Walk a mile in your client’s shoes

Walk a mile in your client’s shoes – it’s more important than ever to clearly articulate the value you bring to the relationship.

Australian insurance literacy is low by world standards. Australians who receive financial advice are more likely to have better literacy levels and a better understanding of their own position.

In this article, Zurich explores the need for advice and provides some strategies for articulating your value to clients.

The need for risk advice

There’s a good reason for risk advice. The laissez-faire attitude to insurance taken by many Australians has resulted in significant under-insurance nationally. Research[1] has found that Australians who have received financial advice specifically on life insurance are considerably more likely to be insurance literate than those who have never received such advice.

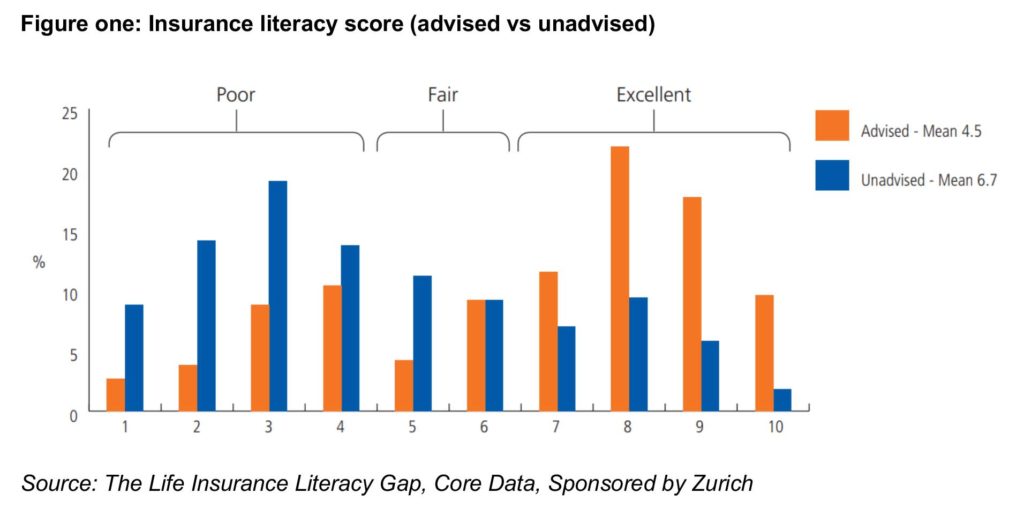

Australian life insurance literacy – an understanding of life insurance products and coverage – is low by world standards. Insurance literacy is important; after all, you don’t know what you don’t know, and a potential client won’t understand their needs if they’re not insurance literate. The average literacy for the advised was approaching ‘Excellent’ levels, compared to the unadvised, who on average, fell into the ‘Poor’ range of scores (figure one).

Of those who were surveyed, 58.1 percent rated their life insurance knowledge and experience as average, while 21.2 percent rated their knowledge and experience as poor or very poor. This presents an opportunity to educate prospective clients; people are more likely to engage with a concept once they understand it. Once insurance literate, a client will be more likely to invest in risk products.

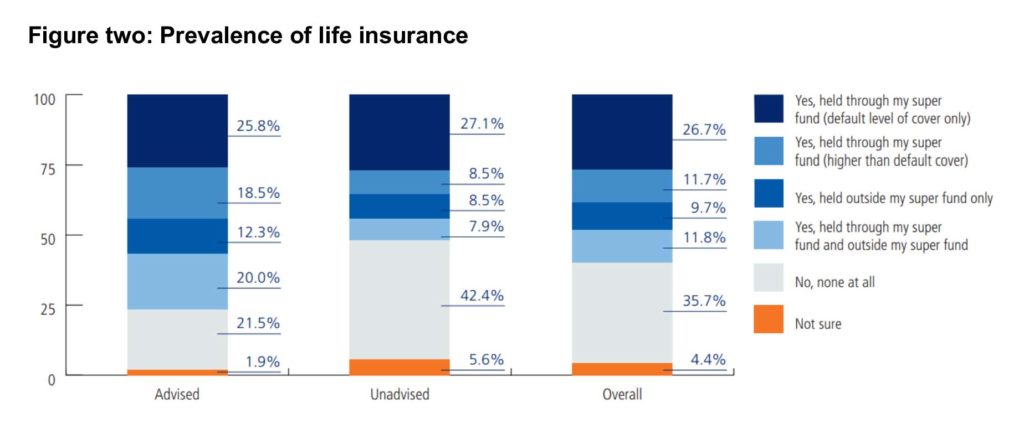

Having some form of life insurance is generally a good indicator of financial ‘fitness’, and by proxy, financial literacy. Advised Australians are considerably more likely than unadvised Australians to have some form of life insurance, whether held inside or outside of super (figure two).

