For the past 17 years we have produced “The Big Issues” report – a report that has sought to highlight the issues that are expected to influence the economy over the forthcoming 12 months.

For the past 17 years we have produced “The Big Issues” report – a report that has sought to highlight the issues that are expected to influence the economy over the forthcoming 12 months.- Now this is no crystal ball gazing exercise. The aim is not just to forecast where certain economic variables are likely to be in a year’s time. Rather the focus has been to highlight trends, issues and ‘big picture’ influences that act as threats or opportunities for consumers, investors and businesses alike.

- The aim has been to produce a highly readable, relatively jargon-free document. Probably today we could call this a blog. But the intention over time has been to produce commentary that causes people to think and ask the ‘so what’ question – that is, to determine what this means for their own circumstances.

- And we undertake this analysis by providing a healthy amount of graphs and pictures in addition to the text to best highlight the issues we think will prove important in 2019. Certainly one of the great innovations over recent years has been the infographic and other developments that have sought to bring subject matter ‘alive’. They say that a picture should tell a thousand words, and that should be the basis for all economic and financial commentaries – make the subject matter more alive and relevant to readers. The real value of economics is when people say ‘so what?’ and relate the commentary and forecasts to their own situation.

…But first…The economic ‘state of play’

Review of the past year

- In addition to our ‘Big Picture’ analysis of key economic issues we feature a recap of the past year’s economic performance together with an outlook for the economy for the coming twelve months.

- This economic assessment largely sets the scene for the discussion of the Big Issues. Because there are themes and trends that have evolved over the past year or years to affect economic performance. And clearly each one of us wants to know whether the same factors or indeed new factors are likely to dominate in the coming year.

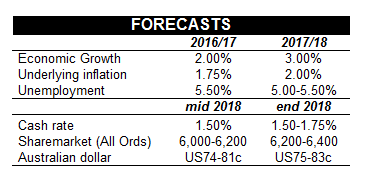

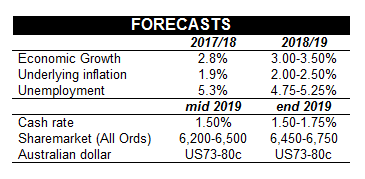

- And for the second straight year the economy has played out generally as expected. Economic growth was 2.8 per cent in 2017/18 and annual growth is currently 3.4 per cent. Inflation stands near 2 per cent, in fact underlying inflation is closer to 1.75%. Unemployment stood at 5 per cent in October (and finished 2017/18 at 5.3 per cent).

- On interest rates, last year we said: “the cash rate may remain at 1.50 per cent for most of the year.” While we had pencilled in a possible rate hike in December 2018, clearly that was premature.

- While the economy has played out largely as expected, the sharemarket and currency have not. The picture was more positive around mid-year, but both the Aussie dollar and sharemarket are ending 2018 weaker than expected. Uncertainty about future global economic prospects has white-anted the sharemarket – both here and abroad. And the combination of higher US interest rates and stable domestic interest rates have served to restrain the value of the Aussie dollar compared with the US dollar.

The year ahead

- Prospects for the Australian economy remain good. The Reserve Bank recently said that GDP growth would be around 3½ per cent on average in 2018 and 2019. And we wouldn’t greatly disagree with the forecasts.

- Aussie consumers are spending, underpinned by lower prices and a strong job market. Consumer confidence is above longer-term averages (or ‘normal’ levels’). Household consumption is growing close to 3 per cent – near the strongest annual rate in six years.

- Overseas buyers continue to embrace our high quality mining and consumer goods while tourists and students flock ‘Down Under’.

- As a result, business conditions and confidence are generally seen as good. Consumers are spending and profits are rising.

- Businesses are also ploughing back money into their operations and are investing. Similarly, state and federal governments are actively spending on infrastructure. Transport infrastructure dominates, but the firm population growth rates across the country are necessitating more social infrastructure such as schools and hospitals.

- Inflation and wage growth are lifting. In fact there is more evidence of labour shortages and higher wages, especially in the mining sector. Trends in these areas will prove pivotal to whether the Reserve Bank begins ‘normalisation’ – starts to lifts rates later in 2019.

