James Studdart

Our aim is to assess credit market cycles in order to structure beta and stock picking policies. For the first time in 46 editions of this Global Credit Quarterly Outlook we feel there are multiple turning points in these cycles that simultaneously have an impact on markets.

It is clear to us that deglobalization is under way. This is a secular trend fueled by widespread populism, which will cause trade tariffs to rise for the first time in 40 years. In the medium term this will put pressure on the advantage of cheap outsourced labor (China), ultimately eroding record-high margins and potentially limiting the breadth of firms’ global customer base.

Another secular trend is the development of a less economically favorable demographic backdrop, changing established trends in saving and investment. Finally, the bursting 12 years ago of the debt super cycle is the main ongoing reason for cautious household sector behavior and the consequent impotence of traditional monetary policy.

Furthermore, we are having to cope with a cyclical slowdown in growth, more frequent mini spread cycles driven by lack of liquidity, and central bank interventions due to fading inflation. These events have become much more cyclical in nature.

In order to take advantage of all these turning points and quick changes in market direction, one has to be smart, quick and lucky. In retrospect, only December 2018, which was a time when there wasn’t much liquidity, proved to be a good entry point. The research of Jamie Stuttard, our credit strategist and co-head global macro, illustrates that there is typically a short period of time after the first rate cut where credit performs well, a ‘sugar rush’ if you will. Again, one has to be smart, quick and lucky to take advantage of that.

We do not make it our central thesis to continually trade beta higher and lower. Although we do try doing so when possible, we believe we are in the phase of the credit cycle when stock picking, regional allocations and sectoral trends have a much higher relative probability of being profitable.

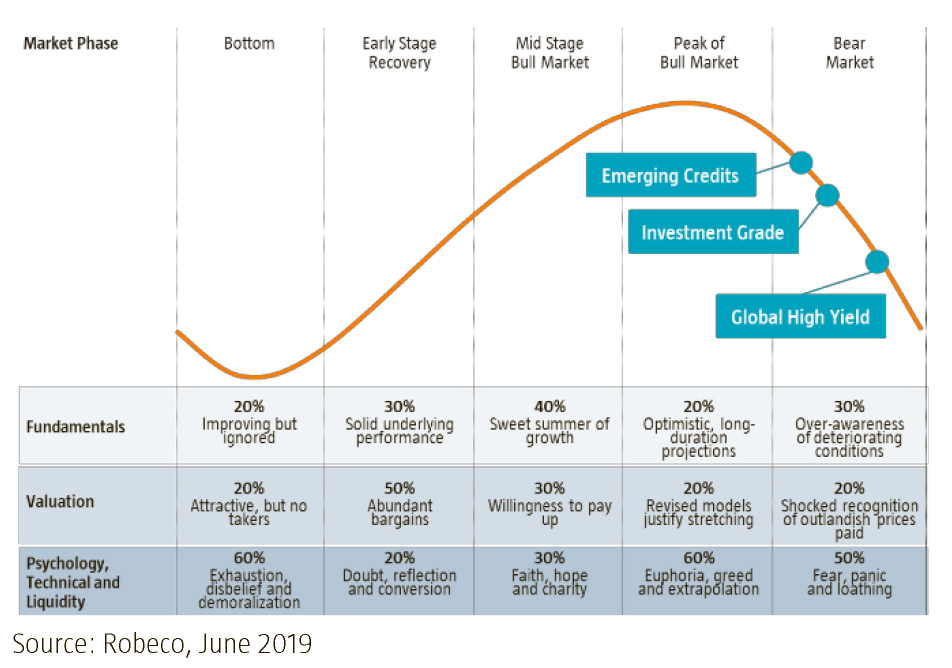

According to Stuttard, we are still in a slow bear market, marked by sugar-rush rallies from time to time, just as was the case in the 1997-2002 cycle. Meanwhile, central banks are stubbornly and repeatedly trying the same remedy to cure the patient – a recipe which ultimately does not work. However, we know it is wise not to fight the Fed or the ECB. QE might return and we may then have more reason to be overtly bearish.

Fundamentals: follow the debt

In this part we look at economic fundamentals, such as economic growth, inflation expectations, debt levels and FX considerations.

A new secular trend

Corporates have since 2000 gained a larger share of GDP relative to workers. Margins have been on an uptrend, corporate taxes were cut in many countries, and de-unionization and Chinese manufacturing capacity have pressured wages. This globalization trend gave rise to a few ‘supercompanies’, companies that took a disproportionately large market share in their sectors, while muscling away competition. With political trends now reacting, the benign spiral risks going into reverse. It might not immediately have an impact on markets, but higher corporate taxes, trade tariffs and a smaller global ‘GDP pie’ need to be taken into account in forecasting earnings and factor trends.

US: taking stock of that inventory cycle

Back to the cyclical story: in the US, corporate credit has been growing above trend GDP for a while now. The economy has been helped by fiscal stimulus, just like the economist Richard Koo prescribed.