Although nearly 60 percent of Australians have some form of life insurance, 62.7 percent of those hold it through their super fund. Only 10.5 percent take out that cover with the advice or assistance of a financial adviser.

Not surprisingly, advised Australians are considerably more likely to have some form of life insurance, whether held through superannuation or outside super; the unadvised who do hold life insurance are almost twice as likely to have the default levels of coverage set via their super fund. This means there’s a greater risk of them having cover that’s potentially inadequate for their circumstances.

Among those who elected to settle for the default level of insurance cover provided by their super fund, nearly one quarter believed it looked sufficient; only four percent came to that view with the aid of a financial adviser.

A super overestimation

While the majority of respondents correctly identified that they can obtain life insurance through their super fund without having to pay for it directly, they found other insurances a tad more confusing. For example, a small proportion of respondents incorrectly claimed they could obtain home, car or travel insurance through their super fund.

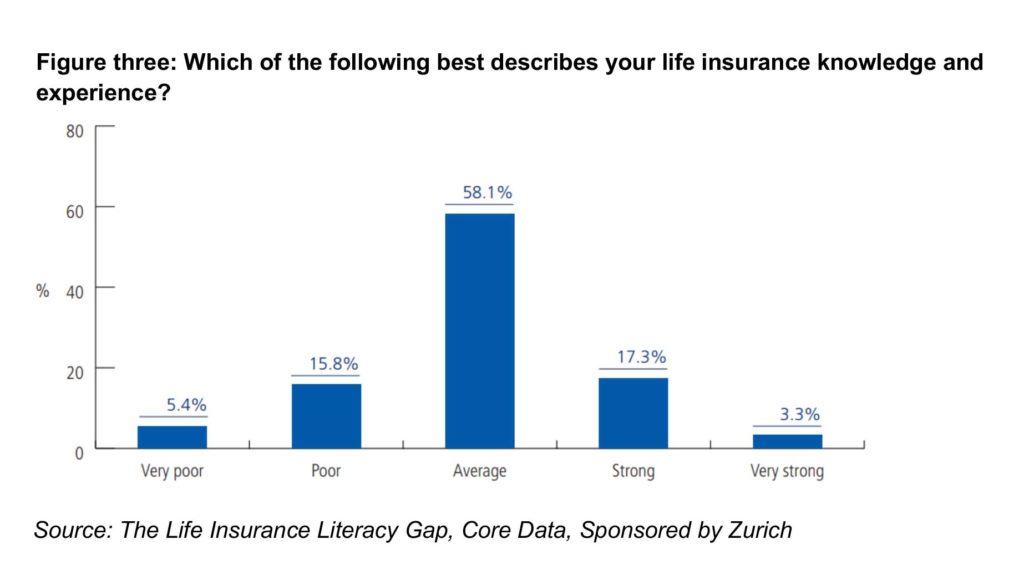

Of greater concern was the large number of Australians who believed they could access a variety of risk products through their super fund; for example, more than 41.2 percent incorrectly believed that they can obtain trauma cover through their super fund. It’s not surprising then that one in five Australians have poor knowledge and experience of risk insurance (figure three).

Not good on the detail

Although some of those who participated in the research may have understood broad concepts about insurance, they weren’t so good on the finer details. For example:

- Only two in five realised that being diagnosed with a terminal illness may be a trigger for an insurance payout

- One in five were unsure under what events a term life insurance policy would pay out

- A number of people believed health insurance to be a more effective protection against a serious medical condition than trauma insurance

- One in ten believe the National Disability Insurance Scheme (NDIS) to be a substitute for TPD insurance

Of concern is confusion about the role of the NDIS, and how it differs from life insurance. Unadvised Australians are more than twice as likely to regard the NDIS to be an effective substitute for income protection and a third believe it’s an alternative to TPD insurance.

Barriers to risk advice

Given the low levels of insurance literacy already described, a lot of people need expert help. Oxford University research[2] found that in Australia, independent financial advisers were the preferred source of that expert help. Advisers are seen as the most reliable source of life insurance help, but the cost of advice is a barrier.

Mind the gap

When consumers were asked about their willingness to pay an out of pocket fee for life insurance advice, there was a significant disconnect between what they would pay and what advisers believe they would need to pay. None were willing to pay $2,000 or more, the figure 65 percent of advisers said they would need to charge. The majority of consumers – 78 percent – are willing to pay $500 or less, a figure one percent of advisers nominate as a potential fee.

