Unconventional monetary policies – part 3: Lessons for investors from unconventional monetary policies – featuring high grade bonds

High-grade bonds grind out returns and dampen risky asset exposures, even in a muted yield environment.

Sovereign bonds have the potential to support investor returns during periods when countries pursue unconventional monetary policies.

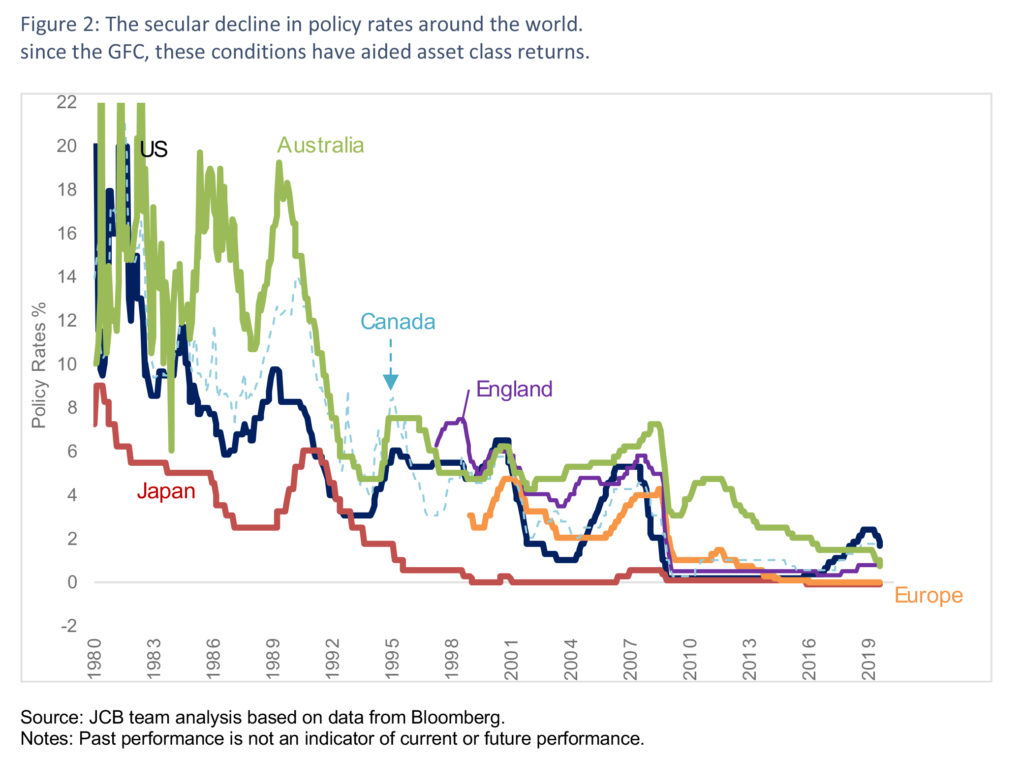

As lacklustre economic conditions persist around the world, large-scale, high-impact strategies such as zero interest rates and negative interest rates are being carefully considered by central banks across the world. They are likely to become increasingly mainstream and it’s important for investors to understand what their effects may be.

This is the final instalment in a three-part series exploring the effect of unconventional monetary policies on economies and financial markets. In the previous piece we looked at Japan and Germany’s approach to unconventional monetary policies. In this story, we’ll look at the impact they have had on different asset classes, with a special focus on sovereign bonds.

Investors have been forced to take on more risk in pursuit of returns or yield as central banks have lowered interest rates to near zero, zero or less. As such, investors have had to move up the risk spectrum to generate returns, while being penalised for holding onto cash given the low interest rate environment.

This has encouraged investors to allocate funds to more speculative assets such as emerging market debt, leveraged loans and private equity. But, while these instruments offer attractive yields, they also carry material, and often hidden, risks. With return expectations falling given myriad nearer-term economic headwinds, risk has been cheapened by these policies and risen in investor portfolios. These are typical features of a late-cycle environment.

At the same time, central bank rhetoric has altered investor beliefs. When poor economic data is released, central banks have further eased monetary policy, a strategy that has become increasingly ineffective. More and more accommodation is required just to maintain economic growth.

Risky assets rally hard in this environment. But markets have been lulled into a false sense of security. This has the potential to wrong-foot investors, especially in times of crisis.

Where to from here?

The world continues deeper into a late-cycle phase, one in which investors are encouraged by policy makers to reach for yield and return in an increasingly uncertain time. Thoughtful portfolio construction is one of the keys to navigating these difficulties.

