Super members have every reason to be optimistic about 2020, but when it comes to a repeat of 2019’s double-digit returns, it would be wise to temper expectations.

Super members have every reason to be optimistic about 2020, but when it comes to a repeat of 2019’s double-digit returns, it would be wise to temper expectations.

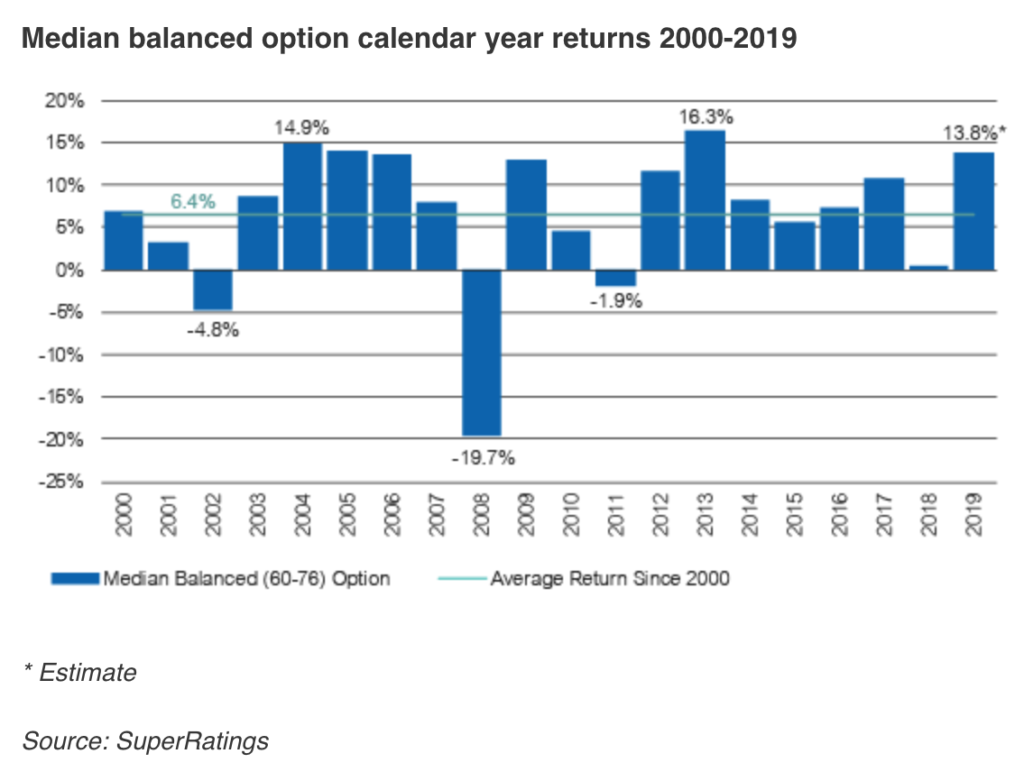

According to estimates from leading research house SuperRatings, 2019 was the best year for superannuation funds since 2013, with the median balanced option returning 13.8%. Despite a selloff in Australian shares in December, funds entered the new year in a strong position as markets shrugged off a string of negative economic news and rising geopolitical tension.

However, funds are already battling the new normal of lower yields and returns, which will make a repeat of 2019’s results unlikely in 2020.

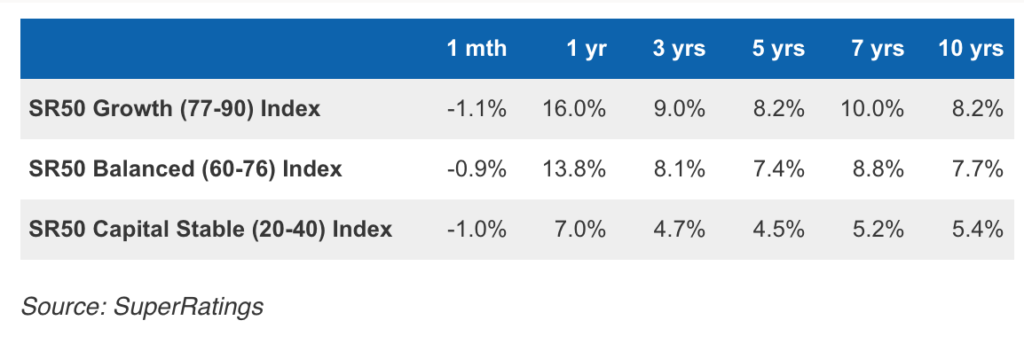

Looking back over 2019, the median balanced accumulation option returned 13.8% over the year to the end of December and has returned 7.7% p.a. over the past decade. December saw an estimated fall of 0.9%, ending an otherwise stellar year for Australian shares, on a sour note. Markets were driven predominately by the health care and materials sectors, while the financial services sector, despite delivering a positive result, remains largely beaten down, thanks mostly to the major banks.

