Chaos theory – how APRA’s Disability Income Proposals and the Best Interests Duty are connected

For those of us involved in the post-Hayne life insurance sector the analogy of chaos theory may be a useful one.

Introduction

“Does the flap of a butterfly’s wings in Brazil set off a tornado in Texas?”

This was the question posed by Edward Lorenz[1], an American meteorologist and a pioneer of chaos theory who coined the term ‘butterfly effect’.

For those of us observing and/or involved in the post-Hayne life insurance sector – where the words ‘unintended consequences’ are heard and uttered frequently – the analogy of chaos theory may be a useful one. Not because the sector is in anyway chaotic (although some may disagree!), but because chaos theory itself posits that within the apparent randomness of chaotic complex systems, there are underlying patterns, interconnectedness, constant feedback loops, and repetition.

Unexpected connections

This idea of complex interconnections is an excellent lens through which to observe the life insurance sector. Understanding these interconnections can also help us understand and evaluate specific trends, events, and occurrences within the sector. This is especially true in relation to countless policy and regulatory changes our sector continues to adapt to.

For the purposes of this article we will examine two highly current and seemingly unrelated topics within the life insurance and advice sectors – APRA’s recent involvement in the Individual Disability Income Insurance (IDII) space; and the ongoing dialogue about the Safe Harbour provisions under the Best Interests Duty, seemingly under siege from both Kenneth Hayne and FASEA.

APRA moves to shore up retail Disability Income

In December 2019 the Australian Prudential Regulation Authority (APRA) announced a raft of new guidelines for life insurers in respect of the retail disability income product category.

These guidelines were a response to the increasing sustainability challenges faced by the category, which have seen life insurers lose more than $3.4 billion on individual disability income products over the last 5 years. (Alarmingly, a third of these losses – $1.1 billion – came in the last 12 months alone.) With at least one major reinsurer indicating they would cease supporting the DI market, and a strong possibility others would follow, APRA became concerned about the future viability of the product and – in order to help insurers protect the interests of both existing and prospective policy holders – decided to ‘intervene’.

The intent behind APRA’s intervention is to provide a framework within which life insurers can provide retail DI protection in a truly sustainable way. Whilst some mainstream media reporting on APRA’s announcement chose to focus on the ‘punitive’ nature of increased capital requirements for insurers issuing DI cover, the primary emphasis of the guidelines is on providing parameters around product features, pricing and even policy contractual terms, designed to ensure this valuable type of cover remains accessible and affordable, and at the same time improving the sustainability of the overall retail life sector.

Effectively APRA has paved the way for insurers to apply new thinking to an old problem, in a way that was previously much more difficult due to structural factors discussed later in this article.

What are the APRA DI measures[2]?

APRA has proposed measures in 3 categories:

1. Capital requirements

A capital charge imposed on all insurers, levied according to the quantum of their IDII exposure; This charge will be levied from 31st March 2020 and will remain in place until at least 31st March 2021, when APRA will conduct its first review of the effectiveness of the measures. At this time, individual insurers may have their charge increased or decreased depending on their own results.

2. Product design

Some design features of the typical IDII product have become problematic, because they can act to reduce a claimants incentive to return to work (thus creating ‘moral hazard’). These include the way total disability is defined and the way income is calculated at claim time. Compounding the issue is the limited ability of insurers to adjust contract terms through the life of a policy, as major experience changes become apparent.

In response, APRA has directed life insurers to:

- cease offering IDII agreed value6 contracts from 31 March 2020;

- have income at risk closely linked to the actual earnings at time of claim; and

- limit the income replacement ratio to support broader initiatives to encourage claimants to return to work, where appropriate.

APRA further noted that ‘current IDII products typically have policy contract terms and benefit periods set until the insured’s retirement age. These long time horizons contribute further uncertainty and complicate the sustainable management of IDII by reducing the ability to respond to changes in the external environment and consumer circumstances’

In response, APRA expects life companies to:

- have a framework to periodically update policy contract terms, while ensuring policyholders’ insurability rights are maintained; and

- manage their exposure to long benefit periods and have effective controls to manage the associated risks.”

(In line with these expectations, APRA is consulting with the industry on the possibility of mandatory 5 year fixed contract terms).

3. Data

Data is the key to having the most detailed and up-to-date view of claims experience possible, and APRA is encouraging to insurers to be highly collaborative and timely in the way they share data and review experience and assumptions.

First mover disadvantage- why APRA chose to intervene

When announcing[3] the proposed changes, APRA Director Geoff Summerhayes referenced, ‘first mover disadvantage’ as a possible explanation as to why life insurers hadn’t themselves sought to introduce similar measures, sooner.