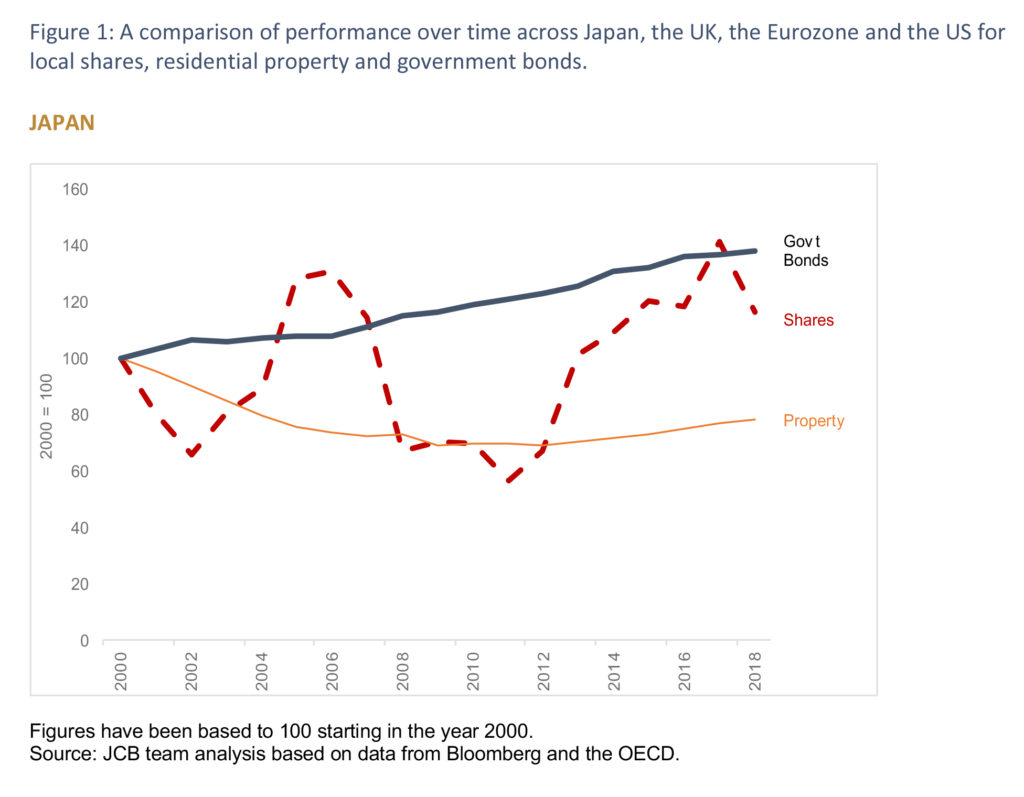

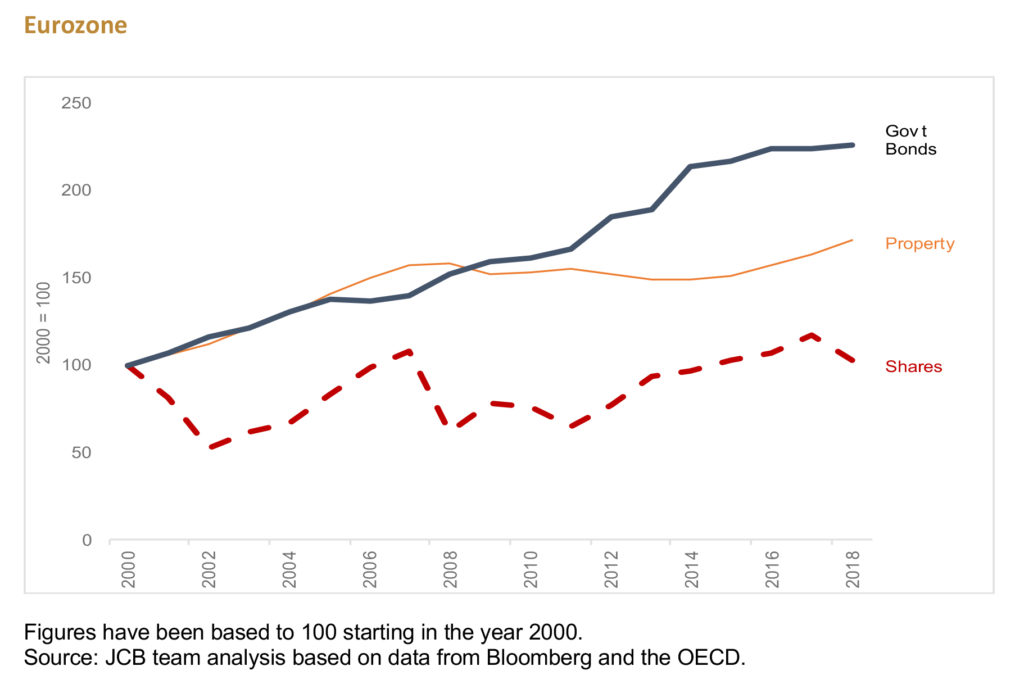

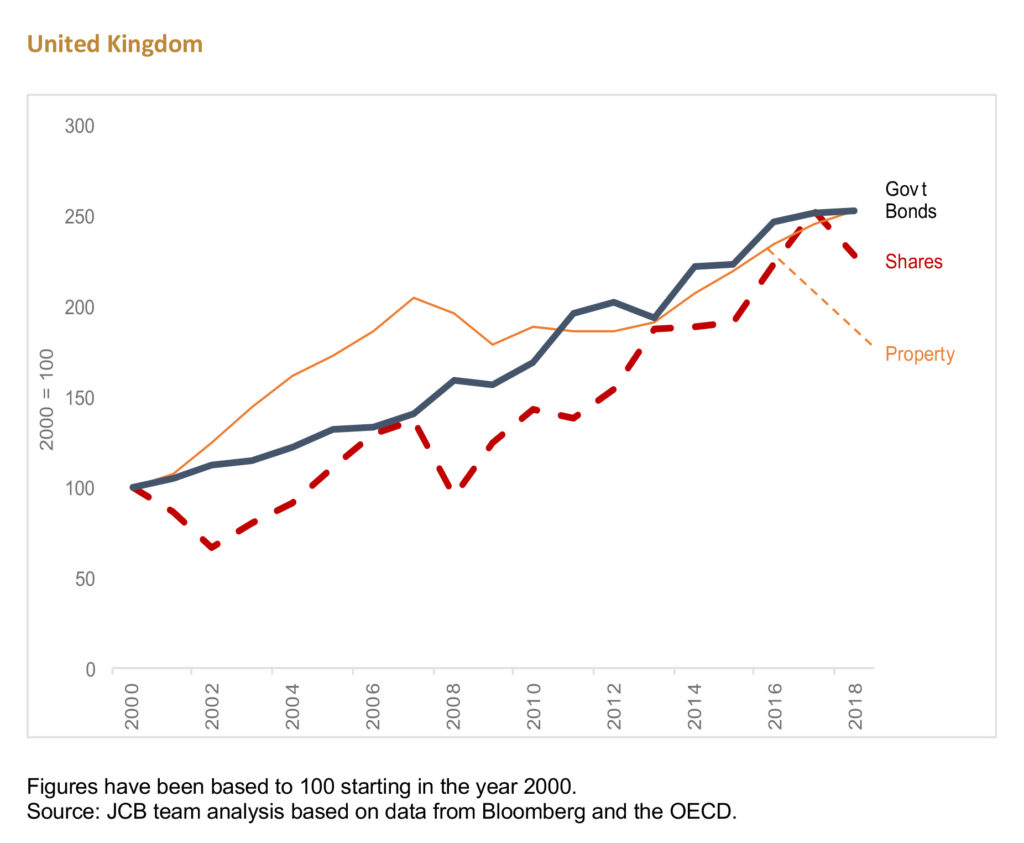

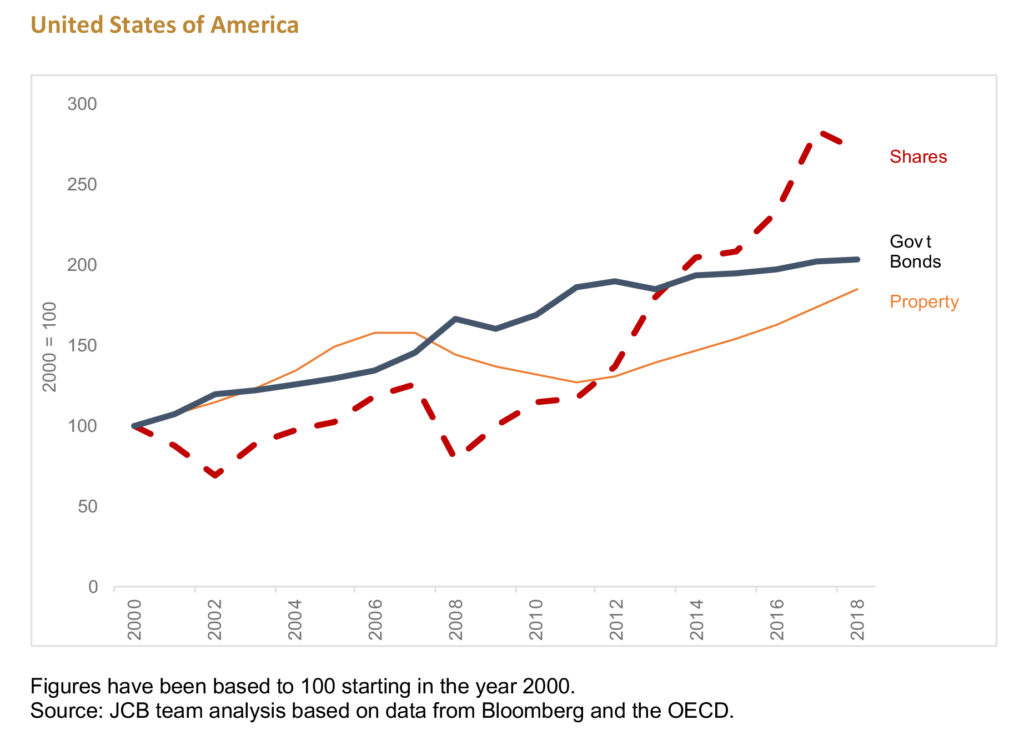

As the Japanese experience demonstrates, traditional asset classes such as cash endure difficult outcomes under these