When it comes to insurance, commission is the most common way consumers pay for advice, with over 80% of advisers charging in this way. This works for adviser and client because it eliminates the need for the client to find a substantial amount of money to fund an upfront fee.

The Risk Advice Disconnect study found that restricting or banning life insurance commissions would impact both the ability of average Australians to access life insurance and would likely reduce the supply of that advice.

Many advisers believe it’s too hard to reduce the cost of advice. Close to 80% of the advisers surveyed felt a combination of costs associated compliance processes, technology and product complexity provided a significant barrier to reducing the cost of advice.

The value you bring

There is a clear need for risk advice in Australia; lack of insurance literacy and underinsurance are real issues. At the same time, cost can be a barrier. It’s never been more important to clearly articulate your value to existing and prospective clients. Existing because you want to retain your clients and of course, they can be a great referral source of new clients.

Nearly every business strategy paper you read or session you attend will tell you to start with a strong – and unique – value proposition. There’s a good reason for that – it’s good advice. They’ll also tell you to see things from your client’s perspective – or put yourself in their shoes. However, it can be deceptively challenging and, when competing with all the other things you need to do each day, often gets pushed to the backburner.

A value proposition is more than a pithy catchphrase or flash tagline. It should be central to your business because directs what you do and how you do it, and importantly, helps you focus on where you most add value.

Why would a prospective client choose you over another financial adviser?

Five steps to a sound value proposition

1. Who is your ideal client

Who is your ideal client? What does this client care about and how do they go about their decision making? The more you know about your ideal client, the more easily you’ll be able to engage with them. Some businesses create personas of their ideal clients…these may be based on demographics, personality types, life stage, profession or other criteria. You may prefer to target the financially literate, or instead target those who would benefit from education to improve their financial literacy.

2. What problem do you solve?

What are the problems your prospective clients need to solve? Is it improving their knowledge and financial literacy first? List out the client persons from step one and what each may want to achieve. For each, list the problem you solve and the potential challenges facing each client persona.

You’ll need to put yourself in your clients’ shoes to think about their problems, needs and challenges. While some clients understand what they need, others need you to explain the problem before they can fully understand their own needs and the steps to take to solve it.

3. How do you solve this problem?

For each persona or client type, articulate how can solve their problem, what service can you provide to make his or her life better. For example, a client with life insurance in super may believe they have adequate insurance cover, but really want cover for illness or injury. In stage two you have listed out problems and challenges – now look at the ways you can resolve each problem. Remember – your client isn’t buying a specific risk product; they are buying a solution to a problem.

4. Why you?

A value proposition often contains the word ‘unique’ – in other words, what makes you stand out from the fifteen thousand or so advisers around the country. Granted, the competition won’t be so vast in your geography, but you still need to stand out.

It’s a good idea to have an eye on your competitors and know how each positions their business. You want to differentiate your offering from the advice practice down the road, so it’s clear to prospective clients why your financial planning and risk approach is different to and better than the alternatives. Importantly, make sure what sets you apart is relevant to your current and prospective clients; what might seem like a great marketing campaign may not translate to a solid value prop.

5. Show them the proof

Client case studies are a great way of proving your worth. Being able to tell stories about ‘people like them’ will help your clients understand what you do, how you do it and who for. A good story will demonstrate that you understand clients’ problems and solve them – you don’t just sell life insurance products. However, remember it’s all about the client and not about you – don’t overwhelm them with ‘proof’ and don’t make it about you – it’s always about the client in front of you and the clients you have helped.

In the clients’ shoes

As outlined in point two above, you need to think from your clients’ perspective, put yourself in their shoes. What are the problems they may seek to solve, what might be their challenges and frustrations? How can you address those problems, resolve their challenges and frustrations?

Putting yourself in your clients’ place is all about empathy – putting aside your own perceptions about their needs and actively listening to the client; their issues, concerns, beliefs. Clients don’t always articulate their problems the way you might expect, you may need to ask questions to get to the heart of their needs. You need to measure your perceptions of a client’s experience against their reality.

In an environment where financial literacy is low, particularly in the risk space, and consumers unwilling to pay for products and services they probably don’t understand, it’s more important than ever to clearly articulate the value you bring to the relationship. The best way to do that is to see the world from their perspective.

It’s important to remember that it’s all about the client and they need to recognise that too. After all, that’s why you’re in business. You want your clients to have a positive experience. After all, the only person who can judge your success is the client, and, as the saying goes, their success is your success.

———

[1] The Risk Advice Disconnect, Zurich

[2] The Life Insurance Literacy Gap, Core Data, (sponsored by Zurich)