The median growth option returned an estimated -1.1% in December and 16.0% over the year, while the capital stable option returned an estimated -1.0% and 7.0% respectively.

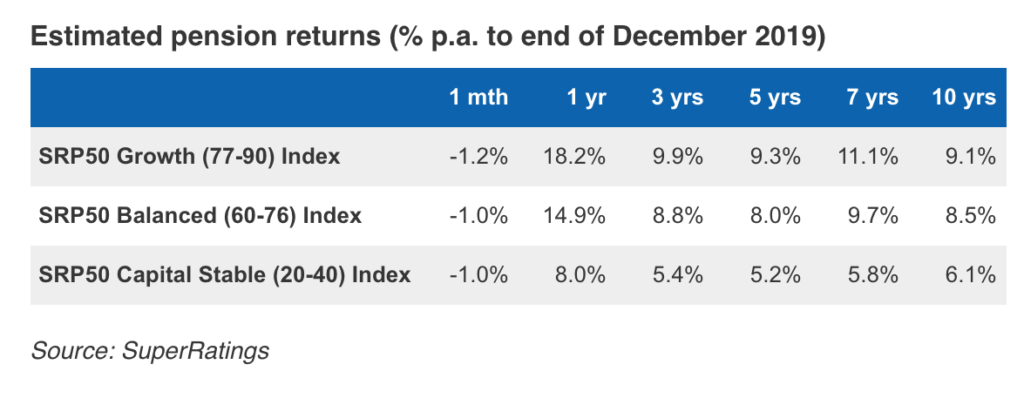

Pensions performed similarly well in 2019, with the median balanced option returning an estimated 14.9% over 2019, compared to 18.2% for the growth option and 8.0% for the capital stable option.

“We’re anticipating a solid year for super in 2020, but the key challenge for funds will be the low return environment,” said SuperRatings Executive Director Kirby Rappell.

“Even with the possibility of a pickup in economic growth, yields are extremely low and it’s getting harder to find opportunities in the market. Company earnings growth is slowing, and Australian consumers are under pressure, so fundamentally it will be more challenging than 2019. That doesn’t mean it will be a bad year, but super members should not expect to bank another 13 per cent.”

Super’s long-term growth story still a winner

As the chart below shows, 2019’s double-digit return compares favourably to recent years and is significantly higher than the average return (6.4% over the past 20 years). Based on SuperRatings’ estimate of 13.8%, 2019 would represent the highest return since 2013 and the fourth-highest over the past two decades.

Following the volatility of 2018, super funds saw steady growth over 2019 with only three down months during the year, with the largest fall in the median balanced option estimated to be -0.9% in December.