conditions. Bonds are the exception. They can offer compounding qualities that prove invaluable in a low-return environment.

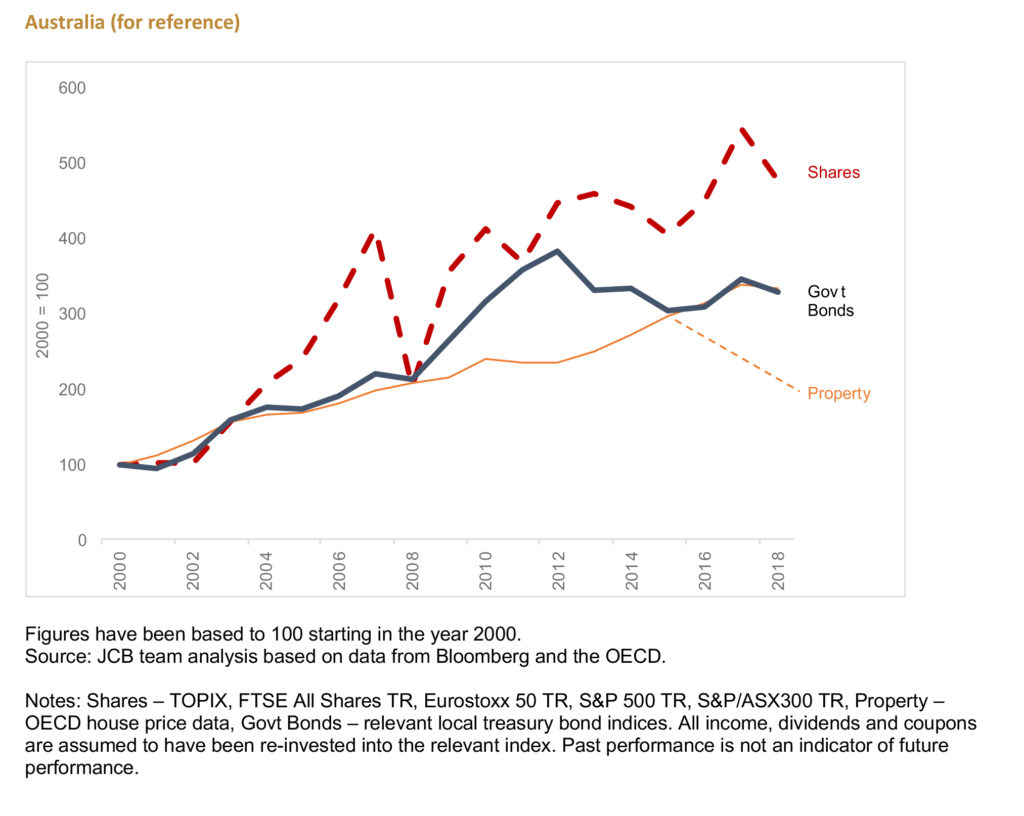

Investors who have tilted their portfolios towards risky assets such as shares and property have been conditioned since the GFC to believe returns are virtuous and markets are supported by central banks doing ‘whatever it takes’ to maintain an even economic keel. This is understandable when considering the strong performance shares and property have enjoyed in recent years. But this environment is unlikely to persist.