- In terms of the Aussie dollar, we think the US Federal Reserve is getting closer to pausing in the rate hiking cycle. At the same time, higher wages are the pre-requisite to higher rates in Australia. US-China trade discussions will also determine where the Aussie is headed. That said, China is already actively stimulating its economy. This time next year, the Aussie is seen closer to US75 cents.

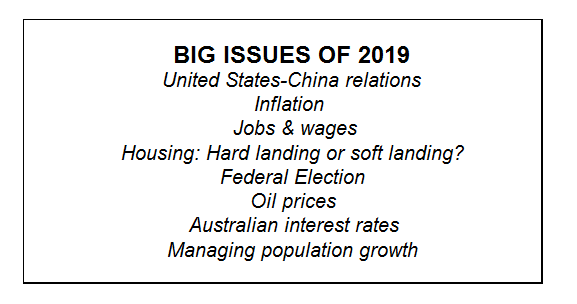

United States-China relations

- At the time of writing, there is greater optimism that a trade deal can be secured between China and the United States. In fact the White House reported that the US and Chinese leaders concluded a “highly successful meeting” between themselves and their most senior representatives” on the sidelines of the Group of 20 (G20 meeting) in Buenos Aires, Argentina.

- “President Trump and President Xi have agreed to immediately begin negotiations on structural changes with respect to forced technology transfer, intellectual property protection, non-tariff barriers, cyber intrusions and cyber theft, services and agriculture. Both parties agree that they will endeavour to have this transaction completed within the next 90 days. If at the end of this period of time, the parties are unable to reach an agreement, the 10 per cent tariffs will be raised to 25 per cent”

- Significant hurdles lay ahead, especially to achieve agreement in 90 days. But if a trade deal is indeed hammered out, will that mean that we can remove this Big Issue from the 2019 list? The answer is no. It is not just trade issues that dominate the relationship between the two super powers. Effectively the two nations are vying for the position of the major super power and this involves issues such as regional defence, especially in the Pacific Rim. Leaders of the US, Japan and India met on the sidelines of the G20 summit to emphasise the importance of a ‘free and open Indo-Pacific’

- Australia’s Prime Minister, Scott Morrison, believes he can work with both powers but understandably tensions will emerge. China is Australia’s largest trading partner. And the United States and Australia maintain a historically close relationship on regional security

- In economic terms, China is drawing close to the number one spot, if economic size is determined by gross domestic product. By 2023 China’s economy is expected to be almost US$20 trillion with the US at almost US$25 trillion. On purchasing power parity though China actually passed the US in 2014 and currently accounts for 18.7 per cent of the world economy with the US at 15.2 per cent

- But economic dominance involves more than just the size of the economy. China is the world’s largest trading nation and its contribution to world economic growth has consistently been close to 30 per cent in recent years, far bigger than any other nation.

Inflation

- Inflation has featured in our Big Issues reports for a number of years. Last year we asked: “How long will inflation stay low?” The previous year was: “Is inflation at an inflexion point? Again in Big Issues 2017 we asked: ‘Will we need to worry about inflation again?’ In 2014 we posed the question ‘Is Inflation dead?’ And in the 2013 edition of Big Issues we questioned: “Inflation or Deflation?”

- This year again inflation features as a Big Issue, but we have left the topic open-ended. We suspect that it will be a ‘much-focused-on’ and ‘much-talked-about’ issue but there will be a number of facets.

- In some countries we suspect that inflation will start to lift. In fact in many developing nations, inflation has already started lifting with key catalysts being the strong US dollar, rising import prices and higher wages. In other countries – such as Australia – inflation appears cemented at low levels, even with weak local currencies. A key reason being global competition. Consumers face an explosion of choices on where they fulfil their needs. And business has more choices on where work tasks are completed or how they source supplies.

- Eventually consumers and business will adjust to these relatively new circumstances. Arguably the choice provided by technology and globalisation, including disruption, is only a few years old.

- Central banks also have to work through the issues from a monetary policy perspective. The banks must decide whether the new ‘global choice’ is likely to become mainstream. If they conclude ‘yes’, that consumers and businesses have adapted to new circumstances, then it won’t require any adjustment of inflation targets.

