One of the benefits of an unconstrained fixed income fund is that it’s not tied to the duration of its benchmark index.

Brad Boyd, senior vice president with fixed income specialist Payden & Rygel, was in Australia recently and shared a range of insights with advisers around the country.

In this article, Grant Samuel Funds Management shares some of those insights; a retrospective look at bond markets and economies before the Global Financial Crisis (GFC), what’s happened in the ten years since those calamitous events and how to best position your clients’ bond portfolios in these uncertain times.

“Then as it was, then again it will be

And though the course may change sometimes

Rivers always reach the sea…”Led Zeppelin, 10 Years Gone

Ten years have gone since the GFC caused markets to plummet, companies to implode and investors left counting the cost. While it is more usual to quote an investment guru, the words of Led Zeppelin’s aptly named song summed up Brad Boyd’s thoughts about the GFC and the prospects of a similar cataclysm impacting markets in the future. People never really learn; instead, hubris and greed, fear and laziness can lead to bad decisions. In other words, risk in markets never disappears, it just changes shape; the lesson industry players learn is to shift that risk.

The GFC…a retrospective

With the benefit of hindsight, it’s easy to look back and understand how the GFC unfolded; however, it’s far more complex when living in real time. It was triggered, in part, by deregulation leading to lax lending standards; easy money resulted in bad loans, which in turn increased the likelihood that the individual, company or country was unable to repay it.

At the same time there was a dramatic rise in property values and new home sales in the US and other markets during the early 2000s (figure one); overvaluation, however, was just the tip of the iceberg. The combination of a loose regulatory environment and excessive leverage fuelled the highest property prices in the US residential housing market in history. This value declined nearly 50% following the GFC.

The overvaluation in property prices was evident with new home sales data, which nearly quadrupled from 1994 to 2005. This number declined by nearly 60% post-crisis, suggesting lending standards have tightened materially.

The US property bubble and loose regulatory environment led to an explosion of questionable loans. These sub-prime loans were packaged up by investment bankers to create ‘interesting’ securities; the sales message generally made claims suggesting the sum of the parts was less risky than the individual underlying loans – and unsuspecting institutions bought them up.

It’s easier to see the flaws in that premise in retrospect, however it does beg the question; has this behaviour been corrected or will another bubble precipitate another crisis?

Have the lessons been learned?

The market – and regulators – seem to have fixed the major issues highlighted by the GFC, issues such as loose regulatory environments, household leverage and easy lending standards.

There are however, some issues that remain outstanding:

1. Ratings agencies

Debt securities are rated by agencies, which collectively, got the credit crisis completely wrong. Post-GFC, 90% of instruments rated ‘investment grade’ before the GFC were re-rated as ‘junk’.

Although ratings agencies were penalised by regulators, and forced to separate their marketing and research divisions, there remains concern that the models used today remain unchanged from those used ten years ago and, despite the increased complexity of some financial products, there has been a resurgence in using over-simplified models.

2. The return of the VaR

Prior to the GFC, banks measured downside risk through a single statistical measure, the ‘value at risk’ (VaR) number. It is used to assess the level of risk associated with a portfolio or company, and can oversimplify complex financial instruments.

The VaR is solely reliant on history and is not forward looking; it was certainly not predictive of an event such as the GFC. Of concern is that some in the industry are starting to rely on it again today to measure forward-looking risk – and unlike financial product performance, it does not come with a regulator prescribed ‘health’ warning.

3. Central bank debt

Historically, risk has tended to shift from one area to another. A clear example of this is illustrated in figure two, which looks at the balance sheet of central banks. To prevent a potential liquidity crisis being precipitated by the GFC, central banks globally stepped in and bought billions of dollars’ worth of debt, default mortgages, credit, and in some cases (such as the Bank of Japan), equities. Although it’s starting to shrink, central bank balance sheets still hold significant assets which will, over time, need to be sold off. Will there be a market for this?

Global economic outlook

Despite recent headlines, market gyrations and a flattening of the yield curve, Payden has a positive outlook for the global economy. This is based on three key measures – GDP growth (figure three), employment growth and low inflation. Unemployment rates have a downward trajectory, which means people are working and there are signs of wage growth.

