The first cold war ended in November 1989 – the new cold war – 2.0 – is occurring between the US and China.

Bill Priest, CEO, co-CIO and portfolio manager of Epoch Investment Partners (Epoch) recently visited Australia to share Epoch’s world view with financial advisers and in particular, the potential impact of Cold War 2.0 on investment markets.

In this article, GSFM shares Bill’s insights, gleaned from an investment career spanning more than 45 years, and discusses how advisers can find the elusive yield in this environment.

There’s a wall of worry facing investors world-wide. Is a recession looming or ‘just’ a slowdown? How will the US-China trade war impact the global economy and what does elevated political uncertainty mean for markets? How will issues such as the continued rise of populism, Brexit or issues in the Middle East impact domestic and global markets?

Cold War 2.0

The first cold war ended in November 1989 – thirty years ago – with the fall of the Berlin wall. The new cold war – 2.0 – is occurring between the US and China. The platform is trade and technology is a key part of it.

Although recent trade negotiations between the US and China produced a welcome truce, coupled with expressions of goodwill to tackle the tougher issues later, it’s likely to be a temporary cease fire. China has violated more World Trade Organisation (WTO) regulations than any other country that’s ever signed up to the WTO – this isn’t likely to end for some time and is feeding the prevailing uncertainty across global markets. Most of the big disputes are unlikely to be resolved before November 2020 (the next US election) or, for that matter, the 2024 election.

The contentious issue of intellectual property (IP) theft helps illustrate why this is the case.

According to the US Trade Representative, Robert Lighthizer, China is close to agreeing to adopt normal best practices for IP, including criminal enforcement of violations with sufficiently stiff penalties. Apparently he believes this is the case because China has produced enough sophisticated technology on its own that safeguarding IP is now in its national interests.

The problem is that Lighthizer himself has repeatedly lamented that China has made false promises to respect IP on countless occasions. Moreover, China’s own government is highly active in stealing IP and industrial espionage. In fact, economic espionage has become a prime directive of the Ministry of State Security (MSS), and the FBI has estimated that 3,000 Chinese companies in the US are covers for MSS activity. Therefore, Epoch believes China’s pledge to tighten IP protection is unlikely to amount to more than window dressing.

It should be clear to everyone by now that this is not just a trade war; indeed, several recent disputes have made it manifestly clear that the clashes between the US and China are much bigger than trade or even tech.

On October 5, Daryl Morey, the general manager of the NBA’s Houston Rockets, ignited a furore in China with a seven-word tweet: “Fight for freedom. Stand with Hong Kong.” Chinese nationalists angrily asserted that Morey was challenging China’s sovereignty over Hong Kong. Chinese broadcasters quickly announced they would not air Rockets games and retail outlets stopped selling Rockets gear. Because China is by far the NBA’s most important international market, NBA executives quickly distanced themselves from the perceived offense.

As The Economist has emphasised, self-censoring to make money in China is a long-standing business practice. The most obvious example is Hollywood, where studios steer clear of any topics that might offend the Chinese Communist Party (CCP). But virtually all foreign businesses operating in China have long self-censored in a more subtle, pernicious way: by never speaking publicly about any issue the CCP deems off-limits (including the three Ts — Taiwan, Tibet and Tiananmen).

China’s fierce reaction to Morey’s tweet is certain to induce more self-censorship by executives in the future.

Since the fall of the Berlin Wall, America’s approach to China has been founded on a belief in convergence. The prevailing view was that integration into the global economy would not just make China wealthier, it would also make it more open, tolerant, democratic and market-oriented. Today, however, dreams of convergence are dead. America has come to see China as a strategic rival—a malevolent actor and duplicitous rule-breaker. How did that happen?

One key catalyst was President Xi’s ascension in 2012. During “the new era” he has exalted and entrenched the state’s leading role in the command economy. He has also developed a sophisticated surveillance state to stifle dissent and tighten the authoritarian screws, squashing delusions of China morphing into a free and open society. Further, its Belt and Road Initiative made it plain that China has no interest in embracing the American-led global order. Rather, it is seeking to radically overhaul it.

Trade is the battle, tech is the war

In addition to the cascading collapse of the Soviet state, something else happened in 1989, and that was Tiananmen Square. With that tragedy a different kind of threat emerged, although its true extent has only become fully appreciated during the last couple years. This realisation has marked the beginning of this new Cold War, one that requires quite a different type of containment policy than the first.

