Weekly market update – week ending 20 March, 2020

Investment markets and key developments over the past week

Share markets remained under intense pressure over the last week as the number of new coronavirus cases continued to surge, economic data started to weaken sharply and financial markets saw increasing dysfunction. The latter was highlighted by a blow out in corporate borrowing rates and a surge in government bond yields earlier in the week (as fund managers facing redemptions sold their liquid previously strong positions) and increasing difficulty in accessing money market funding. At least, this has been matched by ever more aggressive government support measures and central bank moves to boost liquidity and by the end of the week the latter was helping with bond yields falling sharply. For the week US shares fell 15%, Eurozone shares fell 1.8%, Japanese shares lost 10.8%, Chinese shares dropped 6.2% and Australian shares fell 13.1%. From their recent highs to their recent lows US shares have fallen 32%, Eurozone shares have fallen 38%, Japanese shares have fallen 31%, Chinese shares have fallen 15% and Australian shares have fallen 33%. Commodity prices remained under pressure with oil down another 29% and even gold down, although iron ore has held up well. Despite a decline in bond yields later in the week, for the week as a whole they were mixed with yields down in the US and Italy but up in Germany, Japan and Australia. Safe haven demand saw the US dollar surge and this saw the $A plunge below $US0.56 at one point to levels not seen since 2003.

The news on coronavirus and its impact continued to worsen over the last week:

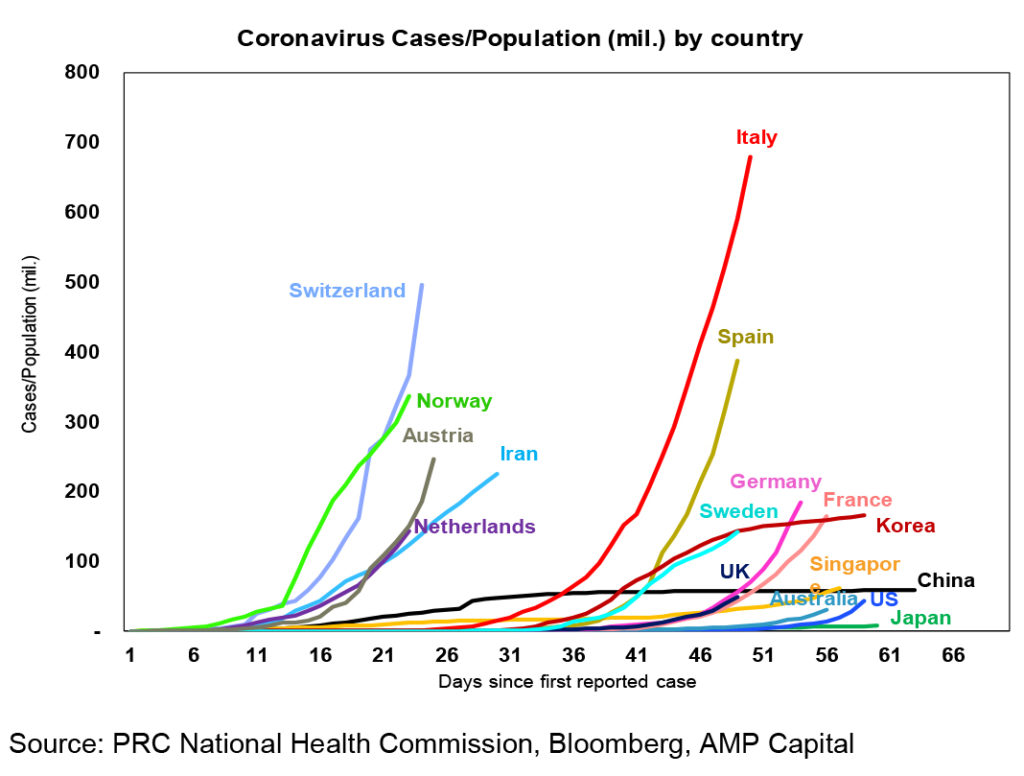

New cases outside China are continuing to surge.

![]()

- Italy, Switzerland, Spain and Norway are looking bad after adjusting for population. Which explains why Italy has now seen more deaths than China – its hospital system has become overwhelmed so the roughly 20% of cases who need hospitalisation and 5% who need intensive care don’t get it leading to many more deaths. The death rate in Italy has been 8.3%. Which is why social distancing is now so important.