Some suggest the flattening of the yield curve is a red flag signalling recession. While a flattening yield curve has preceded recessions, recession generally does not occur until the yield curve inverts. Indeed, there have been long periods of growth when curves are flat. Given the US Federal Reserve is expected to raise rates once more in 2018 and three times in 2019, the yield curve is more likely to steepen in line with those rate increases.

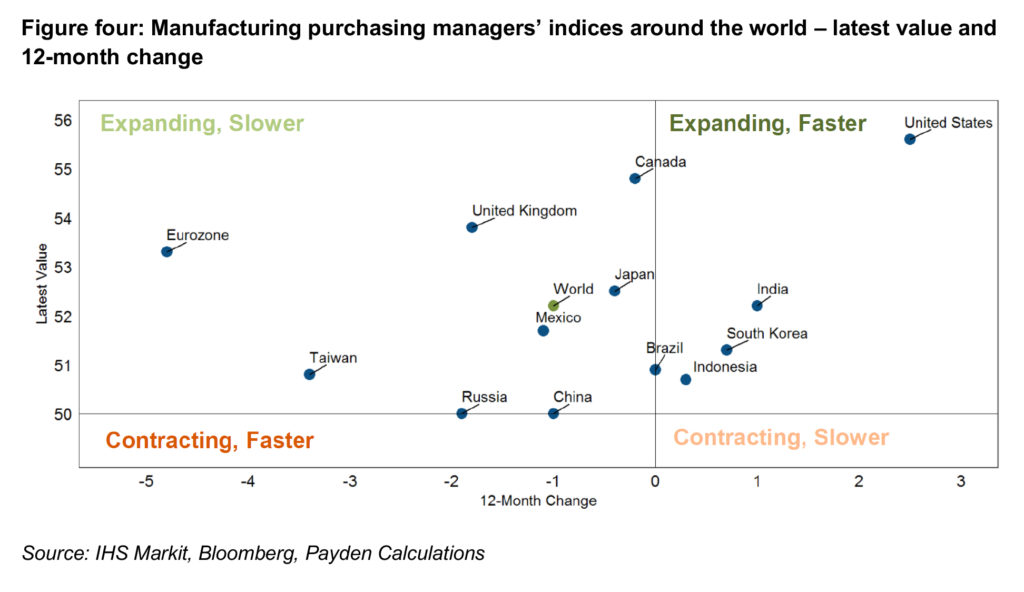

The monthly Purchasing Managers’ Indices (PMIs) for the manufacturing sector is also a useful gauge for the health of the global economy in near real-time. Index values range from 0 to 100; above 50 indicates expansion, below 50 indicates contraction.

As of September 2018, the US has diverged from the rest of the world, accelerating even as global data has decelerated. The overall global index continued to show slower growth but remains in expansionary territory at 52.2 and has been above 50 for 31 consecutive months (figure four).

These indicators are heading in the right direction and support the argument for a positive economic outlook.

Bond indices and strategies

1. Benchmark driven strategies

A market cap weighted index is an interesting snapshot of the bond market, but from an investor’s perspective, does it make sense to use a strategy that replicates the index? Or to look at this another way, why would an investor lend money (remember, if you buy bonds you are lending money) to the most indebted countries and companies?

Instead, investors should be after those issuers with the least amount of debt, less likely to default.

There’s some logic behind a passive equity investment – as stocks grow, so too does the index. It’s reflective of the broad economy and rises in line with a successful economy, capturing the footprint of successful industries and companies.

In the case of bonds, a market cap weighted index does not follow the same logic…why would you weight an index towards those with the most debt, particularly if the intent is to mirror or invest in that index?