Although Cold War 2.0 is not likely to become a hot war, the stakes are just as important. And the stakes are values, as represented by the US Bill of Rights, which guarantees civil rights and individual liberties — including freedom of speech, press, and religion. It also sets rules for the due process of law, and places clear limitations on the government’s power in judicial and other proceedings. In addition, democratic institutions and comparatively free markets have been key to the vibrancy and success of the US experiment.

However, these values are anathema to China’s autocrats. The CCP under President Xi wields power that is unbounded and unchallenged, without the checks and balances provided by an independent judiciary, autonomous media, free and fair elections, and constitutionally guaranteed rights for individuals and society. In China, the law is best viewed as a spear rather than a shield. And not only has state and bureaucratic power become even more centralised since 2012, but markets are increasingly taking a secondary role to the whims and commands of the CCP.

While China’s political system is for it to choose, it is conspicuously evident that the two superpowers possess vastly different values, economic systems and visions for the global economy. This is why Cold War 2.0 has become a defining reality, and not just for the next couple years, but likely for decades to come. And, at least initially, trade is the platform on which this war will be waged.

Moreover, almost all measures of global integration (including merchandise trade, foreign direct investment and the activities of multinational corporations) are already in retreat or stagnating. In fact, these metrics have been in trouble for the good part of a decade now. This regrettable trend is negative for overall economic efficiency and growth, as well as margins and profits, which raises several challenges for investors.

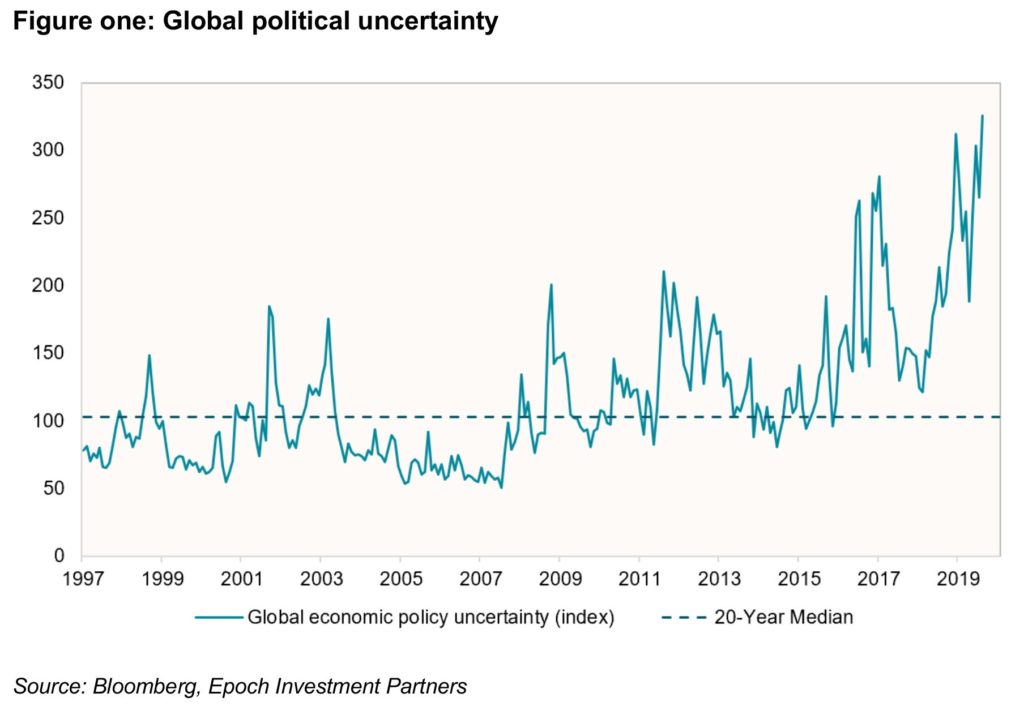

With the advent of Cold War 2.0, global economic policy uncertainty (figure one) has skyrocketed to a record high (the data-series inception was 1997). This has led to slower global growth, which has resulted in today’s hyperactive central banks riding fast and furious to the rescue.

Three key issues will continue to dominate from the US perspective; market access, IP protection and opaque industrial subsidies. The Chinese government fears containment and has stressed it will not compromise its values. As well as risk surrounding trade, the Cold War 2.0 brings increasing risk of a currency war, which could include restrictions on investment and capital flows.