In this context, ‘first mover disadvantage’ is predicated on the idea that the first insurer to make the types of changes sought by APRA would be at a commercial disadvantage on the basis that their products would be seen as less generous and therefore less attractive to customers and advisers.

Whilst conceptually simple, the materiality of ‘first mover disadvantage’ owes itself to a complex interplay between various structural factors within the retail life and advice sectors – including the interpretation of Best Interests Duty obligations, and the extent to which product research ratings are believed to assist in meeting them.

Let’s now explore this in more detail.

Best interests duty and the ‘Safe Harbour’

Introduced in 2013 as part of the Future of FInancial Advice (FOFA) recommendations, section 961b (1) of the Corporations Act requires advisers to “act in the best interests of the client in relation to the advice”.

Section 961b (2) sets out the ‘Safe Harbour’ provisions, a set of seven steps by which advisers can demonstrate they have met their Best Interests obligations.

To obtain the protection of the Safe Harbour, an adviser must demonstrate that they have:

- Identified the client’s needs and objectives;

- Identified the subject matter of advice sought by the client;

- Made reasonable enquiries to obtain complete and accurate information;

- Assessed whether the adviser has the expertise to provide the advice;

- Researched products that might meet the needs and objectives of the client;

- Based all judgements on the client’s needs and objectives; and

- Taken any other step that would reasonably be regarded as being in the best interests of the client.

Of particular interest to us is step 5.

Commissioner Hayne was critical of the Safe Harbour in totality, believing it encouraged a ‘tick a box’ approach to advice. However he reserved special criticism for step 5, claiming in his final report that in practice, it requires “little or no independent inquiry into, or assessment of, products.”

“In most cases, advisers and licensees act on the basis that the obligation to conduct a reasonable investigation is met by choosing a product from the licensee’s approved products list’”.

Whilst hard to question the accuracy of his observation, some may feel it a little harsh, given the intense scrutiny and pressure financial advisers find themselves under to constantly prove they are providing quality, compliant advice.

Is there little wonder that – in order to fulfil their obligations efficiently – many look solely to the guidance provided by ASIC in this area?

ASIC Regulatory Guidance 175 – product investigation

ASIC’s guidance in this area has helped frame attitudes to and practices around Approved Products Lists and Research Rating services, as can be seen below.

RG 175.325 A reasonable investigation conducted under s961B(2)(e) does not require an investigation into every product available:

RG 175.331 Advice providers may rely on investigations conducted by their AFS licensees. While they may also rely, to some extent, on various service providers (e.g. research houses), the advice provider remains responsible to the client for the advice that they give.

RG 175.336 One way an advice provider can conduct a reasonable investigation into financial products, for the purposes of s961B(2)(e)(i), is by benchmarking the product at appropriate intervals against the market for similar products to establish its competitiveness on key criteria, such as: (a) performance history over an appropriate period; (b) features; (c) fees; and (d) risk.

RG 175.346 The best interests duty does not prevent or require the use of approved product lists.

RG 175.347 In some cases, an advice provider can conduct a reasonable investigation into financial products under s961B(2)(e) by investigating the products on their AFS licensee’s approved product list.

How this works in the real world of life insurance advice

As can be seen above RG 175.336, whilst not mandating a reliance on research ratings, certainly suggests (and arguably encourages) it.

This seems appropriate given the complexity of retail life insurance products. Indeed, it is this complexity which some argue makes it impractical for an adviser to have a detailed knowledge of every single product and provider available, and in this context it can be seen how an APL and research ratings work hand in hand to help advisers make robust recommendations more efficiently.

Zurich[4] recently conducted research with financial advisers on this topic, seeking to understand key drivers of client recommendations. 200 active life insurance advisers were asked a range of questions, framed around Bests Interests Duty in relation to risk advice, and the attributes of the product and/or life insurer they saw as supporting their Best Interests obligations.

The results were enlightening:

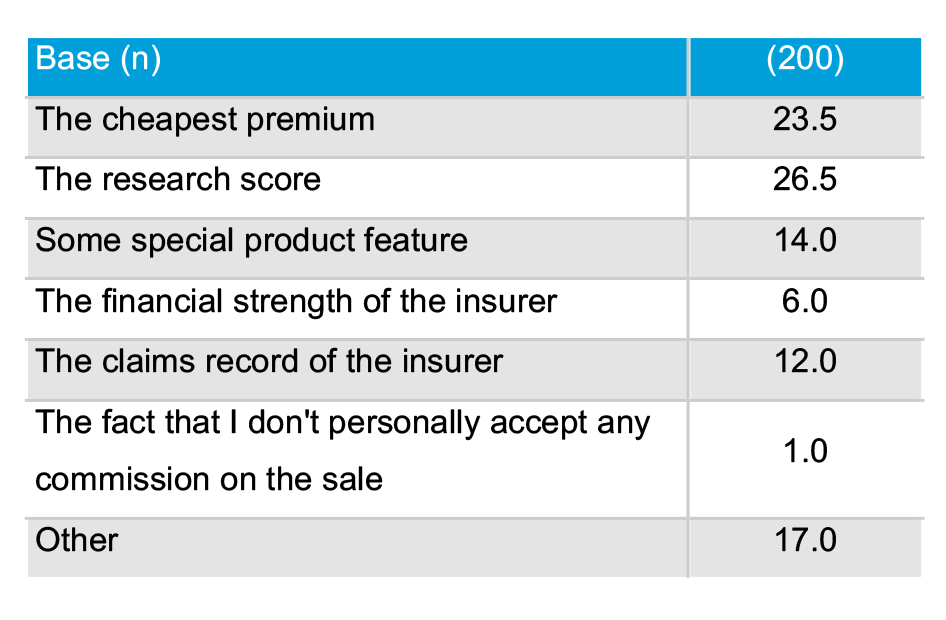

Question: which of the following does your advice process rely on the most as a demonstration of acting in your clients best interests?

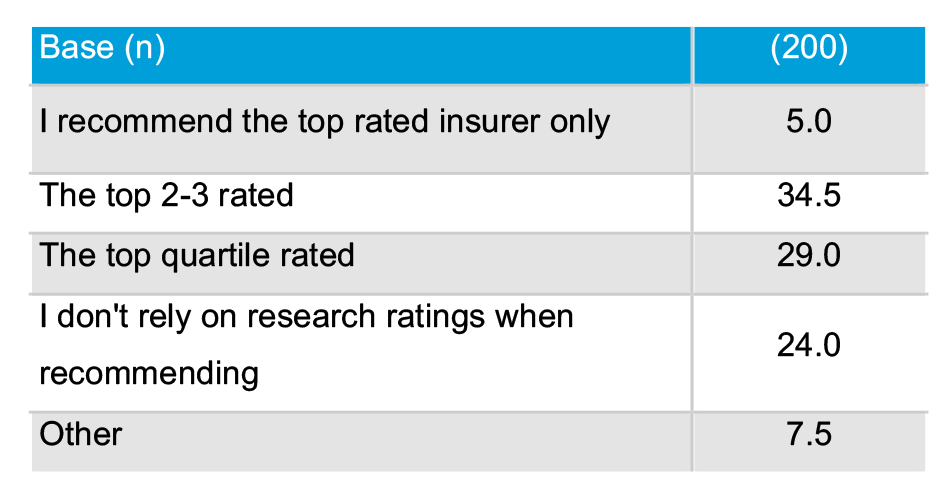

Question: What is your benchmark in terms of research ratings when considering an insurer?

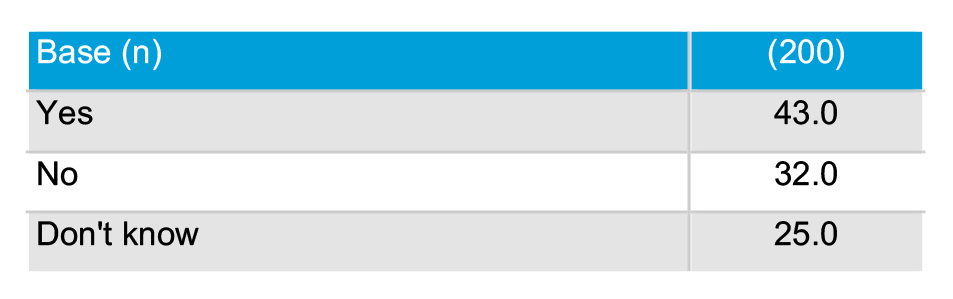

Question: Are there any insurers you wouldn’t recommend as they fall below your own ‘Bests Interests threshold?