The private sector as a whole is deleveraging but we keep an eye on rising corporate leverage: so far in this cycle we have seen 119% growth in corporate credit. The number of high yield bonds experiencing 10-point price drops is increasing. The concerns about the massive BBB issuance (and share buybacks against it) makes clear that, in this cycle, the risk lies in the corporate sector, and not in the financial sector.

In the technical analysis below we do explain that some of the largest BBB issuers have adopted a more credit-friendly stance. Anyhow, the best we can do now is to apply our credit research and avoid being exposed to accidents like downgrades to high yield or even default. Therefore we closely follow where the debt is. And this time, it’s on corporate balance sheets.

From a macroeconomic perspective, the US inventory cycle is a concern. Inventories have been rising versus sales, and could shave up to 2% off the growth rate, bringing the US economy closer to recession. For the rest, though, the economic barometers are stable and we are experiencing a muted recovery in the US.

The most remarkable phenomenon during this expansion has been the labor market. While we see a record-low unemployment rate in the US, wages are not accelerating and unit labor costs even dropped a touch due to increased productivity. Just recently, we have had two monthly non-farm payrolls reports recording jobs growth of under 100,000, something not seen since 2012. We are alert to any further evidence of the lagged effect of six years of monetary policy tightening.

Europe: an open, vulnerable economy

In Europe things are a bit different. On the plus side, there is no inventory cycle to digest. On the other hand, unit labor costs are rising and there is an elephant in the room which is ill: Italian budget talks might become a recurring theme in Europe, pressuring economic sentiment. All in all, the European economy is growing at a stable yet slow pace. Germany has been the biggest victim, but, should the global knock-on effects of Chinese stimulus come through, the worst might be over for that market, too.

The trade war is here to stay and may broaden into a tech war. In any case, Europe, with its high ratio of exports and imports to GDP, will be most exposed to slower global trade. The decline in German industrial production is a case in point. Asian economies are not doing much better. Industrial production in the region is lagging and everyone is suffering from the Chinese slowdown. The short-term hope is that China will add some more stimulus. This will by no means be comparable to the generous packages of 2009 and 2016.

The conclusion is that, at the minimum, we will experience a short period of softer global growth. There are inventory cycles to be digested and there is a need for lower real yields to keep growth rates positive. The good news is that central banks have acknowledged that they were behind the curve, and are correcting the policy error. A policy-engineered soft landing would be positive for credit markets, which need growth – but not too much either.

Valuation: A sugar rally only?

In this section we look at valuations – which market segments look rich and which offer room for spread tightening?

New issuances absorbed with ease

Markets have turned aggressively from their May weakness. Interestingly, a fairly high volume of new issuance was absorbed remarkably easily during this entire period. Books were sometimes five times oversubscribed.

That tells us that the market perhaps is cognizant of the risk of recession, because this is what is priced into rates markets. By contrast, credit is priced for a much softer landing.

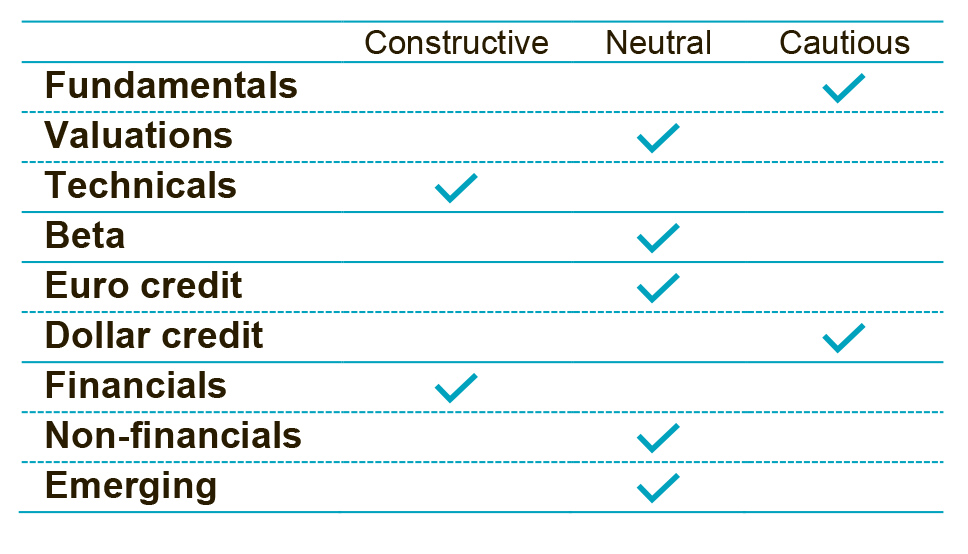

Corporate credit markets are trading at five-year average levels, and high yield is somewhat more expensive. To us that means that an underweight beta position is not the right one for investment grade assets. It worked for us in 2018, but we do not want to position ourselves in the path of a policy steamroller (ECB). We like European senior corporate exposure, preferably ECB-eligible bonds, which might be an argument to be long Euroregion over US credit. That said, in a global context, we see some interesting US opportunities too. US corporates with Asia exposure have underperformed too due to the trade war. In the US, risk-free assets like T-bills are a valid and liquid alternative while waiting for better entry moments.

