Consumer confidence; Spending; RBA Board minutes; Payrolls

- Consumer confidence: The weekly ANZ-Roy Morgan consumer confidence rating rose by 7.7 per cent to 84.2 points.

- CBA Household Spending Intentions (HSI): According to the Commonwealth Bank, “Efforts to slow the spread of Covid‑19 can be dramatically seen in the Household Spending Intentions readings for March 2020 – with Travel and Entertainment spending intentions declining sharply. In contrast, the Retail and Health & fitness sectors both saw sharp increases in March. Pleasingly, Home buying intentions have largely held up at high levels, while Education spending intentions stabilised after February’s sharp decline.”

- Reserve Bank Board minutes: The Reserve Bank confirmed its commitment to keep the cash rate and the yield on 3-year government bonds near 0.25 percent as long as necessary.

- New survey of payrolls & wages: The Bureau of Statistics reported that between the week ending 28 March 2020 and the week ending 4 April 2020 employee jobs decreased by 5.5 per cent, compared to a decrease of 0.5 per cent in the previous week

The consumer confidence figures have implications for retailers, and other consumer-focussed businesses. The CBA household spending intentions survey provides guidance for consumer-focussed businesses. The payroll and wage data helps government with decisions on assistance measures for households and businesses.

What does it all mean?

- The Australian Bureau of Statistics (ABS) and Australian Tax Office are to be congratulated for the new survey showing the impact of COVID-19 on jobs and wages. Governments need the latest data so they can best direct assistance to those in most need.

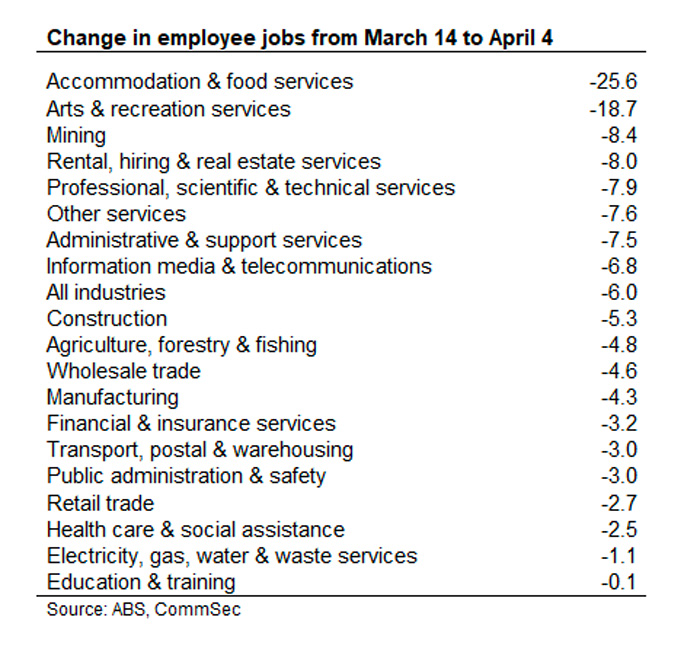

- Clearly workers in hotels, cafes and restaurants are doing it tough with jobs down 25.6 per cent in the space of three weeks. Mining is a surprise with jobs down over 8 per cent. But jobs in the utilities and education sectors are relatively unchanged.

- Aussie consumers are no doubt encouraged by the progress made in ‘flattening the curve’ as well as lower petrol prices.

- Sentiment has lifted by 26.5 per cent since hitting record lows (lowest since 1973) of 65.3 points on March 29. But sentiment is below both the average of 113.3 points held since 2014 and the longer term average of 113.0 points since 1990. Consumers’ inflation expectations fell from 3.8 per cent to a record low (since 2010) of 3.1 per cent as national average retail petrol prices hit 4-year lows of 107.2 cents a litre last week.

What do the figures show?

Consumer sentiment – Week ended April 19

- The weekly ANZ-Roy Morgan consumer confidence rating rose by 7.7 per cent to 84.2 points. Sentiment has lifted by 26.5 per cent since hitting record lows (lowest since 1973) of 65.3 points on March 29.

- Four of the five major components of the index rose last week:

- The estimate of family finances compared with a year ago was down from -19.1 points to -21.2 points;

- The estimate of family finances over the next year was up from +5.2 points to +12.1 points;

- Economic conditions over the next 12 months was up from -53.1 points to -48.6 points;

- Economic conditions over the next 5 years was up from -7.9 points to -1.7 points;

- The measure of whether it was a good time to buy a major household item was up from -33.9 points to -19.7 points.

- The measure of inflation expectations fell from 3.8 per cent to a record low (since 2010) of 3.1 per cent.

The Commonwealth Bank (CBA) Household Spending Intentions Series (HSI) – March

- On home buying intentions: “Home buying intentions declined marginally in March, but remained near all-time record highs. Since March, however, turnover in the housing market has declined significant as public open houses and public auctions were banned, as evidenced by the fall in auction clearance rates. Rising job insecurity is also a factor.”

