Lisa Gregory

Recent discussion in the media has suggested that the dollar amount needed for a comfortable retirement has been overstated.

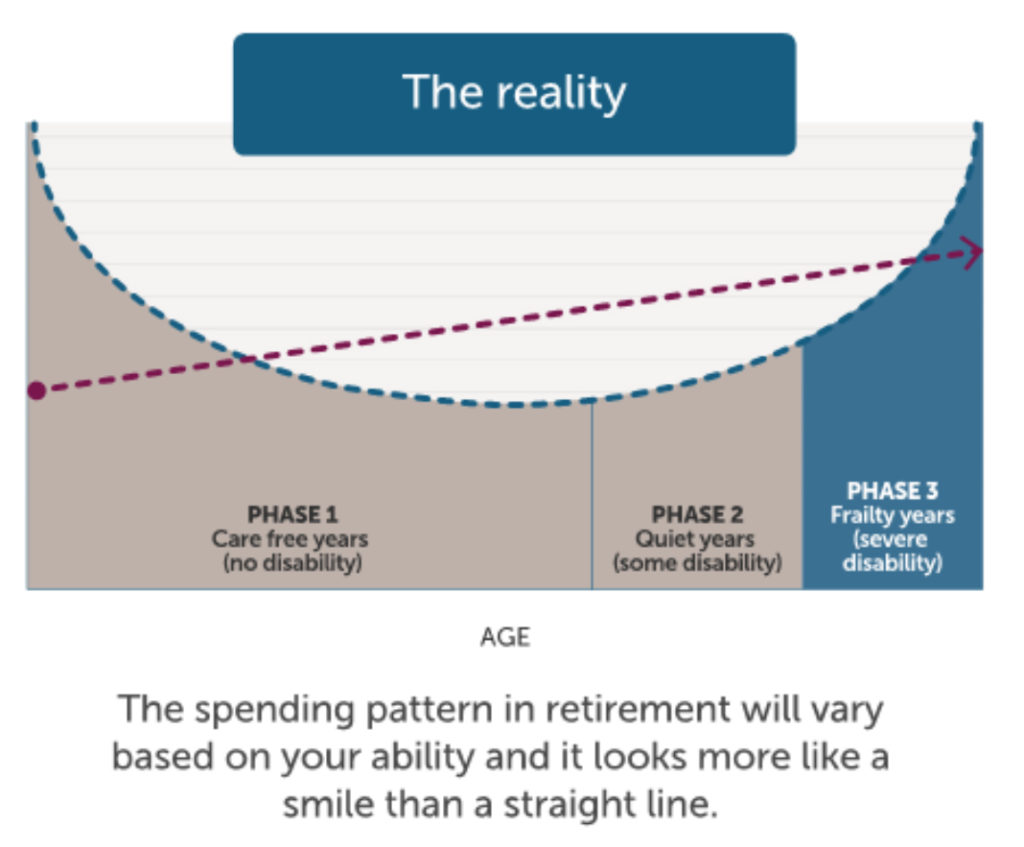

While it is true that many of us can get by in our retirement with less than the often-quoted recommendation of ‘at least a million dollars in super’, there are significant costs associated with ageing that are regularly overlooked in traditional retirement planning – costs incurred during the frailty years.

While lifestyle spending does tend to reduce as we enter our 70’s, living costs can ramp up again considerably during the “frailty” years – the last three to five years of life, generally after age 80. It is then that we are likely to have some form of disability caused by ageing, as well as a general decline in independence, which means we become reliant on others.

Business Partnership Manager at Aged Care Steps, Lisa Gregory, believes that the common view that Medicare can shield people from the bulk of health costs in older ages misses the point.

‘Aged care is not covered under Medicare,’ she says. ‘There are government subsidies, but consumers need to contribute to the costs of care – potentially both their accommodation costs and actual care needs.’

Increasing longevity and expectations around the quality of care as we age are also putting greater pressure on income needs in the later stages of retirement.

Aged care covers a range of support services – including home care, respite and residential care – all of which may require consumers to contribute to the cost of care via a means-tested calculation.

The Association of Superannuation Funds of Australia (ASFA) figures projecting the cost of a ‘moderate’ or ‘comfortable’ retirement appear to make insufficient allowances for aged care needs, giving cause for concern about the potential for families to be left unprepared when a crisis occurs. Provisioning for the cost of aged care is not a luxury; it’s a necessity, which is why planning for the cost of future care is critical for families to discuss before an urgent need arises.

‘We encourage adult children to talk with their parents and an accredited aged care professional to discuss potential aged care options, before a crisis arises,’ says Ms Gregory.

‘An open and honest discussion with family – and an understanding of quality of care expectations and affordability – can help retirees to maintain greater control and independence as they age.’