Estate planning and insurance

Making estate planning a part of the financial planning process is not only good for your client – and their family – it’s also good for business.

Improving the financial outlook for the family is the key driver for most Australians, yet many fail to fortify that legacy through sound estate planning and adequate insurance. In this article, Zurich examines the importance of estate planning and within that, the role played by insurance, the funding mechanism for a comprehensive estate plan.

The typical family dreams – ‘buying the family home’, ‘I want to plan for the kid’s education’ and ‘be able to spend more time with the family’ – reflects the Financial Planning Association’s (FPA) findings that for 60% of Australians, the motivation for building wealth is to help build a better future for our families.

Most Australians will commit blood, sweat and tears to this endeavour, but the majority of the community fail to adequately fortify their legacy unknowingly jeopardising – financially and emotionally – the very people they once hoped would benefit from their hard work.

The dynamics within the modern day family can be complex – there is both an opportunity and obligation for advisers to guide their clients through estate planning.

Opportunity and obligation

Over the next 30 years, it’s estimated that $2.4 trillion will be passed down to Gen X and Y, which will see their wealth grow from $1.4 trillion (in 2018) to $3.8 trillion[1]. At the same time, it’s expected that 80% of businesses will change hands from 2018 to 2028, an exchange of $1.53 trillion over the next 10 years[2]. Despite this, many Australians fail to fortify their legacy.

Estate planning is simply the process of ensuring that a lifetime of effort is preserved with the right amount of money landing in the right hands at the right time. Conversations about estate planning between clients and adviser will be highly valued because death – whether expected or not – is inevitable, and your guidance will help clients, and their families, avoid potentially costly and complex problems.

While the componentry of the estate plan and the provision of legal advice falls in the sphere of a legal practice, the process of developing and finalising a successful estate plan is far broader than simply preparing legal documentation. Financial advice professionals are best placed to direct the process given the intimate knowledge they possess about their clients financial and personal affairs.

This is where financial advisers can add significant value to both their client relationships and their businesses. An adviser that can help their client manage family complexities will build deeper client relationships as evidenced by higher client satisfaction and referrals rates.

The dynamics within the modern day family can be complex – there is both an opportunity and obligation for advisers to guide their clients through the Estate Planning process. ASIC imposes obligations on practitioners to provide advice around non-financial product solutions, including estate planning. These requirements are encapsulated under RG175.

RG 175.354

Recommendations about a financial product may not fully meet the client’s relevant circumstances in all cases. In some cases, complying with the best interests duty will require an advice provider to give the client advice that is not product specific – for example, advice on debt levels, estate planning or Centrelink benefits.

RG 175.403 (d)

The conflicts priority rule means that an advice provider must recommend nonfinancial product solutions relevant to the client’s situation, where appropriate, even if this means the client is less likely to need financial advice in the future (e.g. advice on debt reduction, estate planning and/or Centrelink benefits)

The estate plan

While a financial plan focuses on creating and preserving wealth, an estate plan defines how this wealth should managed during your clients’ lifetime, and importantly, how this wealth should be disbursed after death. An estate plan also details the important decision as to who will administer your clients’ estate.

Some sobering statistics to consider[3]:

- According to the office of the NSW Trustee and Guardian, at least 45% of Australians don’t have a valid Will

- Research found that 70% of intergenerational wealth transfers fail because no preparation of the successors was taking place

- Family owned businesses comprise 87% of businesses in Australia, but only 20% of them have a business succession plan in place.

Often, when people think of estate planning they focus on the consequences following death. As a result, they often do not appreciate that there are many documents which need to be properly drafted as part of their estate planning.

These are:

- Wills

- Powers of attorney

- Memorandum of wishes

- Testamentary trusts

This is documentation a lawyer should prepare and contain your client’s instructions. This includes who your client appoints as executor, the nomination of guardians where there are children, how your client’s assets should be distributed, and importantly, who will make decisions if your client loses capacity.

From an advice perspective, estate planning should be considered early in the financial planning process. Although there is a perception that estate planning slots in at the end of the process, wealth building and protection plays a significant role throughout your client’s life, through the accumulation phase and into retirement, and, finally, when the estate is passed onto the client’s beneficiaries.

The failure to implement a sound estate plan can negatively impact both the value of the estate and the beneficiaries. For example:

- Disputes can result in lengthy delays in accessing estate proceeds

- The estate could be distributed to unintended beneficiaries

- High legal fees could be incurred to collect all the assets

- Erosion of wealth due to tax implications, reducing the value of the estate.

Estate planning is more than just having an up-to-date Will or establishing a power of attorney. It’s also about making sure your clients’ assets are protected to ensure their bequests leave an enduring legacy.

Insurance – the funding mechanism

While there might be some aspects handled by lawyers, insurance is the domain of advice. Investors spend a lifetime saving and building their wealth. Without an effective and up-to-date estate planning solution, one that includes adequate insurance coverage, families can face a range consequences upon the death or disablement of a parent or partner.

