Fidelity International Analyst Survey: A watershed year for ESG

As we enter a new decade, has uncovered a tipping point for corporates globally as they recognise that considering environmental, social and governance factors is not just the right thing to do, but good business too.

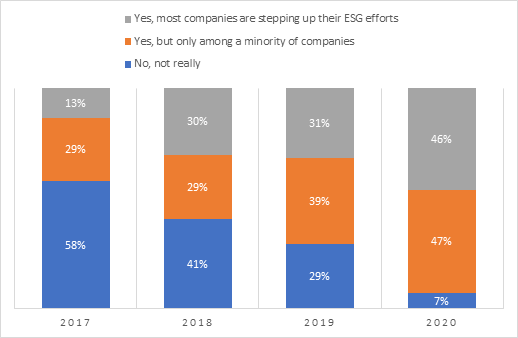

This year, 90 per cent of Fidelity International’s analysts report that some or all of the companies they cover are focusing more on ESG, up from 70 per cent in 2019. Following a pronounced increase in climate change awareness and corporate reforms, the change can be seen throughout most sectors and all regions, including areas where ESG interest had previously appeared to stall or be in decline.

Each year Fidelity International surveys its global analyst team to take the pulse of the corporate landscape. Unlike many other top-down macro-economic surveys, the research starts at the bottom, aggregating c. 15,000 individual company meetings until a big picture emerges.

While corporate governance is generally improving, with greater levels of investor engagement throughout the world, companies have made less progress on board diversity. Most Fidelity International analysts report that their companies’ boards have low to middling diversity, with almost no change on the previous year.

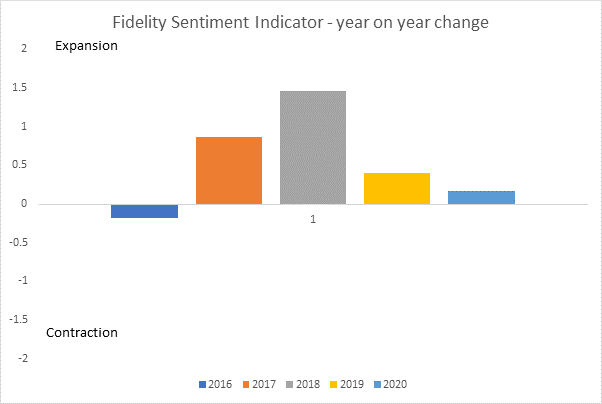

Chart 1: ESG issues shoot up the corporate agenda

Source: Fidelity International Analyst Survey 2020

ESG on the rise in China…and the US

While ESG has been increasing in importance for a while in Europe, it is now very much on the agenda in regions such as Asia and in particular, China where 80 per cent of analysts report an increase in ESG emphasis at some or all of their companies in 2020. This marks a dramatic rise from 63 per cent in last year’s survey and just 33 per cent in 2018.

Just over 90 per cent of Fidelity International’s analysts covering the US and Canada cite a growing emphasis on ESG at some or all of their companies, compared with just 57 per cent in 2019.

Chart 2: Regional breakdown

Source: Fidelity International Analyst Survey 2020

Jenn-Hui Tan, Global Head of Stewardship and Sustainable Investing at Fidelity International commented: “It is encouraging to see an increased focus on ESG from China corporates. We believe this is due a combination of factors including the Chinese authorities’ drive to improve governance, a rush among companies to invest in renewables before government subsidies are cut, and calls from investors for greater transparency around supply chains. More Chinese companies are also considering increasing dividends to shareholders and engaging with investors as a way of attracting further capital.

“In the US, despite a rolling back of environmental regulations at a federal level, interest is growing. Indeed, sustainability is bouncing back after appearing to be on the wane in 2019, spurred on by the very public re-definition of corporate purpose by the Business Roundtable.”

Global sentiment still positive…just

After correctly predicting an end to synchronised growth in 2019 but no recession, this year Fidelity International’s analysts believe the business environment will improve, but only slightly and at a slower pace. Recession again appears to have been postponed, at least until 2021, thanks to low interest rates, recovering global trade and a still-strong consumer. Only 36 per cent of analysts report that their companies are preparing for the end of the cycle, down from 49 per cent a year ago. Instead, Fidelity International analysts anticipate a calmer 12 months for corporate fundamentals in aggregate, even as geopolitical risks remain and the full impact of the coronavirus is still unknown.

Fiona O’Neill, Deputy Head of Equity Research at Fidelity International commented: “Fears of recession have certainly subsided since early 2019, especially in China where only 27% of analysts say companies are preparing for the end of the cycle, down significantly from 70% last year. In fact, the survey’s capex readings and a surprise spike in planned headcount across all sectors and regions (despite already low unemployment) suggest that many companies feel the cycle can be prolonged.

“The big unknown at present is the coronavirus: it’s just so difficult to gauge its length or severity. While we currently view this as a short-term disruptor to the China economy, if it is not effectively contained by Q2 it may well cause global forecasts to shift downward.”