Bear-market rally

Within high yield we continue to see a striking divergence between high quality and low quality. CCC-rated bonds strongly underperformed during the crash in December. Interestingly, they continued to underperform on a beta-adjusted basis during the rebound in the first quarter. This is an indication that 2019 is a bear-market rally instead of a genuine sustained recovery. We remain overweight in quality in the high yield sector.

Ten years ago we wrote about the chances of Europe becoming ‘Japanified’. By now we can conclude it has happened, given that ten-year bunds are at persistently negative yields, hedging costs are relatively attractive and cash rates are negative – and might soon be lowered even further. However, these developments will make the European credit market attractive for asset owners and even for foreign investors. Recent flows from Asia into Europe may get larger.

A regime shift that calls for nimbleness

A large portion of this industry has been raised with the idea that yields are negatively correlated with asset returns, with higher yields implying tighter spreads. We have now shifted to a regime where lower yields are accompanied by tighter spreads. This has created a correlation amongst asset classes. In combination with poor liquidity and central banks reacting rapidly to financial markets, this makes short-term sentiment almost bi-polar. It requires one to be nimble and to have the capacity to switch quickly from being bearish to bullish, in line with all other asset classes.

The conclusion on valuations is that we have become slightly more optimistic – but not a lot. Spreads are still wider than during the lows of 2018, but yields are too low to chase the current tightening trend. Our preference is to be slightly long in European spread products, but not in a global context.

Technicals: Japanification

In this section we discuss the implications of technical factors for our view on the credit cycle.

Trust the market – or not?

Our macro research strategy team has built on Neil McLeish’s pioneering work on the credit cycle and the Fed cycle. It turns out that a large chunk of spread widening occurs in the first half of the rate cut cycle. Most returns are captured just after the last rate cut. Therefore it remains a delicate choice whether one believes the bond market is right in pricing in 100 bps of cuts. If the market is indeed correct, the next Fed move (lower) is not a buying moment. But, if the bond market is wrong and we see only a continuation of this cycle, credit is not that expensive yet.

One negative indicator is the gold price. Now trading at a fresh five-year high, it flashes as a warning signal. So, both bond and gold markets would need to be wrong in order to abandon caution.

Discernment is called for

We also took a look at the 30 biggest US investment grade (BBB) bond issuers. Collectively these owe USD 1 trillion in debt, more than the entire value of the high yield market. Most of these took the opportunity to issue cheap debt and embark on share buy-back programs, or to start an M&A process. Admittedly, many of these companies have now cut dividends or have at least adopted much more creditor-friendly behavior. This makes us more sanguine than those sell-side strategists who are pointing to a wall of BBB debt. Nevertheless, there will be winners and losers, so it is important to have analysts with first-hand knowledge of the 2000-2002 corporate downturn, who are able to discern which credits are likely to maintain their investment grade status.

The main reason to update the technical section of this Credit Quarterly Outlook is the now-revised central bank stance. The Fed has just given lower guidance on growth and inflation. Central banks will try again to push real yields lower. Therefore they need to execute rate cuts and confirm a dovish forward guidance. It means that asset owners will have to search for yield once again. Our warning is: do not fight the Fed.

An interesting fact on the Asian credit market is that net supply is now very low. Also, 80% of issuance is bought by local Asian investors, signifying a very strong home market bias. Since around half of Asian issuers are debut issuers, it is important to do thorough credit research here: there inevitably will be accidents among the newbies. The Chinese interbank market is also important to watch. A two-decade credit boom is about to break down. Baoshang is a recent warning.

Delaying the inevitable

The conclusion is that the demographically ageing parts of the world may well be undergoing a gradual process of Japanification. The US could be next, after Europe. In such a climate, the alternatives for investors are punitive. In a low-yielding environment, investors are forced to buy credit in order to get decent yield.

We are skeptical of the idea that central banks are infallible, but we also know that they have the capacity to blow asset bubbles for a short while longer, still. We need a real recession to reset the fundamental backdrop, but the longer that takes to unfold, the worse it will be. For now it seems everyone is cognizant of the risks, but the credit market is not priced for them….yet.

Positioning

How will we position our credit portfolios in the coming quarter?

It is fair to state that we still are in a cyclical bear market; as a result, we have not changed our view materially. On the margin we do have a more constructive short-term view. The main reason for this is that central banks are rapidly falling into the same habit, being jolted into action by financials markets.

In our high yield portfolios we emphasize quality and keep a beta of just under one. For our investment grade portfolios we are marginally more constructive due to the chances of a new round of private credit QE.

Further, we prefer sector trading, like energy. We try to be smart, quick and lucky when short-term beta opportunities arise. Liquidity in credit markets is still challenging, though. This requires a contrarian investment style, which is a bi-polar way of trading by selling at times when things look good and buying when markets feel ugly. It also requires a preparedness to take profits quickly.

———-

We would like to thank the guests who contributed to this new quarterly outlook with their valuable presentations and discussions. The views of Hans Lorenzen (Citi), Jonny Goulden (JPM), Hans Mikkelsen (BOA) and Rikkert Scholten (Robeco) have been taken into account in establishing our credit views.