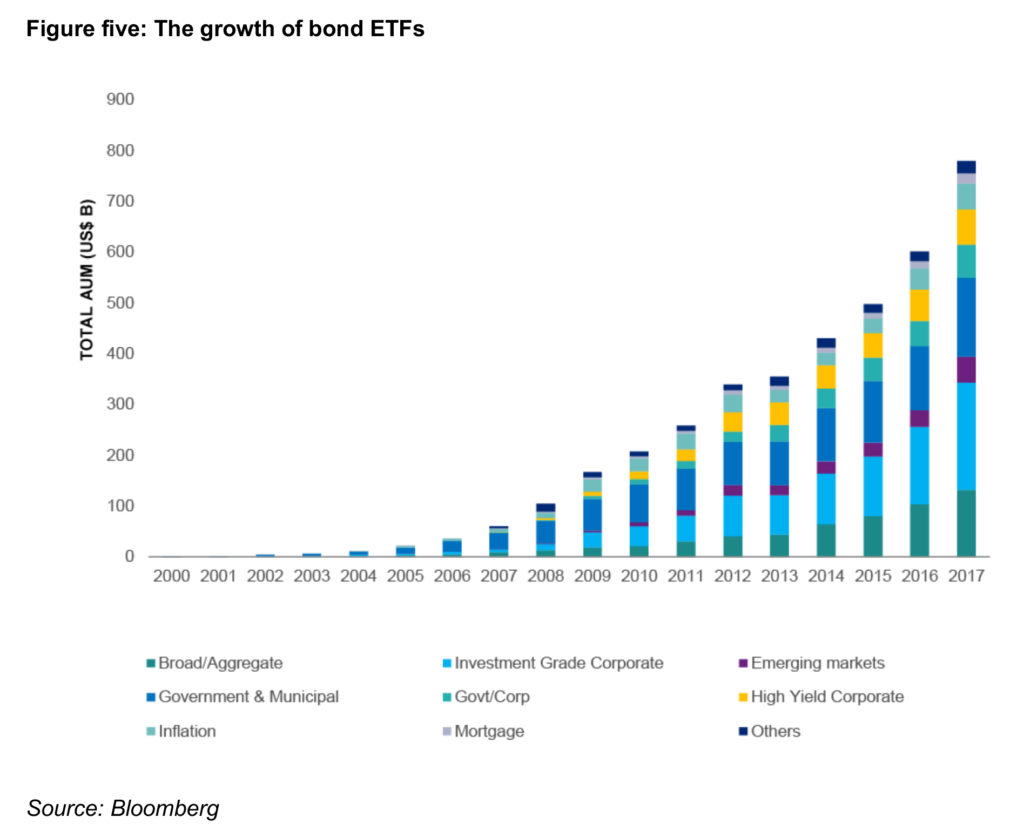

Despite this, there has been exponential growth in the use of bond ETFs around the world. By definition, those replicating a bond index are capturing the largest issuers of debt.

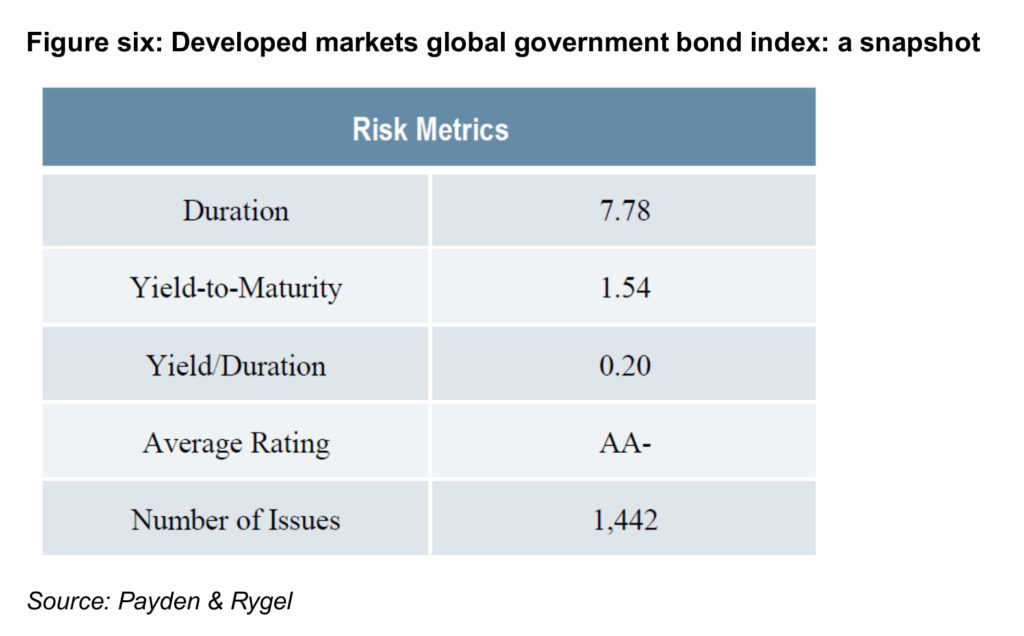

To illustrate, figure six considers the composition of the developed markets global government bond index:

