Sharemarket update

- Australian sharemarket: The ASX 200 index has fallen around 29 per cent from the February 20 high.

- Long-term performance: In 144 years of calendar-year records, the Australian sharemarket has risen 71.5 per cent of the time with average annual gains (excluding dividends) of 6.5 per cent.

Analysis of recent trading on the sharemarket enables investors to take investment decisions.

Global sharemarket state of play

- We are just over a quarter of the way through 2020 so it is a good time to see where the Aussie sharemarket stands in the environment dominated by the COVID-19 coronavirus crisis.

- As at April 3, the ASX 200 had fallen by 24.9 per cent over 2020 with the All Ordinaries index down by 24.2 per cent. Those declines of around 25 per cent are very much in line with other global markets.

- The US Dow Jones has fallen by 26.2 per cent with the broader S&P 500 index down by 23 per cent. In Japan, the Nikkei has fallen 24.7 per cent. In Europe, the UK FTSE has fallen 28.2 per cent and in Germany the Dax is down 28.1 per cent.

- Overall, investors are factoring in the negative effects of COVID-19 on business revenues and therefore on profits. Gauging the magnitude of the economic impact has been difficult, but interestingly all the major markets have fallen by around 25 per cent over 2020.

- It is important to note that the US and Australian markets were at record highs not long ago. In fact the US Dow Jones hit all-time highs on February 12; the S&P 500 and the NASDAQ hit highs on February 19; and the ASX 200 and All Ords were at record levels on February 20.

- From record levels, the US Dow has fallen 28.8 per cent. The ASX 200 has fallen 29.2 per cent. So again, the declines we are experiencing in Australia are consistent with other markets, such as the US.

Perspectives

- The Australian sharemarket is down around 30 per cent from the highs on February 20. However it is also worth noting that key indexes such as the ASX 200 and All Ords are around 4 per cent above the lows recorded on March 23.

- Analysts like to define ‘bear markets’ as periods when markets are more than 20 per cent from highs. Similarly ‘bull markets’ are periods when markets are more than 20 per cent up from lows.

- The definitions are quite arbitrary, not taking into account the broader environment and whether the highs and lows were sustainable.

- While the Australian sharemarket is down 30 per cent from highs, those highs weren’t seen as sustainable. That is, the sharemarket had become ‘expensive’ and the expectation was that the market was at risk of a correction or perhaps a lengthy period of consolidation. In other words, earnings needed to catch up to share prices.

- The global nature of the gains and losses for sharemarkets in recent times is interesting, suggesting that investors haven’t been paying enough regard for local factors.

- Certainly global events such as the US-China trade war, Brexit and now COVID-19 have had major influences on major economies over the past year or so. And central banks collectively have been deploying maximum monetary stimulus to support economies and financial systems.

Australian sectors

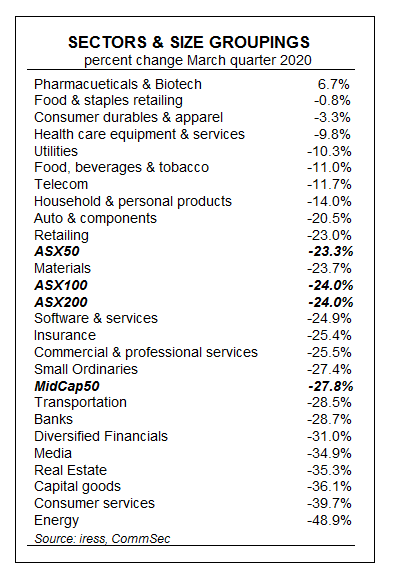

- Over the March quarter, only one of Australia’s 22 sub-industry sectors posted gains: Pharmaceuticals, Biotech and Life Sciences (up 6.7 per cent). Next best was Food & staples retailing, down by 0.8 per cent, and Consumer durables & apparel, down 3.3 per cent. Leading the declines was Energy (down by 48.9 per cent) from Consumer services (down 39.7 per cent) and Capital goods (down 36.1 per cent).

- The out-performance for the Pharmaceuticals, Health care and Food & staples retailing reflects increased demand for the services of companies in the sectors.

- In times of crises, ‘defensive’ sectors tend to do well. This reflects fundamental demand for services that don’t tend to follow economic cycles. So Utilities, Telecom and Food, beverage & tobacco have also tended to underperform the broader market.

- At the other end of the spectrum over the March quarter was the Energy sector. The magnitude of the decline reflects in part the decline in demand for travel (and thus demand for oil and other energy products). But also the fall in the Energy sector reflects the decision by major oil producers such as Saudi Arabia to ramp up production.

- It should be noted that oil prices have posted two record daily gains on hopes that major oil producers will act to restrict output. Oil prices have risen 40 per cent over the past two days.