- The Reserve Bank has been reluctant to tinker with the 2-3 per cent inflation target. However, the Bank of Canada is conducting a review of monetary policy, in what it describes as “a thorough review of the alternatives.” And the US Federal Reserve has continued to lift interest rates despite inflation refusing to budge from levels near 2 per cent. Indeed, the US Federal Reserve must decide in 2019 when to pause in its rate-hiking efforts – an issue that could represent a Big Issue in its own right

Jobs and wages

- In the Big Issues report for 2018, we included the issue: “The disconnect between jobs and wages”. This year, just like what we have done with the issue of inflation, we have again simplified the discussion to Jobs and wages.

- Like inflation, we expect that the discussion on jobs and wages will be somewhat multi-faceted. It won’t just be discussion of why tighter job markets are not seemingly translating to higher wages.

- For instance, some have questioned whether one of the changes wrought from technology/globalisation is new levels of ‘full employment’. And by “full employment”, we mean the lift-off point for wages, usually described as NAIRU – the Non-Accelerating Inflation Rate of Unemployment.

- The NAIRU theory suggests there is some mystical jobless rate, and once you fall below that rate businesses must bid more aggressively for the available workers in the economy.

- Many advanced economies are experiencing historically-low jobless rates without a solid lift in wages. Even in Australia, the Reserve Bank had generally been working on a ‘full employment’ rate of 5 per cent. But the Reserve Bank Governor recently suggested that the unemployment rate could hit 4.5 per cent without prompting the upsurge in wages that may have been witnessed in the past.

- One reason could be the ‘release valve’ of foreign workers. If a business can’t find the necessary workers in the local market, it may seek to fill the positions from overseas. And if there was some government restriction on ‘importing’ the labour, the business may find other ways of getting the work done – such as out-sourcing to overseas contractors or employing staff who work remotely, such as overseas.

- Wage-price relativities, productivity-driven wage increases, the growth of non-cash remuneration sources and new preferences for a great workplace instead of a high-paying job may also be issues or questions in focus

Housing: hard or soft landing?

- Is this issue sufficiently worthy as to be included in the 2019 report? Admittedly, it is the fourth straight year that this Housing topic has been included in the year’s Big Issues. But ultimately, it gets down to the question of whether you think this will be a keenly debated issue again in 2019. And we think the answer will indeed be ‘yes’

- Sydney and Melbourne home prices are lower than a year ago in an aggregate sense. Sydney prices are down around eight per cent from highs after previously lifting around 75 per cent since 2012. Similarly Melbourne home prices have eased six per cent from record highs after lifting 58 per cent in a five year period.

- Sydney and Melbourne are exceptions to the rule. Home prices in other markets didn’t rise anywhere near the same extent and therefore are not falling to the same extent. In fact, prices are rising, certainly in Canberra, Adelaide, Brisbane and Hobart as well as a raft of regional cities.

- Sydney and Melbourne prices rose in response to strong migration and therefore demand by owner-occupiers. The strong price growth encouraged interest from investors, prompting regulators to introduce measures to address the excess property demand.

- With investor demand retreating and more choice on offer for owner-occupiers given the lift in the number of completed new homes, home prices have predictably softened to more sustainable levels.

- Sydney and Melbourne are two housing markets rather than being the Australian housing market. Prices are adjusting to more balanced supply-demand fundamentals. Annual price falls of around 10 per cent are possible in Sydney and Melbourne as the excess price premium with other markets erodes.

- It is important to note that Sydney and Melbourne home prices are adjusting in response a rebalancing of supply-demand fundamentals and not because the job market is softening or interest rates are rising. In fact trend unemployment rates in the two cities are at decade lows. Further, cash rates are not expected to change until later in 2019 at the earliest.

Federal election

- Election year is fast approaching. So it is understandable that this event or ‘issue’ joins with the other Big Issues to be debated over 2019.

- Now the inclusion of the Federal Election amongst the Big Issues may be debated by some. And that is largely due to the timing. It is true that the election will probably be done and dusted by May. But arguably the final results in some seats will take a little longer to come through. Then the new government may decide on handing down a mini Budget (the Federal Budget is delivered early on April 2).

- And then there is the implementation of the new policies – especially given that current opinion polling suggests there is a high chance of a change of government.

- If the current government wants to hold an election for the House of Representatives and half of the Senate, then the poll must be held by May 18, 2019. Conceivably the government could elect to delay the holding of the election of the House of Representatives and Territory Senators until November 2, 2019. But this would involve extra expense. Not to mention the relative inconvenience on Australia voters – especially given that voting is compulsory.

