Michael Price

Income is traditionally associated with term deposits and fixed income among more defensive assets, and with real estate and the traditional concept of high

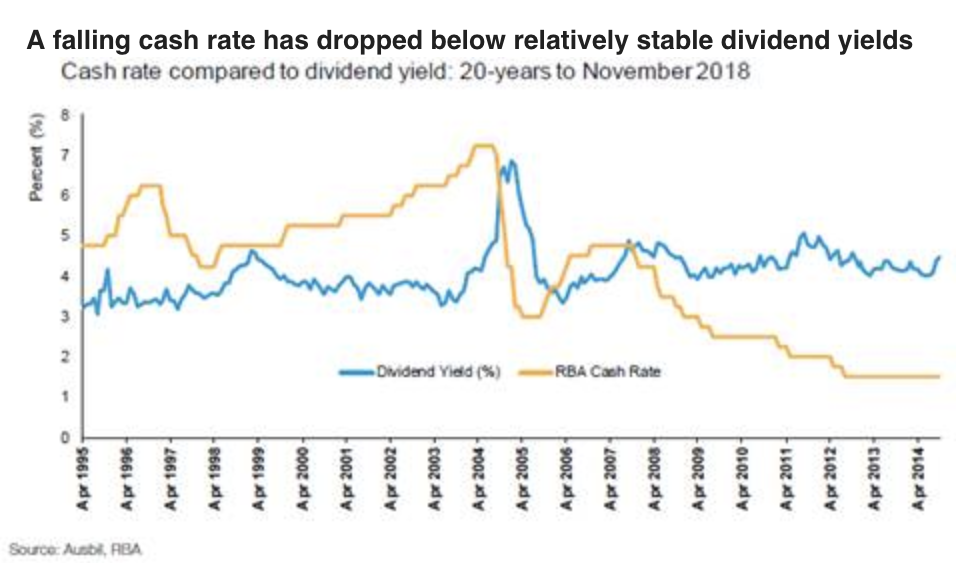

dividend shares among growth assets. In the last 20-years, there has been a fundamental change in the relationship between dividend yields and the cash rate, a proxy for short-term deposit rates (as shown below). The secular fall in interest rates has seen them drop well below the relatively more consistent level of dividend yield.

This differential has become quite significant such that dividend yields currently stand at around 4.4% a year against a cash rate of 1.5% pa. For comparison, over the last 20 years the average equity dividend yield has been around 4.09% (with a standard deviation of 0.60%), compared to the average official cash rate of 4.14% (with a standard deviation of 1.65%). This suggests that over this period, dividend yields have been less dispersed than the cash rate. Or in other words, the relative long-term stability of diversified Australian dividend yields are less variable over time than income derived from assets relate to cash rates.

Drawing dividend income from an actively managed equity portfolio offers the benefits of both income and growth, but with broader diversification for stability and growth, and the potential for active approaches to enhance income.

Regular equity income can help with risks faced by retirees

Investors in the later stages of their accumulation phase, approaching retirement, and in retirement can benefit from the use of equities as part of their overall income plan. At this stage, investors face two major risks that impact how much they have to fund retirement, and how long this will last: longevity risk, and the risk of inflation over time.

In simple terms, longevity risk is the risk of outliving your money. Australian life expectancy has been steadily increasing. According to the ABS, Australian women have a life expectancy of 84.6 years of age (compared to just 50.8 years in 1890), Australian men a life expectancy of 80.5 years (compared to just 47.2 years in 1890). Just in the last 10-years, female life expectancy has risen by 1.5

years, and male by 0.9 years.1 Figure 3 illustrates the gains in life expectancy for men and women since 1890, illustrating a steady trend that is still rising. On reaching retirement at the age of 65, the likelihood of survival for Australian couples is high (where at least one is alive), with 90% expected to reach the age of 85, 50% to reach the age of 93, and 10% who will attain the age of 99 years.

With the population living longer, on average, to ages well in advance of the retirement age of 65-67 years, there is a commensurate increase in demand for income and growth. Older Australians need higher incomes to replace earnings forgone in retirement, a growing income stream to mitigate against rising living costs, income that will last with minimum capital drawdown, income that is reliable and regular, and income that makes the most of existing tax rules.

Essentially, investors increasingly need income to live off, without necessarily having to eat into capital. Equities are beneficial in the capital growth they can achieve over the long term, helping replenish capital for the much longer journey investors are experiencing in retirement.

A second risk investors should consider is the impact of inflation on the purchasing power of their money. Investment returns do not account for inflation. If you earn 10% from an investment, and inflation (the price of things) rises by 3%, then you actually only have 7% in real spending power (without accounting for any taxes for illustrative purposes).

Equities, being businesses, can typically adjust for inflation within their business models by changing their prices. Moreover, over the long term, equities typically provide a higher level of return that can help offset the long-term detrimental wealth impact of inflation.

Why does active dividend income investing work?

An active dividend investment approach can add value to a portfolio, and generate outperformance, through focusing on quality companies with strong dividends and dividend growth, companies with sustainable earnings growth, maximising the benefits available through the tax and imputation system, and tactical allocation to capture a greater share of dividend income.

Markets are efficient, but not perfect. The first and most fundamental reason that an active approach to income investing works is the fact that the market is relatively inefficient, particularly in the short term.