- Duration (or sensitivity to interest rates) of 7.78 years…why would investors want that much interest rate sensitivity and potential volatility in their portfolio?

- This duration is being taken on with a yield to maturity near record lows

- Yield divided by duration is a measure of interest rate sensitivity – figure six shows that if yields move 20 basis points (bps) higher, investors would wipe out their income; this is a historically thin margin and not a good scenario where interest rates are more likely to move upward, and bond yields increase. By way of comparison, back in the 1990s, it would take a move of 200bps before an investor was taking on losses on a bond investment.

Any strategy that mimics an index will share the characteristics of that index. In an environment with rising bond yields, volatility and a degree of geopolitical and interest rate uncertainty, traditional benchmark-based approaches to fixed income investment may be less effective.

2. Unconstrained investment strategies

An unconstrained investment strategy is one that is not beholden to a benchmark; rather it is designed to be better able to navigate the complexities of the evolving fixed income landscape than traditional benchmark aware bond funds.

Unconstrained strategies are typically managed to beat a cash or equivalent benchmark, rather than a bond index; this removes constraints around duration and sector positioning.

This results in a fund that has the flexibility to dynamically alter its investment mix to find the best opportunities across securities, duration and geography.

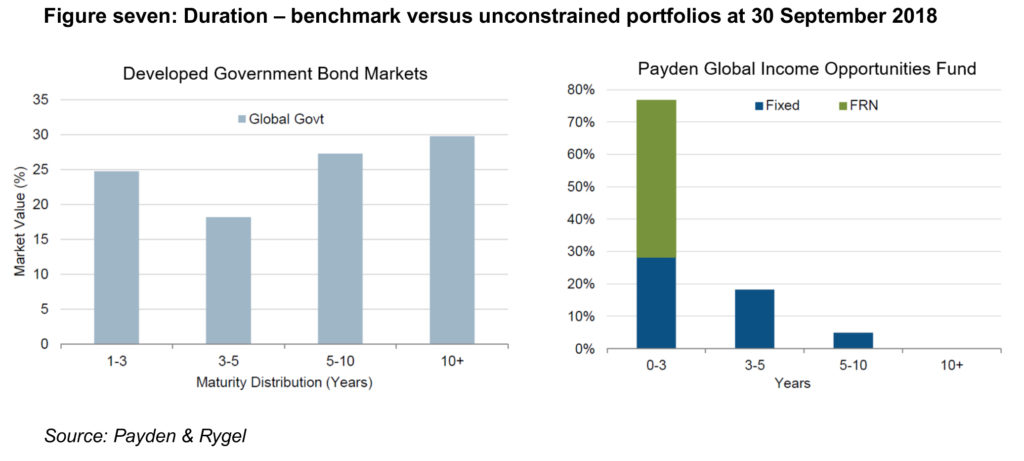

One of the benefits of an unconstrained fixed income fund is that it’s not tied to the duration of its benchmark index. In the current environment, Payden has elected to have the bulk of the Payden Global Income Opportunities Fund’s assets in shorter duration; as illustrated in figure seven, nearly 80 percent of the Fund’s securities have a duration three years or less in total, with approximately five percent of the portfolio in securities with a duration of five years or more. Compare that to developed government bond markets, where 30 percent of securities have a duration of 10 years or more and more than 50 percent have a duration of five years or more.

While the global economic outlook looks positive, it won’t be without its challenges. Both equity and fixed income markets will be tested, so it makes sense to take stock of the investments in your clients’ portfolios and ensure they are best positioned to deliver positive returns in a challenging investment environment.

———