requires at least 40 hours of work in a consecutive 30-day period.

It is proposed that clients with total superannuation balances less than $300,000 will be able to make voluntary contributions for 12 months from the end of the financial year in which they last met the work test. The superannuation balance is measured on 1 July following the financial year in which they last worked.

This proposal allows retiring clients with lower superannuation balances the flexibility to organise their financial plans after finishing work. It allows both non-concessional and concessional contributions to be made, including any unused concessional cap rolled forward.

———-

Example

Oliver reaches age 65 on 3 May 2020. On 1 July 2020 his total superannuation balance is calculated at $260,000, allowing him to make voluntary contributions into superannuation during the 2020/21 financial year.

Assuming Oliver only had SG contributions of $18,000 made on his behalf in 2018/19 and $12,000 in 2019/20, he can make concessional contributions up to $45,000 in 2020/21. He can also contribute up to $100,000 in nonconcessional contributions.

———-

Client conversations

This measure creates opportunities for advisers to work with clients over age 65 who have recently retired to restructure investments and make contributions into superannuation.

———-

Proposed commencement: 1 July 2019

Protecting your super package

Concerns have been identified around fees eroding small superannuation balances. Four protection measures have been announced:

- Exit fees will be banned on superannuation funds

- Superannuation funds will not be able to charge passive fees of more than 3% on accounts with balances less than $6,000

- All inactive accounts with balances less than $6,000 will be transferred to the ATO. The ATO will increase data-matching activities to identify other active accounts held by the person.

- To avoid small superannuation balances being eroded by insurance premiums, if the account balance is less than $6,000 or contributions have not been received for at least 13 months and the account is inactive, or the member is under age 25, insurance cover will only be provided if the member opts-in to accept the cover, instead of being provided as a default option.

Proposed commencement: 1 July 2019

Notification of personal deductions

Clients wishing to claim a personal deduction for superannuation contributions should first submit a Notice of Intent (NOI) to the fund trustee and receive acknowledgement back. This ensures the fund trustee is appropriately deducting the 15% contributions tax.

It appears that some members are not following this process, so the ATO will introduce measures to improve integrity with new compliance measures.

Proposed commencement: 1 July 2018

Flexibility for SMSFs

Clients with self-managed superannuation funds (SMSFs) will be allowed to include up to six members in their fund. This may allow flexibility for families who want to include children and their spouses in the fund.

Even though SMSFs can currently have up to four members, most funds are one or two-member funds.

SMSFs that have a history of good record-keeping and compliance may only need to be audited requirements every three years instead of every year. This is proposed to apply to funds that have had three consecutive years of clear audit reports and have lodged annual returns within required deadlines.

Proposed commencement: 1 July 2019

SG opt-out

Clients with employment income above $263,157 could potentially receive superannuation guarantee (SG) contributions that exceed the concessional contribution cap of $25,000 per year.

If these clients have multiple employers they will be able to opt out of SG contributions from certain employers. This may allow the employees to instead negotiate a higher cash salary instead of an SG inclusive package.

Proposed commencement: 1 July 2018

Retirement income strategies

The SIS Act will be amended to introduce a retirement covenant that will require superannuation fund trustees to formulate a retirement income strategy for members to help members achieve their retirement income objectives.

Trustees will also be required to offer a Comprehensive Income Product for Retirement (CIPR) that provides income for life. This could form a combination of an account-based product and a deferred lifetime product. Clients will not be forced to commence a CIPR but it will offer them greater choice and flexibility.

A consultation paper will be issued shortly in relation to this measure.

In addition, the Corporations Act will be amended to introduce a requirement for income stream providers to report simplified, standardised metrics in product disclosure so clients can make more effective choices and comparisons.