- Flowing from this, lockdowns have intensified with several countries including Australia banning foreign arrivals and ever tighter limitations on engaging with others.

- Chinese economic activity data highlighted the impact shutdowns will have with January and February data showing falls compared to a year ago of 13.5% for industrial production, 20.5% for retail sales and 24.5% or investment.

- Reflecting the intense uncertainty over the economic outlook and fund redemptions, signs of market stress and illiquidity ramped up dramatically over the last week as evident in widening credit spreads and perversely rising bond yields and a surging US dollar. The latter now threatens a dollar funding crisis in emerging countries that have borrowed in US dollars.

But while the unfolding human crisis is horrible and the flow on to economies makes it all seem increasingly bleak it is worth continuing to bear in mind some positives from an economic and investment perspective:

First, after 30% plus falls shares are now cheap, particularly against ultra-low bond yields & interest rates. Forward PEs are now well below long term averages even allowing for a fall in earnings.

Second, negative investor sentiment is extreme – with the VIX (or fear index) having gone beyond levels seen in the GFC – which is positive from a contrarian point of view.

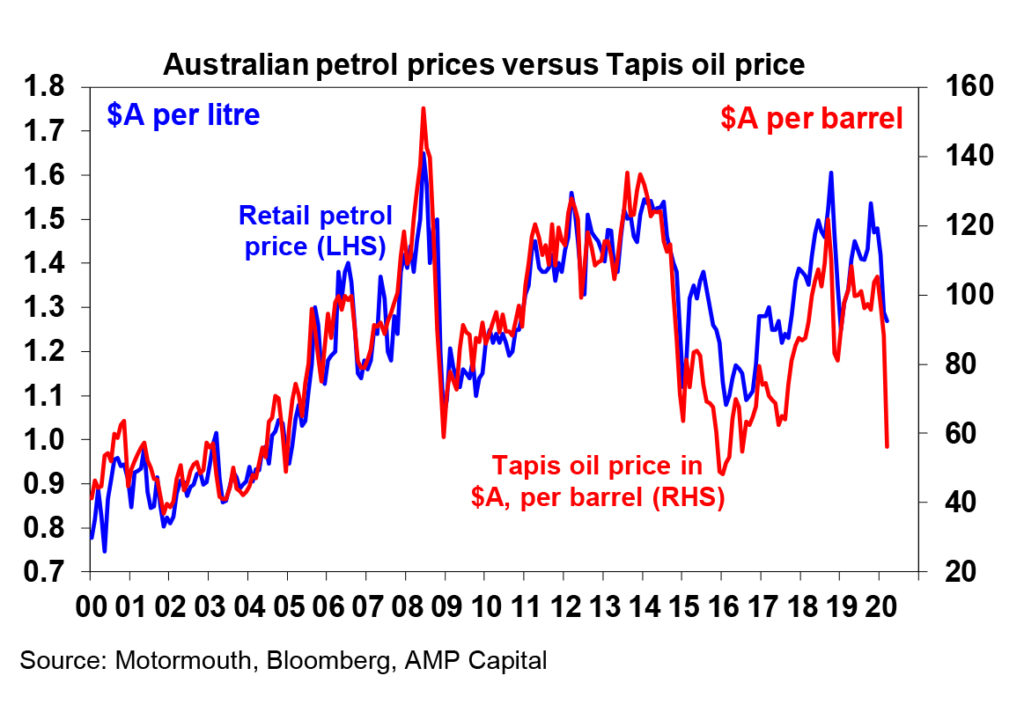

Third, the oil price collapse to an 18 year low is good news for motorists. Australian petrol prices are likely now on the way to around $1/litre which will save the average family around $16 a week on their petrol bill compared to what they were paying in December. It may not drive much of an increase in spending in the immediate months ahead as the lockdown continues but it will take a bit of pressure of family finances.

Fourth, and very importantly, the past week has seen a dramatic ramp up in government and central bank policy support on an almost daily basis. Highlights include:

- The Fed slashing interest rates by 100 basis points to zero, restarting quantitative easing with a $US700bn asset purchasing program and launching a commercial paper funding facility which would see it lend directly to companies and launching a facility to help stabilise money market mutual funds.