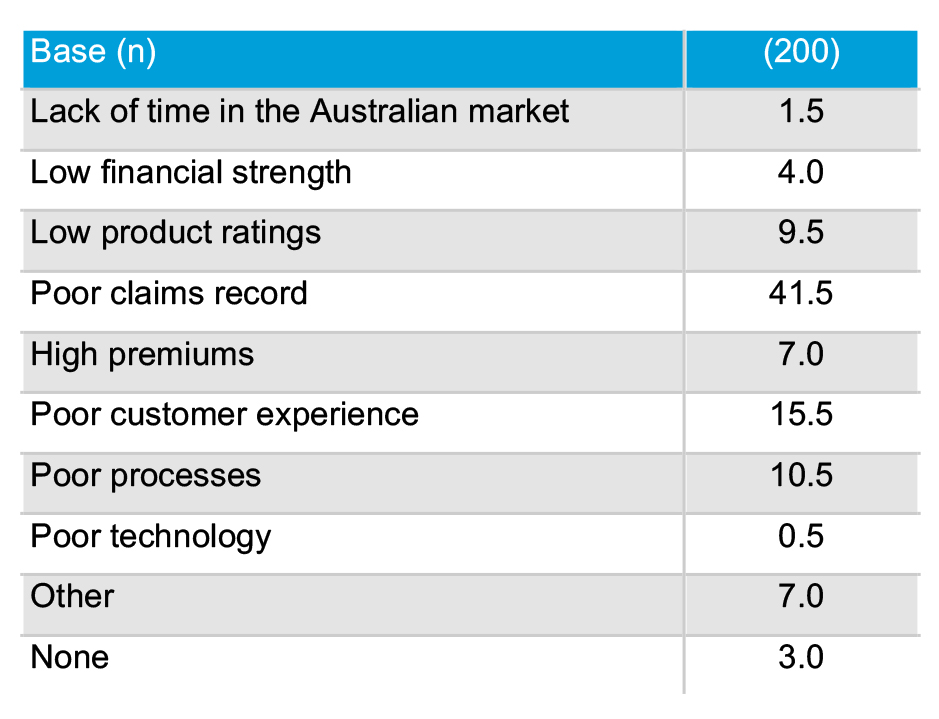

Question: Why do some insurers fall below your Best Interests threshold?

Examining the findings

As we can see, exactly half of those surveyed indicated premium or research rating as the single most important factor in them satisfying the product investigation step requirements under Best Interests Duty.

And when we dig deeper we can see that for those relying on research rating as their primary ‘proxy’, 40% would only choose a product rated in the top 3.

Claims record is also clearly a key driver, with over 40% identifying this as an attribute where the choice of insurer could be seen to compromise an adviser’s ability to meet their Best Interests obligations.

In the context of life insurance, successfully claiming on one’s insurance is the only time an insurer and adviser can truly deliver on the promise they have made to the client, and so the importance placed on claims record is unsurprising.

The butterfly and the tornado – making the connection

The aim of this paper was to (1) inform readers about two very important and current industry topics and (2) uncover the link between them.

If you have made it this far but still need help joining the dots, Munich Re summed it up best in their discussion paper “The price isn’t right and nor is the product”:

According to Munich Re[5], “There appears little doubt that competitive pressure to maintain research house product ratings which are in turn used to support “best interests” advice has contributed to product creep.”

Put more simply, the enormous pressure to provide quality, compliant, efficient advice has helped create an (understandable) reliance for some (not all) licensees and advisers on research ratings. This in turn has created pressure on product manufacturers to design products which garner the highest rating relative to their peers.

Combine that with relatively imperfect data about rapidly evolving societal trends impacting claims (eg mental health), and we see that this flapping butterfly has left us with a billion dollar challenge of concern to advisers, consumers, regulators, and of course insurers.

But it’s not all doom and gloom.

The measures proposed by APRA are sensible and will go a long way to returning this product category to a more sustainable footing, meaning it becomes more affordable and more accessible, without compromising on its core purpose.

This is important, as it remains the most claimed upon product in the market, with APRA data showing there are more income protection claims than claims for trauma, death and TPD put together.

And APRA isn’t cooling its heels on this issue; some of the measures announced have a March 31st 2020 start date. Meaning we will see a quick and meaningful response from the industry. The regulators and policy makers will be keeping a close watch – this approach may well set a precedent in dealing with other challenges.

Perhaps then we should let the last word go to Lorenz, from his 1972 paper:

“If the flap of a butterfly’s wings can be instrumental in generating a tornado, it can equally well be instrumental in preventing a tornado.”

———-

References

[1] Edward Lorenz, from paper to American Association for the Advancement of Science, 1972.

[2] Letter to life insurers, ‘Sustainability measures for individual disability income insurance’, APRA, December 2019.

[3] APRA Media Release, ‘APRA intervenes to improve sustainability of individual disability income insurance’, December 2019.

[4] Survey of 200 advisers actively recommending risk products, conducted by Beaton Research and Consulting on behalf of Zurich, 2018.

[5] Munich Re: Presentation to Institute of Actuaries, 2015.

![]()