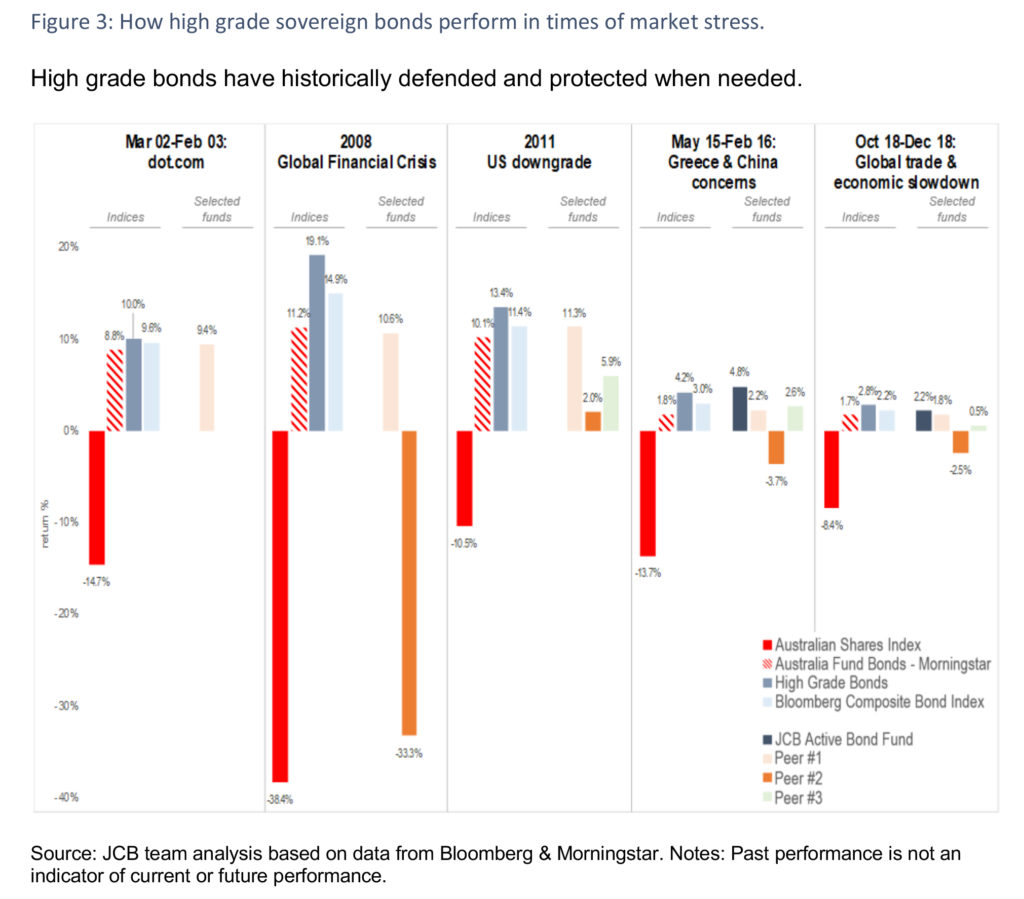

Against this backdrop, high-grade sovereign bonds have an enduring and a nearer-term role to play. While forward return expectations for all asset classes are somewhat dampened relative to historic trends, high-grade sovereign bonds offer benefits such as diversification.

High-grade bonds grind out returns and dampen risky asset exposures, even in a muted yield environment. They also deliver compound income over time and provide constructive returns. And, while their returns are likely to be moderated relative to trend, high-grade sovereign bonds offer protection against cyclical downturns and risky assets.

They also enjoy other advantages such as being backed by highly-rated governments including Australia which, alongside Canada and Switzerland, is one of three AAA-rated countries with wide scale, functioning bond markets. As stable and well-regulated nations, investors are confident governments can make good on their ongoing debt obligations, which supports the sovereign bond market.

Given the uncertainty and rising pressures in financial markets, proven sources of defensiveness and diversification such as sovereign bonds should help investors mitigate inevitable market pitfalls. In fact, there’s a case for having both domestic and global high-grade sovereign bond exposures in portfolios.

Central banks are likely to continue to use unconventional monetary policies in a persistent low-rate environment. As a result, it’s worthwhile for investors to consider the role of sovereign bonds in their portfolio to help mitigate risk and generate returns.