- OPEC was to meet on April 6 but the meeting has been delayed to April 9.

- The Consumer Services sector was another underperformer in the March quarter, reflecting reduced demand for product and services of companies in the sector reflecting government travel restrictions and directives. The Consumer Services sector includes sub-sectors such as Restaurants, Leisure Facilities, Casinos & Gaming and Hotels, Resorts & Cruise Lines.

- The Banks, Diversified Financials and Insurance sectors also under-performed over the March quarter. And there has been further weakness in recent days. The Banks sector is now near 11-year lows, down 32.1 per cent over 2020.

- The European Central Bank (ECB) has asked banks to refrain from dividend payments in order to shore up balances sheets. British banks also have agreed to suspend dividends. And Reserve Bank New Zealand ordered local banks to freeze dividends.

- In Australia, the Australian Prudential Regulation Authority is liaising with banks on their plans for dividends and other distributions.

Where to from here?

- As we wrote in our March 30 paper (“COVID-19: Making sense of the economic impact”) these are extraordinary times with no exact precedent. The volatility has been breath-taking as has the speed of sharemarket falls from highs.

- But major sharemarket downturns in Australia have generally occurred when major downturns have been experienced globally. And the same has occurred with COVID-19.

- Past sharemarket downturns have been induced by economic or financial factors rather than a health crisis. The 2007 Global Financial Crisis (GFC) was a case in point. While the current downturn has its origin as a health emergency, investors are rightly assessing the economic implications – that is, the implications for companies, sectors, revenues and profitability.

- But the speed of the current sharemarket contraction has similarities to the October 1987 sharemarket crash. On both occasions, sharemarkets were perceived to have become expensive, raising the prospect of corrections or a period of market consolidation to restore value for investors.

- In 2007, it took 84 days for the All Ordinaries index to fall more than 20 per cent from the highs. In 1987, the sharemarket hit highs on September 21. It took 20 days for the All Ords to fall 10.9 per cent off its highs, before the massive 25 per cent fall on October 20.

- Compared with 2020, again there was nowhere near the speed of falls in sharemarket declines over periods such as 1970-74, 1982-83, or 1990-91 when there were times of economic downturn.

- The 1980s were volatile times for the economy and the sharemarket. The economy experienced a long recession from September quarter 1982 to June quarter 1983. Over 1981 the All Ords fell 14.4 per cent and then fell another 19.7 per cent in 1982. But in 1983 the sharemarket posted a 59.7 per cent gain – the biggest lift on record.

- In 1960, it took 42 days for the sharemarket to fall 20 per cent from the September 16 high. It actually took 717 days for the sharemarket to regain its 1960 highs.

- Looking back further, in the Great Depression, it took 6½ years for the Australian sharemarket to regain the February 1929 high. And it took more than 6 years for the September 1875 high to be exceeded.

- Still, in weak economic times and affected by the Spanish influenza pandemic, the sharemarket actually rose 19 per cent over 1919 and 1920.

What are the implications for investors?

- It is all about COVID-19. It is about finding treatments and a vaccine. It is about containment of the COVID-19 cases. It is about “flattening the curve”.

- The course of future events is largely out of the hands of policymakers. It is now up to the medical experts. But governments and central banks can – and indeed are – supporting businesses and people through the crisis period. Many of the measures taken are ‘temporary’. Just how ‘temporary’ remains to be seen.

- From Australia’s perspective, the banking system is unquestionably strong. And just like the 2007 GFC, federal and state balance sheets went into this COVID-19 crisis in good shape.

- Corporate Australia was also in reasonable shape, as judged by the recent reporting season. Of the ASX 200 companies that reported half-year results, 92.1 per cent reported a profit, above the 88.4 per cent long-term average.

- Over the past year the hard part for Australia’s listed companies has been to lift profits with only 50.7 per cent reporting higher profits than a year earlier (long-term average 60.3 per cent.)

- No doubt investors will be closely following the latest news on dividends. A number of companies have sought to suspend dividends in a period where revenues have been drying up. Companies clearly need to focus on survival first

- And while shareholders – especially those that rely on dividends for income – will be disappointed that dividends may not be paid or will be delayed, they are keenly wanting to see companies come out of the crisis in reasonable shape.

- The Australian sharemarket is at risk of recession. And if not recession, the economy is expected to remain weak over much of 2020. But Australia has experienced weak economic times in the past, and as noted above, one of the most protracted periods of weakness over 1982/83.

- The sharemarket fell 34 per cent over 1981 and 1982 but then posted a record 59.7 per cent rebound in 1983.

- One thing is for certain, there will always be economic cycles. And while the sharemarket will also experience cycles, in the past it has been notable for anticipating the recovery. Defining at what point that occurs is the hard part.