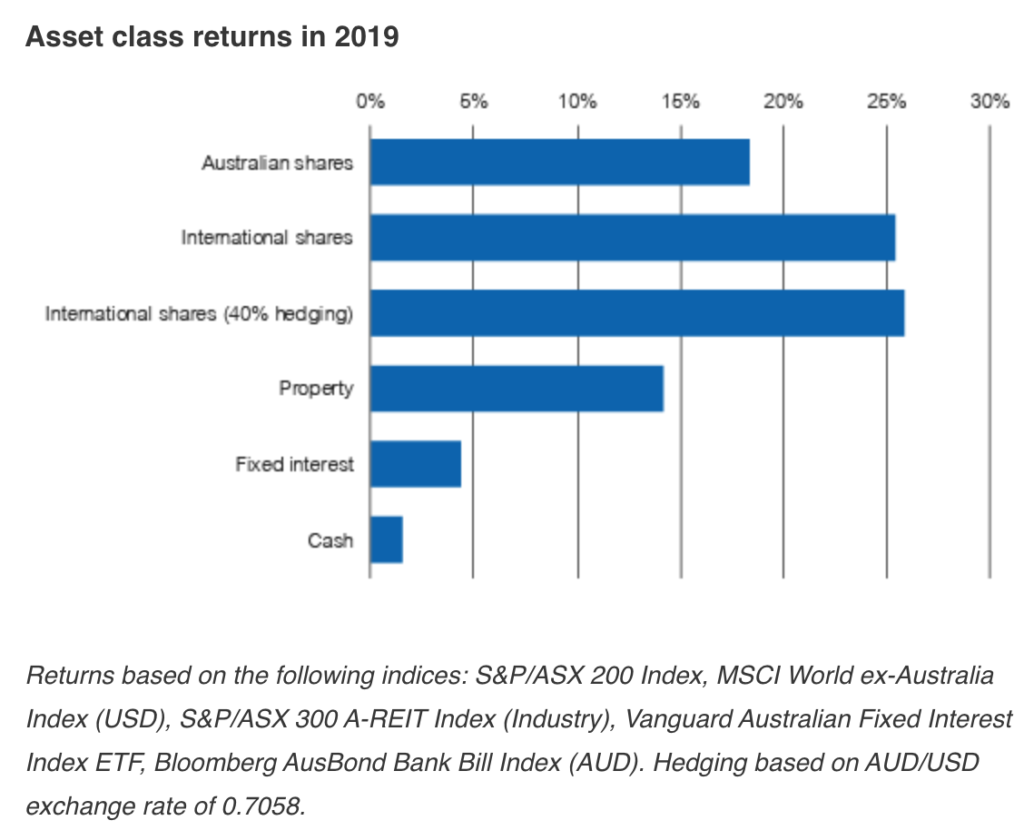

The main drivers of performance typically come from equities, of which Australian shares generally make up the greatest proportion. As the chart below shows, the Australian share market delivered a return of 18.4%, while international shares delivered 25.4% (unhedged) and 25.8% (40% hedged in Australian dollars). Meanwhile, listed property returned 14.2%, fixed interest – another major asset class for funds – returned 4.4%, and cash returned 1.5%. Another important asset class is Alternatives (including private equity), although market-based measures of performance are harder to determine as they are offered within diversified portfolios rather than standalone options.