- At this relatively early stage we can already identify a number of issues that are likely to feature in the Federal Election. The Labor Opposition have indicated that it wants to make changes to eligibility and tax status of franking credits. Further, Labor are proposing changes to negative gearing.

- Differing approaches to Energy policy will also be keenly debated. And there could be different approaches advocated on population policy.

- It is hoped that the Liberal/National Coalition and Labor parties will engage in serious discussion over true taxation reform, rather than just arguments on relative tax scales for different sized businesses and individual taxpayers. The International Monetary Fund has recently indicated that there is need for a better balanced system of direct and indirect taxation.

Oil prices

- One issue that tends to regularly feature in discussion on financial markets is oil prices. In many respects this reflects the myriad of influences that affect the price of oil. In turn, the changes in oil prices have broader implications across countries and industries and knock-on effects for consumers and a raft of other businesses.

- So in some respects, the inclusion of Oil Prices in the list of Big Issues is to incorporate a number of other and different issues. For instance, over 2018, some of the influences on oil prices have included sanctions on Iran; the slowdown of the Chinese economy; instability and production disruptions in developing oil producing nations like Venezuela; US-Russian relations; US-Saudi Arabian relations; take-up rate of electric vehicles; disruption such as ride-sharing and taxi-type services; and changes in economic growth rates for major economies.

- US Nymex crude began the year around US$60 a barrel. Over the first quarter, crude prices were relatively settled, broadly holding US$60-65 a barrel. But prices motored to US$74 in the second quarter and to near 4-year highs in early October. Predictions of US$100 began to abound. And soaring petrol prices featured in the media, both here and abroad.

- But since early October, crude oil prices have slumped by more than a third. Now there are more predictions for crude at US$40 a barrel rather than US$100 a barrel. The ‘sweet spot’ for crude oil is probably near US$60 a barrel – a level that consumers and producers can live with. But getting to that price level and holding that level involve the interactions of a range of economic, political and weather-driven factors. OPEC and its allies meet in Vienna on December 6 where it is expected that production will be cut by 1-1.5 million barrels a day. However, bottlenecks in the Permian Basin have receded and US supply is expected to be boosted, potentially countering Saudi-led efforts to stabilise the oil market.

Australian interest rates

- This could be the most controversial entry to the Big Issues list for 2019. The Reserve Bank hasn’t changed the cash rate for 27 consecutive months. The last move was a rate cut in August 2016, with the Reserve Bank cutting the cash rate from 1.75 per cent to a record low – an emergency level – of 1.50 per cent.

- The Reserve Bank hasn’t changed rates in over two years. And some economists, armed with extraordinary binoculars, don’t see a rate change before 2020 or 2021. So why do we think interest rates could be much debated in 2019?

- One reason is that some economists are questioning the value of leaving rates steady. If inflation is not a risk, they argue, and the Reserve Bank is keen to see a lift in wages, why not cut the cash rate?

- That is clearly an out-of-consensus call. But what if the global economy was to soften, especially China. And what if the falls in Sydney and Melbourne home prices had the effect of weakening consumer sentiment and spending. Clearly if either or both were to occur then the calls for lower rates would get louder.

- Of course the Reserve Bank Board currently believe that the next move in interest rates is more likely to be up, not down. Other countries are normalising monetary policy with similar growth and inflation rates as Australia. So circumstances would certainly need to change markedly for the Board to start altering its view. The Reserve Bank also would need to fundamentally re-assess its underlying assumptions about how the economy operates.

- There also may be another alternate set of circumstances that prompts debate on interest rates, For instance, the jobless rate continues to fall sharply, perhaps hitting 4.5 per cent or lower. In addition, there are more anecdotes of higher wages being paid. Being forward-looking, the Reserve Bank may start entertaining thoughts of lifting interest rates to pre-empt higher wages being passed on in terms of higher prices.

- If at the same time Sydney and Melbourne home prices continued to fall, a decision to lift interest rates would prove to be somewhat controversial.

Managing population growth

- Australia maintains one of the fastest growing population growth rates in the world. And certainly one of the fastest growth rates of advanced economies. In the year to March (latest data), Australia’s population was up by 1.6 per cent on the previous year.