Capital markets outlook

On the upside, the team at Epoch is not anticipating a global recession. Mixed signals abound, pointing to challenging times ahead. While some economies (such as Germany) may fall into recession, it’s unlikely to be experienced globally.

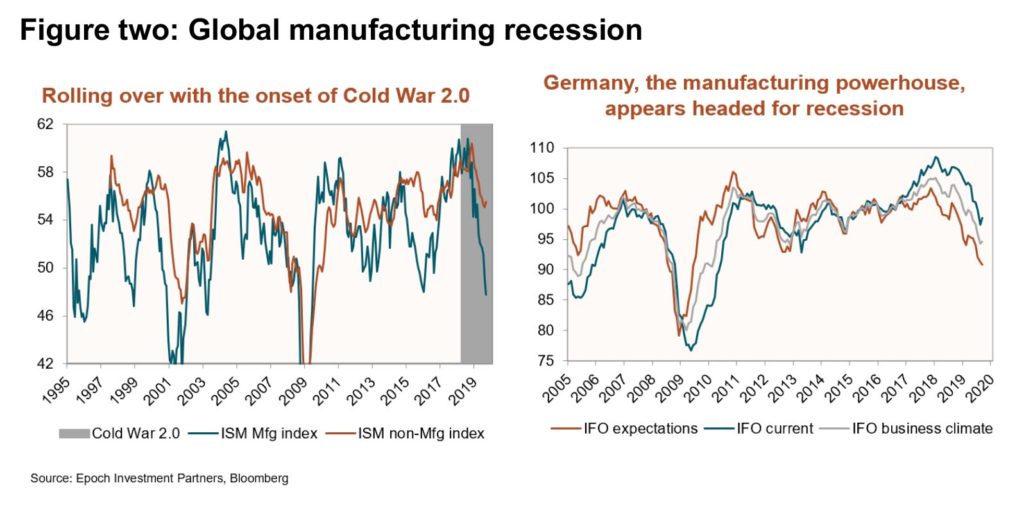

The US manufacturing index (ISM) suggests manufacturing has declined since the onset of the Cold War 2.0, but that’s only part of the story. The non-ISM (non-manufacturing industries) numbers are more solid (figure two). At the same time, Germany’s business climate index the IFO, a closely followed leading indicator for economic activity, is close to its lowest level since November 2012.

A recession is defined as two consecutive quarters of negative GDP. Negative GDP is comprised of two things: growth in the workforce and growth in productivity. In the US, while productivity growth might be weak, the workforce is still growing – therefore recession in US is unlikely.

Capital expenditure and export growth have both been negatively impacted by the Cold War 2.0. Profit margins for the S&P500 were flat from the 1950s to 1989 – then it took off, at the end of the first cold war. This was when China came into the ‘world’ and the global labour force grew by over one billion people. China brought no money or technology, but a giant labour arbitrage opportunity – this is now coming to an end.

Trade war consequences

There are two significant consequences of the trade war – the end of margin expansion and the end of price discovery.

Margin expansion

Globalisation has faltered. For the three decades following 1989, large and sustained increases in the cross-border flow of goods, services, capital, ideas and people were the most important factor in world affairs. However, today most measures of global integration are in retreat or stagnating.

Manufacturing margins were flat for decades at around 6 percent, but they have doubled since 2000, with four factors explaining most of the expansion (figure 4): labour arbitrage derived from China entering the WTO, the evolution of complex and highly efficient global supply chains, lower corporate tax rates and declining interest rates. While lower taxes may be here to stay, the other three are reversing direction, in large part due to rising trade tensions and the transition to QT. Therefore, Epoch expects profit margins to struggle and market multiples to fall or at best remain flat.

Price discovery is the mechanism by which competing buyers and sellers determine the price of a security. Cold War 2.0 has resulted in slower growth, which, in turn, results in lower interest rates, cheap money and falling bond yields (figure five). The US Federal Reserve is likely to lower rates at least another two times and the European Central Bank (ECB) is talking about it. This is a particular issue for the fixed income market.

Every single German bond has a negative yield today; if you have mortgage debt in Denmark, most are negative – in other words, you’re being paid to stay in your own home. An interest rate environment like this destroys price discovery.

Capitalism doesn’t work without a mechanism that allows competition within prices, so the potential impacts on markets is significant. The disappearance of price discovery is exacerbated by ‘hyperactive’ central banks trying to manage the economy in a way that might ease the trouble in the shorter term but will undoubtedly lead to volatility in the longer term.