The establishment of comprehensive life insurance is designed to assist individuals and families from the financial impact of certain inevitabilities, such as death, along with those risks in life that can’t be foreseen, such as a traumatic event or a total and permanent disability (TPD).

Life insurance

Life insurance has a special role allowing assets to pass inside or outside the insured’s estate and is therefore pivotal as a funding mechanism in estate planning. The owner of the proceeds of a life insurance policy is the policy owner. If a person is the owner of the policy taken out over their life, then they can dispose of those proceeds through their Will.

Alternatively, if someone else is the policy owner, such as their spouse or children, then the proceeds of the policy cannot be disposed of through the Will.

A further exception is where the insured has made a “nomination of beneficiary” in respect of the policy. It is possible to nominate a percentage (up to 100%) of the proceeds in favour of other people. Normally the people nominated will be the spouse and/or children of the life insured, or business partners. In this case, when the proceeds of the life insurance policy are claimed, the life office will, after reviewing the claim pay the proceeds in accordance with the nomination.

TPD insurance

Where an individual is a business owner, total and permanent disability (TPD) insurance is as important as life insurance. An inherent difficulty in assessing TPD claims – particularly for business owners who often wear various hats preforming several different roles within the business – is the disconnect between insurance policy definitions and the medical assessment of patients.

While doctors assess a patient’s condition based on objective impairment and diagnostic criteria, traditional TPD definitions require the doctor to make a subjective assessment on a person’s ability to perform occupational duties and categorically state whether someone is likely to ever return to work. Extended activities of daily living (ADLs) provide an objective, medically-based alternative for assessing TPD.

Extended ADLs can be used to assess TPD in place of the traditional TPD definition, meaning that in some cases occupational assessment regarding cessation of work and whether the client will ever be likely to work again will not be required. Time is money for business owners – particularly if a business owner is unexpectedly incapacitated. A TPD solution that uses ADLs as a form of assessment can simplify the claim process.

Income protection

Income protection can also play an important role in estate planning; some policies will continue to be paid to the insured’s spouse for up to five years following the death of the insured.

It is worth noting that some insurance policies will provide an advance payment to cover funeral expenses; this amount will vary according to the insurer. According to ASIC’s MoneySmart website[4], funeral costs vary from $4,000 through to $15,000.

Failing to plan

The adage ‘fail to plan, plan to fail’ is especially pertinent in the context of estate planning. People do pass away unexpectedly and ‘waiting for later’ to implement an estate plan may have unintended consequences for their family and beneficiaries.

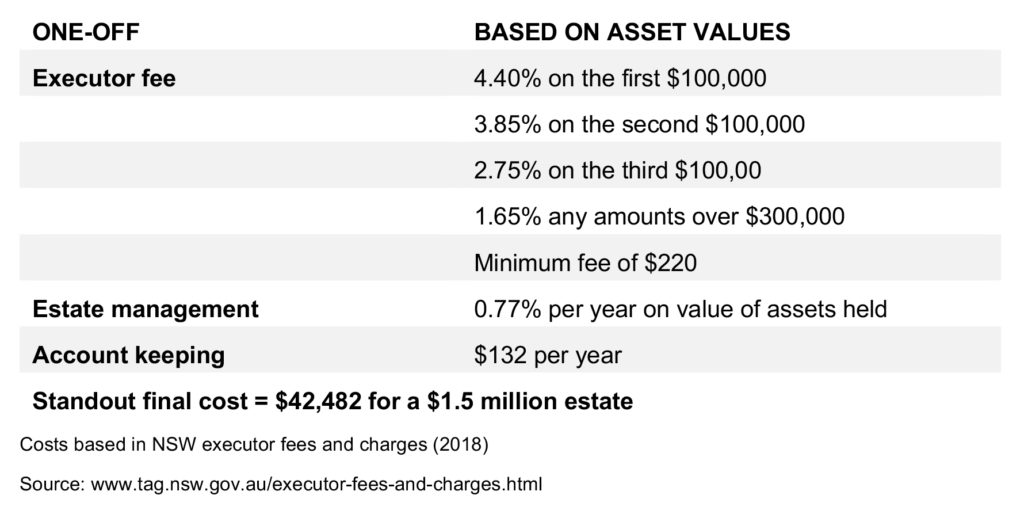

A failure to plan could expose loved ones to financial stress and hardship. It can potentially erode wealth through unnecessary taxes and legal fees. Those who die intestate (without a valid Will) will have their assets distributed according to a legislative formula, one that may not reflect their wishes.

The following table illustrates what it might cost when the state managers the affairs of someone who dies intestate, based on an estate valued at $1.5 million.

A productive collaboration between financial adviser and client relies on a unified understanding of the client’s wishes and prepping all roundtable participants ahead of time. Making estate planning a part of the financial planning process is not only good for your client – and their family – it’s also good for business.

——–

[1] Source: ING DIRECT The Truth About Gen X and Gen Y 2016

[2] Source: mccrindle, Dare to Dream, 2017

[3] Bria Program, Shirlaws Tim Dwyer 2014

[4] https://www.moneysmart.gov.au/life-events-and-you/over-55s/paying-for-your-funeral

![]()