- Population growth hasn’t deviated too much over the past seven years with the annual rate broadly holding between 1.4-1.8 per cent. However population growth is still lower than the near 40-year high of 2.2 per cent set in the resource boom high of 2008.

- It is important to note that Australia’s relatively fast rate of population growth is no accident. Federal Treasury has maintained a ‘PPP policy’ over the past decade in an attempt to address the challenges of an ageing population on the economy, more broadly, and specifically on the Budget

- In practice this has meant putting in place policies and initiatives designed to achieve higher productivity growth; higher workforce participation; and higher population growth.

- The PPP policy has been quietly carried out, but has been amazingly successful over time. Australia has been successful at maintaining a faster economic growth rate than other advanced economies and avoiding recession for 27 years – the longest expansion by a major world economy in the modern era.

- On a number of occasions, population growth was supported by schemes like the ‘baby’ bonus. But the general aim has been to import workers in specific sectors and professions to address skill shortages. The workers coming to Australia in their 20s and 30s have slowed the rate that the economy has been ageing. Migrants have also contributed to spending and tax collections from day 1 of their arrival. In most cases they are highly skilled and more educated than Australian-born workers.

- State and Federal governments are now questioning the speed of Australia’s population growth with some advocating a slower rate of growth for a period of time to allow social and economic infrastructure to ‘catch up’.

- With the Federal Election due in 2019, there will be plenty of contributions to the debate on how to manage population growth and therefore manage prosperity.

Rewind: The big issues for 2018

- As we noted at the start of this report, we have been producing the Big Issues report for the past 17 years. It is interesting – and perhaps even instructive – to rewind over the past year and assess what we had on the radar in December 2017.

- Looking ahead into 2018, we highlighted eight issues. And the first issue was “President Donald Trump”. This was the second year in a row that we had Donald Trump on the Big Issues list. But it turns out that the decision was vindicated. There was the trade deal with Canada and Mexico, the on-going trade stoush with China, President Trump’s influence on the oil market with trade sanctions on Iran and also the President’s comments on interest rate policy conducted by the Federal Reserve. President Trump moved markets.

- We also continued to pose the question: “How long will inflation stay low?” And clearly the question wasn’t answered. Despite robust growth across advanced nations and low jobless rates, inflation has remained stubbornly low.

- Number three on the Big Issues list for 2018 was: “The disconnect between jobs and wages”. And what an issue this turned out to be – both at home and abroad. In fact the Reserve Bank Governor focussed on the issue in his last speech. The Reserve Bank thinking now is that even a jobless rate of 4.5 per cent won’t spark a major lift in wage growth. In large part globalisation and technology have served to lift supply. That is, how and where spending occurs and how and where work is done.

- Housing has also dominated our ‘Big List’ for a few years. And with good reason. Home prices rose sharply in cities like Sydney and Melbourne in 2015 and 2016. And then prices began to correct from later in 2017 and through 2018. In both 2017 and 2018 we featured the question: “Housing: Hard landing or soft landing?” There are plenty of views out there and they certainly attracted numerous column-inches in the media over 2018.

- A new Big Issue was introduced onto the scene in 2018: “Infrastructure”. The federal government, along with every state and territory government were keen to show how much they were willing to spend – especially on key transport initiatives like roads, tunnels, railways and airports. Certainly the spending is necessary to meet the demands of our growing population. But there was also solid debate about the relative worthiness of projects. Economics as well as politics featured in the discussion

- Issue 6 for 2018 was “The economic benefit of lower taxes”. The Government found it hard to win this battle. Seemingly some in the community believe that every business must react the same way to a tax cut.

- Also on the list of Big Issues for 2018 was “Power prices and availability”. In truth, it didn’t turn out to be a regularly debated topic. Rather it appeared for a period of time only to disappear and reappear at various points in time. State and Federal Governments continue to disagree on energy policy.

- China is never too far away from our consciousness. And the issue we nominated as a Big Issue for 2018 was “The ‘slowdown’ of the Chinese economy”. This issue was very much in focus over the second half of 2018 in light of the ‘tit-for-tat’ trade dispute between China and the US. The Chinese economy has indeed slowed, necessitating stimulus measures from the Chinese leadership. Given that China accounts for around a third of global growth and the country is Australia’s major trading partner, clearly the issue deserves close monitoring.