- President Trump and Congress moving towards a $US1.2trillion (5.5% of GDP), and now talk of $4trn, spending package which would include direct payments to individuals and businesses. Trump indicated support for the Government taking equity stakes in companies given bailouts and Larry Kudlow said, “we’ll do whatever it takes”.

- The UK providing £330bn in credit guarantees, cash grants and tax relief for impacted industries plus a three-month mortgage holiday for homeowners.

- The Bank of England cut rates by 0.15% to 0.1% and launched a new £200bn QE program aimed at reducing bond yields.

- The Bank of Japan expanded its asset purchasing or quantitative easing program.

- South Korea, the Philippines and Taiwan all cut interest rates.

- The Reserve Bank of NZ cut rates by 0.75% to 0.25% and the NZ Government announcing a 4% of GDP stimulus which is mostly front-loaded including wages subsidies for businesses. The RBNZ also announced a cheap funding scheme for banks.

- The ECB expanded its asset purchase program by a further €750bn (on top of last week’s extra €120bn) and indicated that it will be applied flexibly leaving plenty of scope to reduce Italian bond yields. Channelling Mario Draghi, ECB President Lagarde tweeted “there is no limit to our commitment to the euro”. This has seen Italian yields fall sharply and the move substantially reduces the risk of a Euro crisis. Along with EU moves to suspend fiscal rules it clears the way for an aggressive EU fiscal stimulus.

- In Australia, the Reserve Bank: cut the cash rate by 0.25% to 0.25%: committed to not raising rates until things are a lot better; announced a target for the three year bond yield of 0.25% to be backed by bond buying (quantitative easing basically); and announced low cost funding for banks at 0.25% for three years. The $90bn available for the latter alone is worth nearly all of the major banks’ wholesale funding requirements for a year! In other words, they will need little access to wholesale funding markets for a year which should get us well beyond this crisis period. On top of this the Australian Government is injecting $15bn into these markets to make it easier for smaller lenders to obtain funding. APRA has also relaxed capital requirements to make it easier for banks to keep lending. The RBA has also announced a swap arrangement for US dollars with the US Federal Reserve to make it easier for borrowers in US dollars to service their $US loans.

- Partly flowing from all the help provided to Australian banks, they have announced a deferral of small business loan repayments for six months and some have extended this to mortgage customers if they are hit by coronavirus problems. This will help take a huge amount of pressure off businesses and households. Banks have also announced sizeable reductions in various interest rates. Note that given the cheap funding being provided to the banks this may all turn out to be neutral for their margins and in the process they, with the RBA’s help, have headed off a potential sharp rise in defaults which would have been disastrous for everyone.

- The Australian Government is set to announce a further fiscal stimulus focussed on helping the unemployed, households and businesses. This is likely to be somewhere between $50bn-100bn (or 2.5-5% of GDP) and on top of the 1.2% of GDP stimulus already announced.