Impacts for individual taxpayers

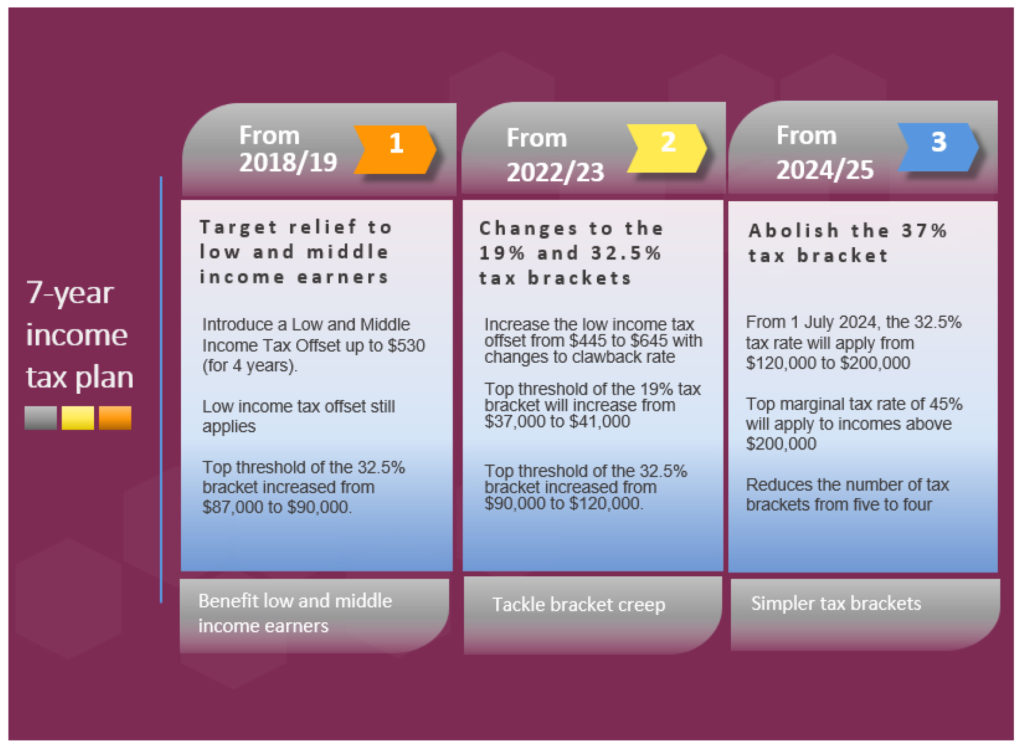

Reductions in personal income tax will be phased in over the next seven years with changes to tax brackets and introduction of a temporary new tax offset which is targeted directly at low to middle income earners.

In addition, the Medicare levy will be retained at the current rate of 2%.

The three phases of the proposed tax reforms are summarised in the diagram below.

Personal tax cuts

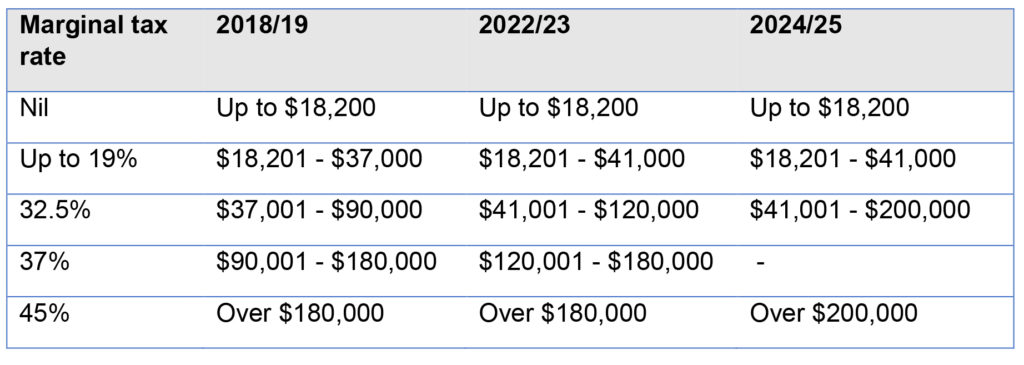

The marginal tax rates are proposed to change as follows:

