New research highlights the serious unintended consequences of proposed reforms for young and active members

Damien Mu

AIA Australia has released new research to highlight the limited financial gains young Australians would receive under the Federal government’s ‘Protecting your Super Package’, which would also leave more than 1.4 million young people under 25 without much needed financial protections.

The research commissioned by AIA and completed by Rice Warner has shown that an opt-in insurance model for members under 25 would not address the unnecessary erosion of superannuation balances, with an individual’s retirement balance to increase by just $1,400 or 0.27 per cent over the course of their working life.

AIA considers this to be inadequate when considering that life insurance claims and benefit payments for under 25s are growing each year, and that the proposed reforms would be offset by the potentially devastating physical and social impacts a member would experience in the event of a serious injury or illness.

AIA Australia and New Zealand CEO, Damien Mu, said: “This data raises legitimate questions as to the value of such reforms, where members will forgo valuable protections for a minimal financial gain in retirement. The cost savings are inadequate when considering the increased health and financial risks for under 25s.

“There are unintended consequences to these measures, including that premiums for remaining insured members will increase across their working life.”

The Productivity Commission’s recent ‘Superannuation: Assessing Efficiency and Competitiveness’ report labelled duplicate accounts as a core driver of balance erosion and estimated that the annual cost of excess insurance premiums for members was $1.9 billion each year. AIA welcomes measures to address duplicate accounts and believes the government can achieve this through the measures outlined by the Insurance in Superannuation Working Group Voluntary Code of Practice.

“By adopting new measures on inactive accounts, the government will achieve two-thirds of its targeted cost savings for members, while addressing the important issue of duplicate accounts. This is what the government should be focused on, removing cover only in instances where insurance is not required,” Mr Mu said.

“They should not remove appropriate levels of protection or coverage for active, working Australians, nor should they discriminate against active members due to age or account balances, as these individuals are at risk, and they do have insurance needs as with other member cohorts.”

Members with active but low balance superannuation accounts do have insurance needs, with more than $75 million in claims paid by AIA to these members in 2017.

AIA has also paid $84 million on 1,200 claims for members under 25 since 2015, with the rate of Income Protection (IP) and Total and Permanent Disability (TPD) claims approximately the same for people aged 20 and those aged 30. Mental ill health is also the largest claim cause for under 25s at AIA for group TPD, representing one in four of all claims; and is the third largest claim cause for IP for under 25s.

“It is simply not the case that young people don’t require cover, or that they work exclusively in casual or part-time employment. More than 600,000 young workers under 25 do so on a full-time basis, which is 42 per cent of the under 25 working population. Of those, almost half are full-time workers in blue collar jobs.” Mr Mu said

“One of the more serious consequences of the proposed policy change is that people working in casual jobs and high-risk occupations such as mining and construction may be unable to attain life insurance, particularly for disability. This is because group insurance schemes were designed to accommodate a broad spectrum of risk across the nation’s policy holders, and a change to the default model would leave these members exposed where there is some form of underwriting.

More than 1.4 million young people under 25 would also be left without cover under the proposed reforms, while the opt-in rate is likely to be less than 10 per cent, even with extensive marketing campaigns.

“This is concerning as most young people are less likely to be able to self-fund in the event of a serious and unexpected event given that, for many, their largest asset is their future income,” Mr Mu said. “We also know that young Australians are less likely to actively opt-in to life insurance due to over optimism about their risk, and apathy – 40 per cent of young members are unaware what their superannuation balance is, let alone being in a position to consider their specific insurance needs and take active steps to opt-in.”

Implications for the Government and Australian economy

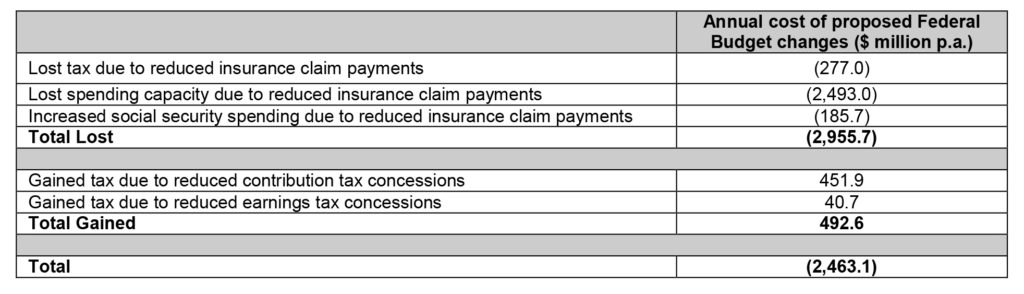

The Rice Warner research also shows that the impact of the ‘Protecting your Super Package’ for the government and Australian economy would be $2.46 billion annually, driven largely by lost economic spending due to reduced insurance payments. In assessing the isolated tax and social security implications, the research shows that the government would only benefit from a marginal gain of just $29.9 million in revenue each year.

“Before even considering the economic cost due to lower spending, the gain in government revenue is insufficient to rationalise the decision to remove insurance protections for young and active members,” Mr Mu said.