- On retail spending intentions: “After a number of months of soft outcomes, Retail spending intentions jumped substantially higher in March. The surge in spending in March was related to consumer’s response to the developing Covid-19 shutdowns and restrictions and a jump in spending on supermarket items, alcohol and household equipment and furnishings. Our CBA credit/debit card data to 17th April shows that spending weakened through to mid-April, with spending on Goods flat on the year and Retail spending down marginally on a year earlier.”

- On travel spending intentions: “Travel spending intentions declined sharply in March as the Covid-19 shutdown and travel restrictions took hold.”

- On health & fitness spending intentions: “After an initial downturn related to the bushfires in February, the Health & Fitness HSI jumped sharply high in March. The increase in the Health and Fitness HSI is related to spending intentions on medical needs and the desire to create ‘home gyms’ and/or undertake ‘virtual’ personal training activities in the Covid-19 shutdown period.”

- On entertainment spending: “The March Entertainment HSI reading is the lowest in the history of the HSI and well below the February reading.”

- On education spending intentions: “The Education HSI picked-up in March, however, as ‘on-line’ and ‘virtual’ schooling and higher education began to dominate.”

- On motor vehicle purchase intentions: “The improvement in HIS readings for motor vehicles partly reversed in March as the Covid-19 shutdown made shopping for a new car or commercial vehicle challenging.”

Minutes of the Reserve Bank Board meeting held on April 7

- The minutes can be found here: https://www.rba.gov.au/monetary-policy/rba-board-minutes/2020/2020-04-07.html

- Final paragraph: “The Board confirmed that the target for three-year yields would be maintained until progress was made towards the Bank’s goals of full employment and the inflation target, and that it would be appropriate to remove the yield target before the cash rate itself was raised. The Board would not increase the cash rate target until progress is made towards full employment and it is confident that inflation will be sustainably within the 2–3 per cent target band.”

- Three-year bond yield target: “The Bank would continue to do what was necessary to achieve the three-year yield target, with the target expected to remain in place until progress was being made towards its goals for full employment and inflation.”

- Market operations: “Members noted that, if conditions continued to improve, it was likely that smaller and less frequent purchases of government bonds would be required.”

- Reserve Bank purchases: “The Bank had purchased in aggregate around $36 billion of government bonds in secondary markets.”…”Alongside these purchases, the Bank had injected around $50 billion of liquidity into the financial system through its daily open market operations to support credit and maintain low funding costs in the economy.”

Weekly payroll and wages

- The Australian Bureau of Statistics (ABS) released a new survey: “Weekly Payroll Jobs and Wages in Australia”.

- The ABS reported:

- “Between the week ending 28 March 2020 and the week ending 4 April 2020:

- Employee jobs decreased by 5.5 per cent, compared to a decrease of 0.5 per cent in the previous week

- Total wages paid decreased by 5.1 per cent, compared to a decrease of 1.3 per cent in the previous week”

- The total loss of jobs of 6 per cent since March 14 was fairly uniform by sex and across states and territories. Jobs in the Northern Territory fell by 4.8 per cent followed by Queensland (down 5.0 per cent). And at the other scale Tasmanian jobs fell by 7.3 per cent with Victoria down 6.8 per cent.

- By industry, employee jobs fell most in the three weeks to April 4 in Accommodation & food services (down 25.6 per cent) from Arts & recreation services (down 18.7 per cent). In the Education & training sector, jobs fell just 0.1 per cent.

- Employee jobs for people aged under 20 decreased by 9.9 per cent and those worked by people aged 70 and over decreased by 9.7 per cent. Meanwhile for those aged 50-59 years, jobs fell just 3.8 per cent.

What is the importance of the economic data?

- Westpac and the Melbourne Institute release the Index of Consumer Sentiment each month. The ANZ/Roy Morgan weekly survey of consumer confidence closely tracks the monthly Westpac/Melbourne Institute consumer sentiment index but the former measure is a timelier assessment of consumer attitudes. Confident consumers may be more inclined to spend, especially on major items.

- The ABS data Weekly payroll jobs and wages “provides indicative information on the economic impact of the COVID-19 coronavirus on employees, including changes in employee jobs, changes in total wages, and changes in average weekly wages per job.”

What are the implications for investors?

- No surprises in the new ABS data, showing that young workers in cafes, restaurants and hotels have been most affected in economic and financial terms by COVID-19. But encouragement for the housing sector in the latest survey of household spending intentions. Interestingly home prices in the five mainland state capital cities have risen 0.3 per cent so far in April with Sydney prices up 0.6 per cent.

- As we keep on stressing, it’s all about COVID-19. And new stats showing a lift in consumer confidence can be linked to moderation in the number of new COVID-19 cases. That is music to the ears of retailers. Those motorists still on the road are also benefitting from lower petrol prices. And those lower prices reflect the COVID-19 measures restricting travel.

- Is this the beginning of the end for the current labour force survey? According to the ABS, “approximately 99 per cent of substantial employers (those with 20 or more employees) and 71 per cent of small employers (19 or fewer employees) are currently reporting through STP” (the Single Touch Payroll system.