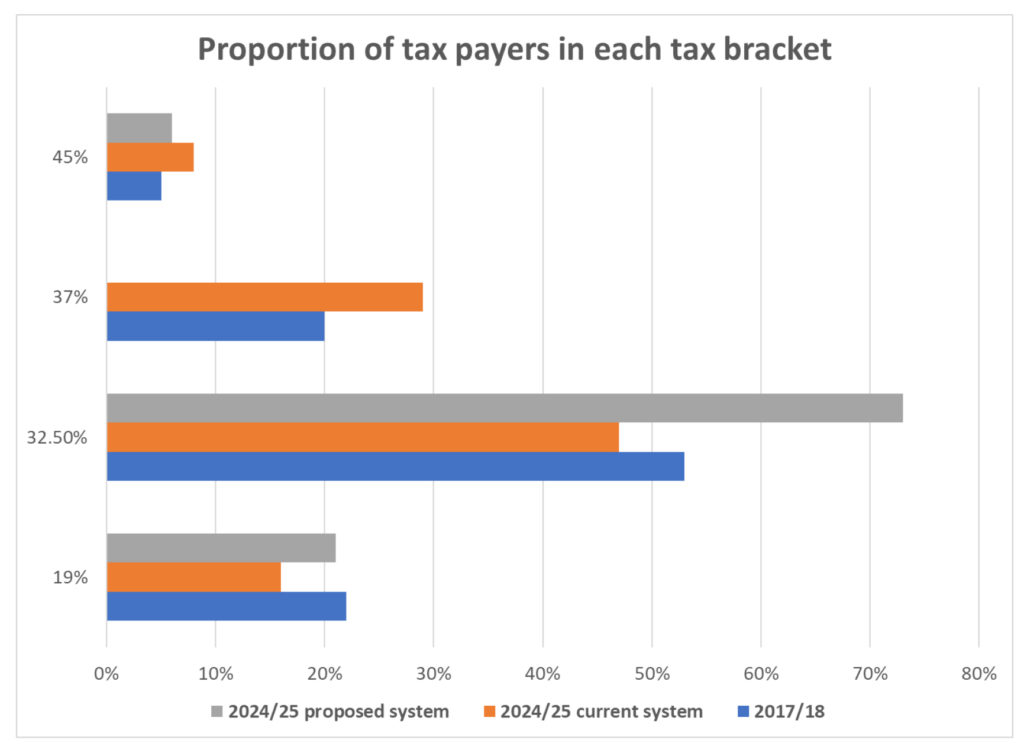

Under the proposed changes, the proportion of taxpayers in each marginal tax rate is shown in the graph below.

Client conversations

Lower tax rates result in clients having greater amounts of after-tax (disposable) income. Inflation is anticipated to remain at low levels and therefore the extra tax savings may provide a net benefit to clients, even after meeting higher costs of living.

The higher disposable income could be channelled into:

- Paying off non-deductible debt

- Saving regularly including increasing contributions to superannuation where possible. The cumulative effect of additional regular savings can translate to significant sums over the long term

- Additional savings to meet future aged care needs such as home care costs in the care years of retirement.

If possible, clients may wish to defer the realisation of income and capital gains to future years when their marginal tax rates are lower, to minimise tax payable. They may also wish to bring tax deductions forward to years before the changes take effect to maximise the value of the deductions.

Proposed commencement: From 1 July 2018, with introduction over 7 years.

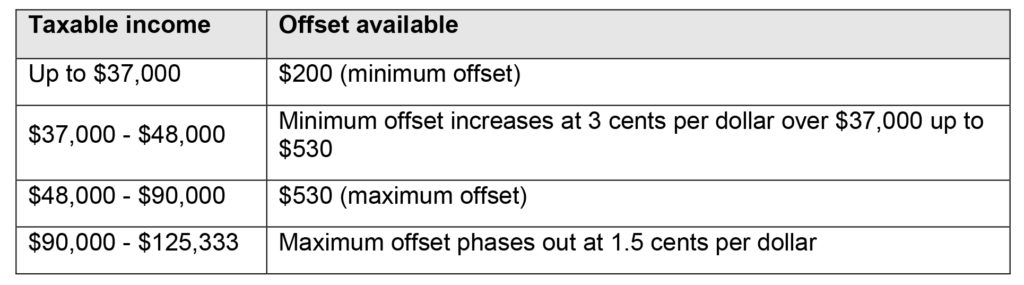

Low-income tax offsets

Tax savings will initially be targeted at clients on lower taxable incomes through the introduction of a Low and Middle-Income Tax Offset.