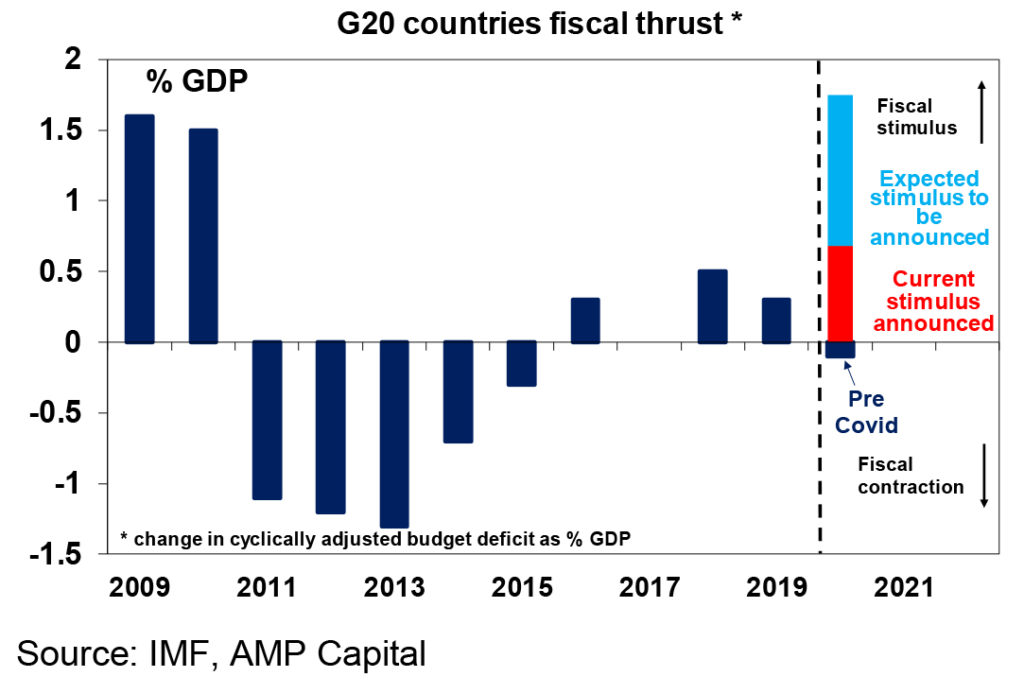

In all there have been over 200 stimulus announcements globally since the crisis began. While it’s not gone smoothly as policy makers (and most of us) did not initially realise the severity of the problem, central banks and governments seem committed to do “whatever it takes”. The next chart shows our estimate of global fiscal stimulus as a share of GDP over the year ahead. If currently proposed measures are introduced it will be greater than that seen in the GFC.

So why all the massive stimulus? Put simply the hit to the economy from coronavirus shutdowns could be worse than anything seen in the post world war two period. Our base case is now for a 3.5% contraction in the Australian economy but it risks being much greater. The key for RBA and Australian Governments and their counterparts globally is to make sure that collateral damage to businesses and households is kept to a minimum through the shutdown period so once the virus comes under control the economy can quickly rebound. This means doing whatever is necessary to minimise business failures, protect incomes and jobs and keep financial markets functioning. Governments will likely have to do more, but they seem committed to the task. This is very different to the Great Depression because it saw no monetary and fiscal stimulus at first. In fact, there was only policy tightening initially which along with an escalating trade war at the time explained why the Great Depression was so deep and so long.

But while these things will help minimise the downside and boost the recovery we still need to see evidence that the virus and its economic impact will come under control such that shares and other investment markets can be confident that the worst has been factored in before markets will bottom. Right now, this is still lacking.