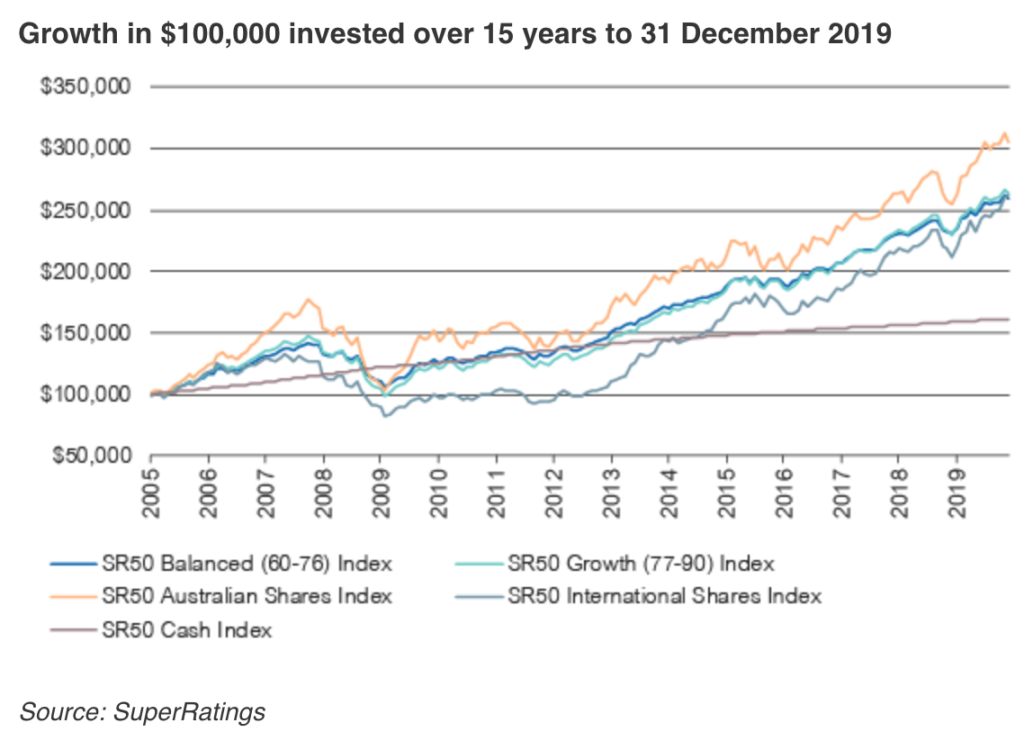

Since the GFC, funds have ridden market turbulence through 2011, 2015 and 2018 to build significant wealth for members. Looking back over the past 15 years to 2005 (before the GFC hit), the median balanced option with a starting balance of $100,000 would have grown to an estimated $259,340 by the end of 2019 (a return of 159.3%). Similarly, the median growth fund would have risen to an estimated $264,208 (a return of 164.2%).

Expect further fund consolidation in 2020

Over the course of 2019 there was a number of high-profile mergers, and 2020 is expected to see more funds come together to achieve greater scale. Mergers have typically been based on geographic proximity, similar industry sectors and strategic fits, with funds seeking merger partners that are strong in areas in which they may be weaker.

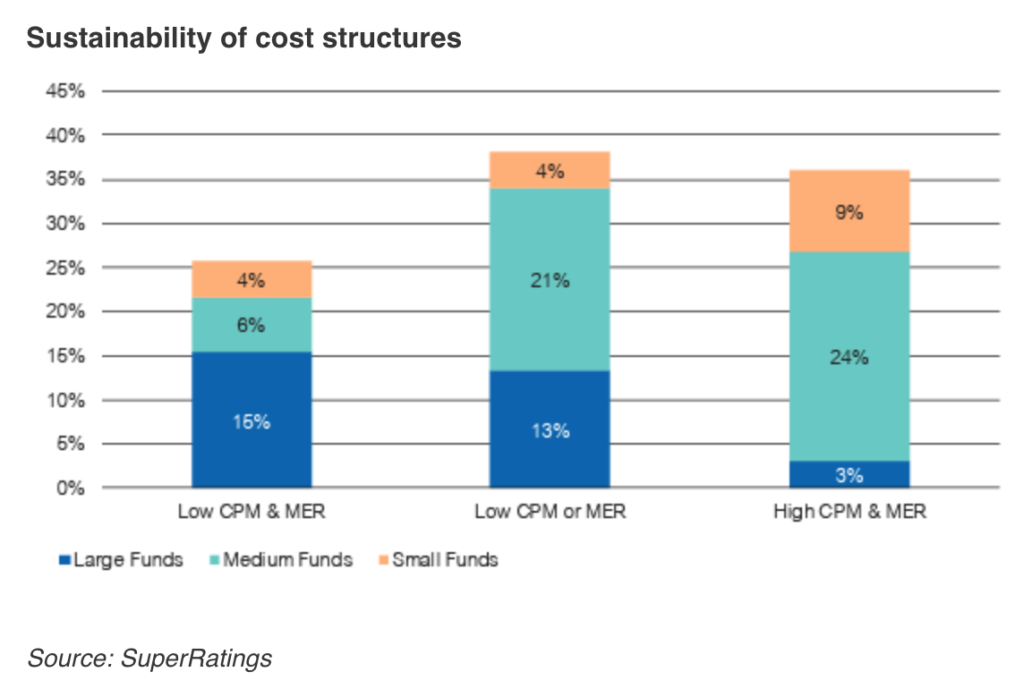

A key driver of mergers will be the sustainability of operating expenses, which as the chart below shows, is a challenge for some funds across all size categories. Though, smaller funds are more likely to have a high cost per member (CPM) and management expense ratio (MER), which measure the operational costs of the fund relative to its size.

“With the increased regulatory scrutiny on the sector, funds are focused on the challenge of increasing scale and driving down fees,” said Mr Rappell. “It’s pleasing to see that there’s a clear focus among providers on their plans to adapt to the changing landscape, which should support continued uplift in member outcomes.”

However, there remains a number of providers who are struggling to deliver sufficient value for money and the industry’s ability to address this is critical. APRA released its MySuper Heatmaps in December 2019 which highlight laggards based on investment returns, fees and sustainability metrics and has emphasised a tougher approach going forward. APRA also now has stronger powers to force underperforming funds to merge, which is likely to further drive consolidation across the industry.