This offset will provide up to $530 as a lump sum on assessment after submitting the tax return. It is proposed to be available for the financial years from 1 July 2018 to 30 June 2022.

This offset applies in addition to the current low-income offset. The low-income offset is proposed to increase from $445 to $645 from 1 July 2022. The maximum offset applies on taxable incomes up to $37,000. It will phase out at the rate of 6.5 cents per dollar of income between $37,000 and $41,000. Then it phases out at the rate of 1.5 cents per dollar of income over $41,000 until it cuts out at $66,667.

Proposed commencement: Low & middle-income tax offset – 1 July 2018

Proposed commencement: Low income tax offset changes – 1 July 2022

Testamentary trusts

Minors who receive income from a testamentary trust are taxed at adult rates. A change is proposed to ensure the adult rates only apply to income that is directly from assets of the deceased estate and not from any other assets injected into the trust.

Proposed commencement: 1 July 2019

No tax deductions for vacant land

Tax deductions will not be able to be claimed for expenses relating to vacant land. These costs can be added to the cost base for CGT purposes. Proposed commencement: 1 July 2019

Small business deductions

A further extension is proposed to keep the immediate deductibility threshold at $20,000 until 30 June 2019. This measure will apply to businesses with aggregated annual turnover less than $10 million.

Impact for life’s luxuries … or vices

The rise of the illegal tobacco trade has been raised as a concern, and ATO powers will be increased to tax imported tobacco when it enters the country. This aims to minimise importers avoiding the tax.

Beer sold in kegs larger than 48 litres have been taxed at a lower rate than smaller kegs. This placed an unfair disadvantage on smaller craft beer brewers. The Budget included a proposal to tax all kegs larger than 8 litres at the same rate to create a more even playing field.

And for spirit drinkers, alcohol manufacturers can currently claim a refund on the excise they pay up to $30,000. This is proposed to increase to $100,000 from 1 July 2019.

Alcohol prices could come down, but for some smokers cheap tobacco may be harder to access.

Impact for the economy

The Australian economy has been growing for 27 consecutive years and this continued growth has not been derailed by the slowdown in the mining sector. Our economy has benefited from global growth that is tracking at the fastest pace in six years. Furthermore, business conditions are at the highest level since the global financial crisis.

Proposed tax relief for individuals have been announced to address the cost of living pressures, even though inflation in Australia has remained at historically low levels.

The improving economic conditions are expected to allow the budget deficit to be repaired more quickly than anticipated. The budget deficit is estimated to improve from 3.0 per cent of GDP in 2013‒14 to 0.8 per cent of GDP in 2018‒19, a fiscal consolidation of 2.2 percentage points. By 2026-27, the budget is expected to return to a surplus of just over 1 per cent of GDP.

Net debt as a share of GDP is expected to peak in 2017‒18 which is a year earlier than anticipated in the 2017‒18 mid-year economic forecast. Net debt as a share of the economy should decline over the medium term. By 2028‒29, net debt is projected to drop to 3.8 per cent of GDP.

Employment growth has been strong and consistent. Net jobs increased in the 16 consecutive months to January 2018, the longest positive run since official statistics began.

Consequently, the unemployment rate is projected to further decline and the tighter employment market is expected to feed into steadily higher wages growth.

The measures announced in the Budget including the $75 billion spend on infrastructure over 10-years, tax cuts that should feed into higher consumer spending and other spending measures are expected to see economic growth (as measured by real GDP) increase from 2.75% in 2017/18 to 3% in future years. Inflation (Consumer Price Index) is anticipated to move higher to 2.5% in 2019/20. Economic growth in Australia will continue its transition to broader based growth, moving away from its reliance on the mining investment boom.

This stronger economic outcome has enabled the Government to fund the proposed initiatives announced in the Budget.

By Louise Biti