Chasing dividend yield, alone does not maximise returns

The assumption that many income investors make regarding dividend yields is that the relationship of current dividend yield to future earnings growth is linear, that is, the higher the dividend yield, the higher the future earnings growth from which dividends are paid. This assumption does not actually hold in the market.

On average, the top dividend yield companies actually see low, or even negative, earnings growth going forward compared to the 4th to 7th decile of companies. This has been true for the last 20 years.

An active approach does more than simply chase yield, as would a passive approach to yield. An active dividend income strategy can increase income from companies whose dividends are healthy, but maybe not the highest, because they are also investing earnings into a growing business, hence their better earnings growth in the year ahead.

Also, the highest yielding stocks are more volatile. Top decile dividend yielding companies tend to show higher volatility in returns, on average. An active approach to dividend income investing can seek to reduce portfolio return volatility by not chasing yield for yield’s sake, but investing judiciously on the fundamental value of future sustainable earnings growth.

The top dividend paying securities may also not be value-for-risk. Another quirk of chasing the highest dividend yield companies is that they can be poor value for risk taken when compared to the market.

Lower decile stocks by dividend yield demonstrate a better performance for risk than for the top decile of dividend yield companies. The top two deciles for dividend yield show a relatively poor performance in terms of risk taken compared to lower decile companies.

High dividend payout ratios sometimes actually signal decline. Yet another quirk of the income investing market is that higher dividend companies may be value traps, especially if high payouts are indicative of a lack of equity investing opportunities within their own businesses. In short, when a company makes rational decisions about how to manage their business, they have two choices: reinvest earnings in the business in positive return projects if this meets or improves their current return on equity; or, if reinvesting in the business is equity diluting, they can elect to pay out earnings as normal or special dividends.

There is a third option, share buybacks, where a company purchases its own stock to reduce the number of shares in issue to improve future shareholder returns, but this is not really an investment in future earnings growth nor in improving the capacity of the actual business.

A classic example of a high dividend paying company compared to a company which has productive opportunities for reinvestment is the difference between Telstra and CSL. Telstra was long considered a key dividend paying stock for investors seeking income from equities. It was sold as such by the Federal Government when it was privatised to mum and dad investors. Over the years, the burden of being the largest telco, legacy systems and infrastructure, rapidly changing technology and limits to growth have seen Telstra lose its status as a key dividend stock. Telstra’s dividends have not grown over time. By contrast, CSL has steadily transformed itself from also being government owned, as the Commonwealth Serum Laboratories, into a global leader in biotechnology, largely by balancing the payment of dividends with significant reinvestment in the growth of its business and IP. CSL has a global contestable marketplace. As a result, CSL’s shares show a growing dividend over time.

Most companies maintain a balance between reinvesting and paying dividends. If high dividend yield companies are such because they lack productive projects in which to invest, in all likelihood they are disinvesting towards an ultimate decline in their business.

Astute active dividend income approaches can seek dividend yield while avoiding companies with no opportunity to reinvest earnings and improve return on equity. In other words, active approaches can avoid companies whose business models are in decline.

Moreover, an active dividend income approach can actively tilt exposures towards companies with both strong dividends, and value-adding opportunities, to expand their business by reinvesting some of their earnings into positive return projects. This can help improve the quality of dividends in a portfolio, and add growth in future dividend income. Actively tilting towards quality companies such as this can help reduce volatility in the overall portfolio.

Stocks tend to outperform around ex-dividend dates. After companies announce earnings, investors tend to bid-up stocks with an impending dividend payment. Once a stock goes ex-dividend (the date from which new owners are not eligible for the current dividend) the price should, theoretically, fall by the amount of the dividend. This is not always the case. Moreover, quality dividend stocks also tend to recover well, ex-dividend, on renewed demand from investors. This provides opportunities for active dividend income investors to take advantage of these inefficiencies around ex-dividend dates through tactically overweighting towards quality dividend paying companies.

Another misunderstanding about active dividend income strategies is assuming that they rely on franking credits and the imputation system. The dividend imputation system was introduced by the Hawke-Keating government in 1987 to solve for the double taxation of company profits where companies paid tax from earnings, and investors then paid tax on these net earnings.

The imputation system may be impacted by the outcome of the 2019 Federal election. However, it is important to note that franking credits are just part of an integrated active dividend income approach. Active dividend income investing can still outperform passive yield chasing without the existence of franking credits, and can also actively increase its exposure to tax effective dividend income beyond what is typically available in passive approaches.

Why the active dividend approach is relevant for investors

The dividend income market is transforming. Income investors like SMSFs, retirees, and investors approaching retirement can diversify away from traditional sources of income, like fixed income and term deposits, for a longer-term approach, diversified across high-quality Australian companies. They can do this in equities without sacrificing the potential for long-term growth.

An active approach to dividend income investing can outperform the market, and is superior to passive income investing approaches as it can actively avoid dividend traps, actively seek quality companies with stable and growing dividends, offer better risk-adjusted returns, make the most of tax effective franking, and deliver less volatility than the market itself.

Finally, the income and earnings quality focus of an active dividend income approach provides a more defensive equities option with regular income benefits that can help improve portfolio resilience and diversity.

By Michael Price, Portfolio Manager of the Ausbil Active Dividend Income Fund