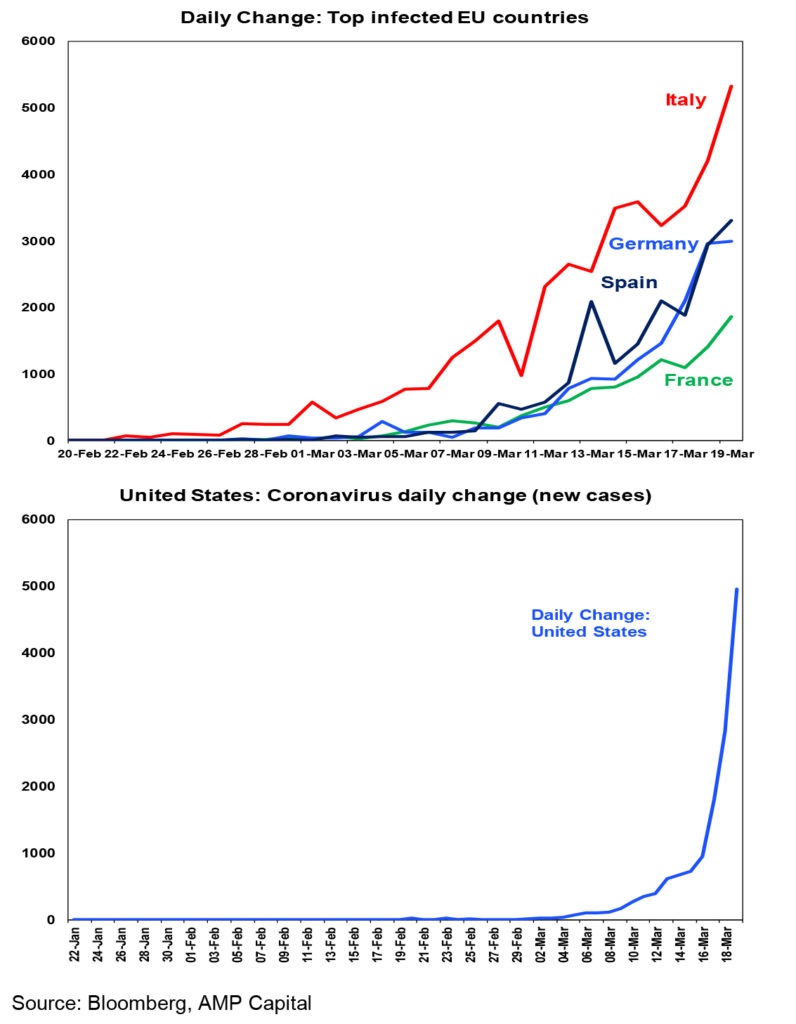

Key to watch for in the short term are: signs that the number of new cases (outside China) is peaking – countries to focus on now are Italy (because its earlier down the path of shutdowns) and the US (as it drives the direction of share markets); signs that corporate and household stress is being successfully kept to a minimum; signs that market liquidity is being maintained and supported as appropriate by authorities – this may soon get a tick; and possibly more policy stimulus to minimise the fall-out from shutdowns.

Major global economic events and implications

While US data for housing starts, home building conditions, existing home sales and industrial production was good in the last week, retail sales for February were weak and coronavirus shutdowns point to a sharp recession ahead. We expect a June quarter decline in annualised GDP of at least 20% (or 5%qoq). An indication of this was provided by sharp falls in regional manufacturing conditions indexes for March and a very sharp spike in weekly jobless claims.

The German IFO business conditions survey fell sharply in March. We expect June quarter GDP to contract by at least 6.5%qoq.

Chinese data for retail sales, investment and industrial production saw roughly 20% falls in January and February compared to a year ago as shutdowns impacted.

Australian economic events and implications

Australian retail sales rose more than expected in February and the jobs market was stronger than expected with unemployment falling back to 5.1%, but both are set to deteriorate from March.

What to watch over the next week?

The focus on the number of Covid-19 cases, associated lockdowns and the deepening economic impact and the global policy response to deal with it will no doubt remain the focus over the week ahead. Key to watch for in the weeks ahead will be a peak in the number of new cases in Italy and the US.

On the data front, March business conditions PMIs to be released Tuesday for the US, Europe and Japan are expected to show sharp 10-20 point falls reflecting the impact of coronavirus lockdowns on economic activity.

In the US expect to see falls in new home sales (Tuesday) and durable goods orders (Wednesday), but a rise in home prices (also Wednesday) and a modest gain in personal spending (Friday). Unemployment claims (Thursday) are expected to rise sharply. Core private final consumption deflator inflation is expected to rise slightly to 1.7% year on year.

Meetings by the Bank of England (Wednesday) and Reserve Bank of NZ (Thursday) will be watched for any further aggressive monetary easing moves

In Australia, the CBA’s business conditions PMIs for March (Tuesday) are likely to fall sharply as coronavirus lockdowns start to impact and expect a decline in skilled vacancies (Wednesday).

Outlook for investment markets

Shares are likely to see further short-term falls given the uncertainty around the coronavirus both in terms of the outbreak’s duration and its economic impact. But on a 12-month horizon shares are expected to see good total returns helped by an eventual rebound in economic activity and policy stimulus.

Low starting point yields are likely to result in low returns from bonds once the dust settles from coronavirus.

Unlisted commercial property and infrastructure are likely to continue benefitting from the search for yield but the decline in retail property values and the hit to economic activity from the virus will weigh on near term returns.

Our base case is that capital city house prices will continue to rise but at a slower pace than has been the case. However, this is now under threat given the expected recession in response to coronavirus disruption. A sharp rise in unemployment would pose a major threat to the property market. Hopefully stimulus measures will head that off as occurred in the GFC and bank deferrals of debt repayments will also help.

Cash & bank deposits are likely to provide very poor returns, with the RBA cutting the cash rate to 0.25%.

The deepening hit to global growth from Covid-19 and its flow on to reduced demand for Australian exports and lower commodity prices now risks pushing the $A to a re-test of its 2001 low of $US 0.477. Expect a strong rebound once the threat from coronavirus recedes though.

By Shane Oliver