The hunt for yield

Although bond yields have been driven lower by record high policy uncertainty, the late-cycle slowdown and hyper-aggressive central banks, dividends and buybacks remain robust, partially reflecting a capital-lite world. As a result, the yield available from equities can be far superior to that currently available in fixed income markets.

For example:

- US SPX: Dividend yield of 2.0% + buyback* yield 3.3%

- Europe SXXP: Dividend yield of 3.8% + buyback* yield 1.1%

- Japan TPX: Dividend yield of 2.5% + buyback* yield 1.2%

*Buyback yield = value of shares repurchased divided by market capitalisation

Source: Bloomberg, Yardeni, Goldman

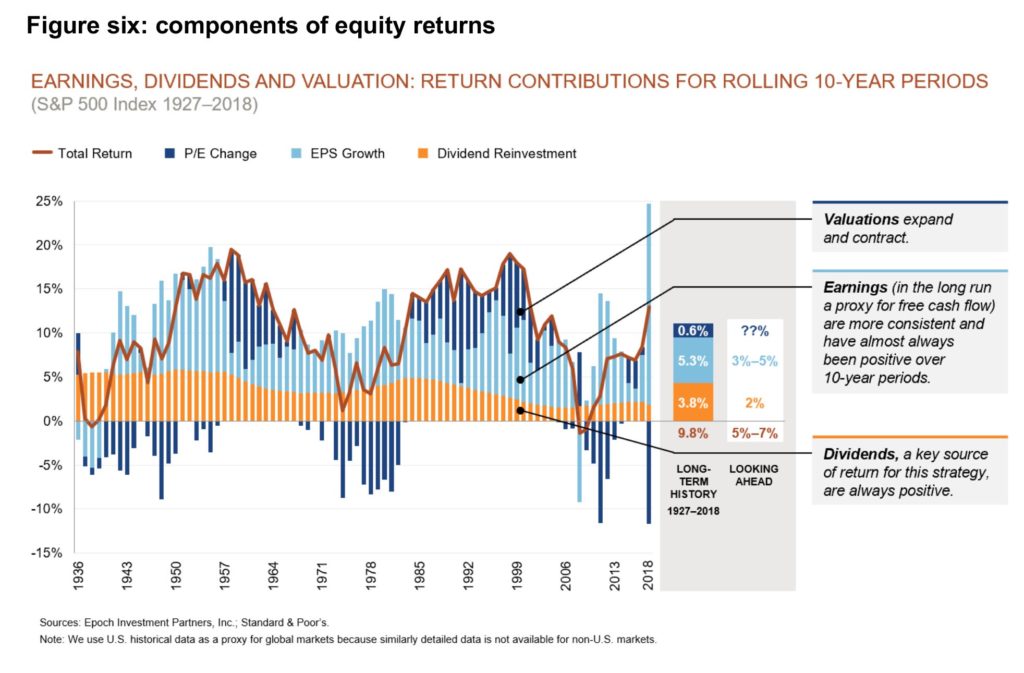

There are three ways to make money from equities: the dividends, the change in earnings and the change in the P/E multiple. As illustrated in figure six, rolling 10-year return for the S&P 500 Index has broken down between those three components going back to the 1930s. You can see that dividends have been a positive contributor in every 10-year time period, and earnings have contributed positively in all but five of the eighty-two rolling 10-year periods.

You may also note that the contribution from dividends seems to have decreased starting in the early 1990s. That is due to the fact that regulatory changes ten years earlier made share buybacks an attractive (and tax-efficient) alternative to cash dividends, and companies began to make increasing use of this additional method for returning cash to shareholders.

Because buybacks reduce the outstanding share count, they tend to drive up earnings per share, so some of what used to show up in this analysis as the contribution of dividends has been transferred to the earnings contribution.

The confluence of Cold War 2.0 and technology has reduced capex expenditure; this makes tech inherently deflationary and helps to explain why we find ourselves entrenched in a ‘lower for longer’ interest rate environment. Indeed, pervasive digital technologies and their associated economies of scale imply that we are living in a disinflationary, capital-light world.

This implies that, with less cash flow being directed to fund capex, payout ratios are likely to remain high and may even rise further from here. So, even as bond yields have plummeted, stranding us in a world of yield starvation, we expect dividends and buybacks to remain robust. As a result, the yield available from equities can be far superior to that available in fixed income markets.

———